What a time it is to be a lithium investor – When spot prices and valuations were on the backfoot, Albemarle lobbed three lowball offers at Liontown Resources (ASX: LTR), which drove a sector-wide rebound. And when Chinese lithium prices bottomed in late April, the stocks were also quick to recover.

Does this dynamic of optimistic M&A, coupled with well-documented factors such as tight supply and electric vehicle demand create a floor for lithium stocks? And if so, shouldn’t investors be buying the dip?

In this wire, I sat down with Wilsons’ Senior Metals & Mining Equity Analyst – Sam Catalano – to break down the state of play for ASX-listed lithium stocks and perhaps more importantly, where should investors go if they’ve missed the boat?

Never miss an update

Get the latest insights from me in your inbox when they’re published.

FOLLOW

The Story So Far: The dust settles after a 70% drawdown

Large cap lithium names like Pilbara Minerals (ASX: PLS) and Allkem (ASX: AKE) experienced a ~40% drawdown from November 2022 peaks to late March lows.

Pilbara Minerals 6-month price chart (Source: Market Index)

The stocks managed to bottom a month before the underlying commodity thanks to Albemarle’s unsolicited takeover bid for Liontown on 28 March, which offered $2.50 per share (63.7% premium).

But Liontown management wanted none of it, describing the bid as “opportunistic” and seeking to take advantage of the “recent softness in companies exposed to the lithium sector and the pre-production status of the Kathleen Valley Project.”

So, here’s my logic from all of this:

Lithium prices fall: Stocks tank and large players seek to buy ‘low hanging fruit’

Lithium prices rise: Lithium stocks rise as well

Wouldn’t this dynamic create a floor for lithium stocks?

“Commodity sectors and equities are always going to be volatile in the short-term, and the stocking and destocking cycles have impacted the lithium space over the past six months,” explains Catalano.

“I would think that when there is weakness in equity prices, the M&A thematic in this space is something that will help provide something of a floor to valuations and should provide confidence to investors.” If there is support and a floor for valuations, then wouldn’t investors, more broadly speaking, be buying the dip?

“Absolutely, this is a thematic that we believe has got legs and the lithium market appears to be structurally undersupplied for quite some time into the future,” said Catalano. Don’t sleep on Africa

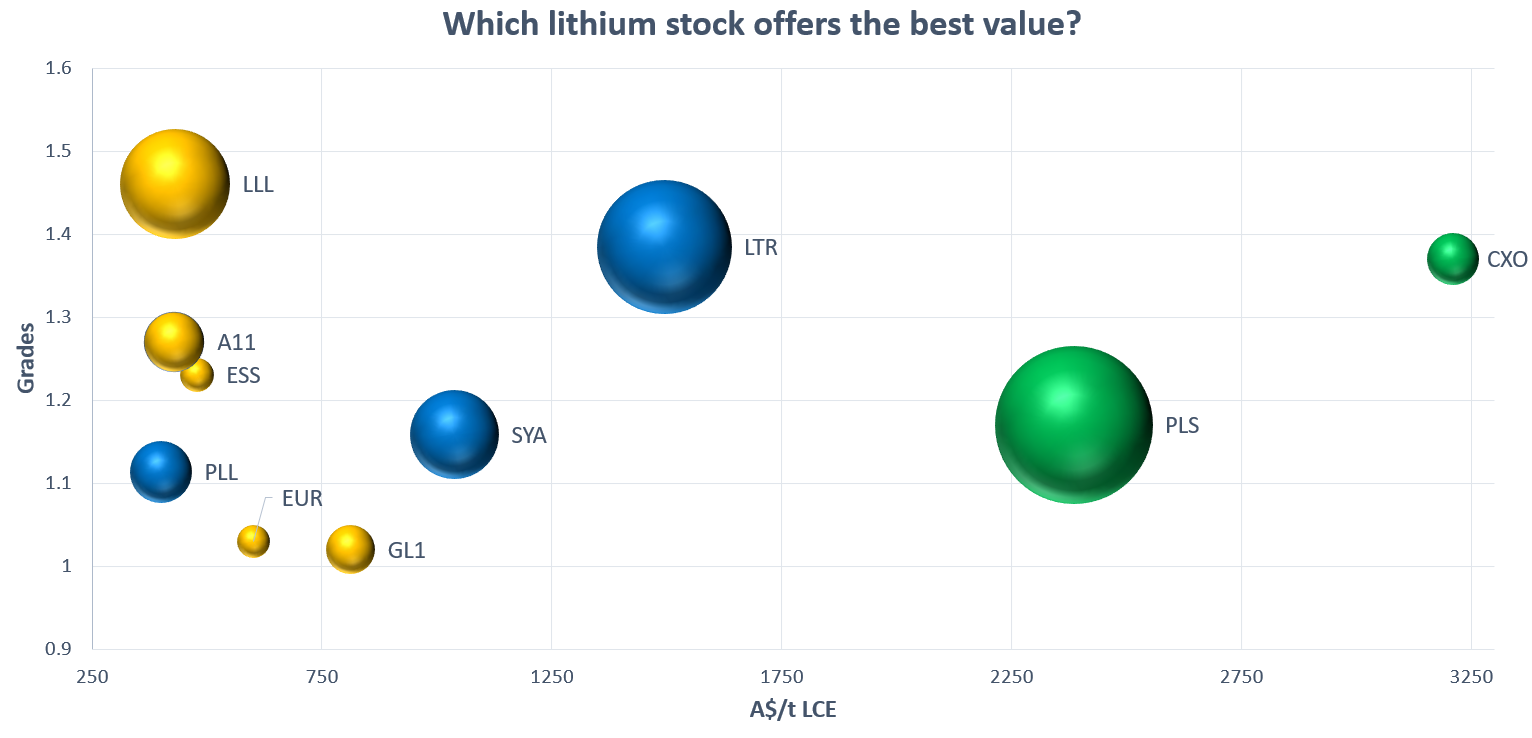

Earlier this month, I wanted to find out which hard rock lithium stocks offer the best value for money based on market capitalisation and mineral resource.

Notwithstanding other factors such as project status and production costs etc, Africa-based projects like Leo Lithium (ASX: LLL) and Atlantic Lithium (ASX: A11) were trading at a substantial discount to peers.

The graph is for illustrative purposes only and should not be used as investment advice (Source: Market Index)

There might be a million good things about Leo Lithium but you can always finish the sentence with “but their project is located in Mali”. What’s the risk of investing in these Africa-based projects, is it tangible or more of an overhang or stigma?

“There have been some challenges in some jurisdictions over time. If you look at Mali, which is where Leo Lithium’s Goulamina Project is located, they’ve had two military coups in the last couple of years as well as sanctions and border closures,” said Catalano.

“But you also need to think about how these events are impacting the mining sector and by and large, you’ve actually seen the minerals industry in that country suffer relatively little disruption.”

Atlantic Lithium on the other hand, operates the Ewoyaa Project in Ghana – Which was reported as one of the best places to do business in Africa, according to EY’s Africa Attractiveness Report.

“Places like Ghana often get perceived as high risk just by nearby geography if anything else,” he said. How does one get a re-rate?

Leo Lithium’s Goulamina Project (50% owned) has a resource that’s comparable to Liontown Resources, a post-tax NPV of US$2.9bn and set to hit production status in 2024. But will its valuation always be subdued simply because of where it’s located?

When it comes to breaking the mould – I immediately thought about Alpha HPA (ASX: A4N), an emerging producer of high-purity alumina. In short, the stock went nowhere between May 2021 and March 2023. As the company started to put the pieces together, the market started to think “hey they’re actually going to do this and the margins are pretty mean.”

The stock would break out of its two year base and rally as much as 80% in less than three weeks.

Alpha HPA 5-year chart (Source: Market Index)

I asked Catalano whether or not we could see something similar for Leo Lithium and Africa-based producers, where at some point, the market cannot ignore the fundamentals.

“The difficult thing for some stocks, particularly when they’re pre-production and pre-revenue, is that nothing is really changing. Even when the project is progressing, the market struggles to see exactly what is going on,” explains Catalano.

“But the catalyst for a re-rate here is when the company starts producing cash. And in the case of Leo Lithium is around 12 months or a little less if you consider their early cash flows from direct shipping ore.”

“Within 12 months, you’re suddenly going to start seeing significant cash flow in the door. By our numbers, we’ve got the stock trading on an average free cash flow of 50% for each of the first four years of operation and going higher after that as they ramp up to higher levels of production”.

Leo Lithium shares rallied 70% in May, supported by announcements including high-grade drilling results last week and a $106 million placement (held at a premium) on Monday. Even after the breakout, brokers like Wilsons and Macquarie both have target prices around $1.50.

Leo Lithium 12-month price chart (Source: Market Index) What about back at home?

What about the names in our backyard like Pilbara Minerals and Core Lithium?

“A lot of the domestic, easy-to-own exposures are relatively fully priced. And that’s the difference,” said Catalano, adding that “the real upside opportunities lie in exposure to developers, whether they be domestic or offshore.”

“Perhaps going outside of the vanilla is where the opportunities are.”

What's your next Pilbara Minerals or Core Lithium? And what makes them so compelling? Let us know in the comments section below.

VIEW DISCLAIMER:

Livewire gives readers access to information and educational content provided by financial services professionals and companies (“Livewire Contributors”. Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

LLL Price at posting:

84.5¢ Sentiment: Buy Disclosure: Held

. Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

%20Share%20Price%20-%20Market%20Index.png)

%20Share%20Price%20-%20Market%20Index.png)

%20Share%20Price%20-%20Market%20Index.png)

(20min delay)

(20min delay)