Arcadium Lithium (formerly Livent) is a revenue-generating company trading at $3.36. It offers a ridiculous amount of value.

Lithium stocks are currently unpopular due to sector-wide destruction, slow government loans, and economic uncertainties. However, future demand is expected to increase significantly.

Major companies like Honda, Volkswagen, Panasonic, Asahi Kasei, Rivian, and Toyota are investing billions in EV and lithium technologies.

Lithium investors are currently despondent and lithium stocks are trading at extreme value levels. A buy and hold strategy could work.

MF3d

I was looking over lithium ticker symbols last week and ran across a name that I've not looked at in ages, Livent, now called Arcadium Lithium (NYSE:ALTM) (after its merger with Allkem). Arcadium is a great company, it has a lot of revenue, and it is much different than most of the speculative lithium stocks I write about.

I was shocked when I pulled up the ticker and they were trading at a mere $3.36. In this article we are going to look at Arcadium and we are going to look at the lithium market. The question is, does investing in lithium still make sense? If so, should we invest in Arcadium Lithium? Does Lithium Make Sense?

I think it is safe to say that lithium stocks are almost universally despised at the moment. After a fantastic run a few years ago, it has been nothing but a non-stop pain-train. Month after month of sector wide destruction as lithium prices started to come back to reality. EV sales, while growing, are also slowing down some as the economy continues to struggle with inflation and a housing crisis due to high interest rates on inflated home prices.

Meanwhile the Inflation Reduction Act ("IRA") is moving about as fast as a stunned slug (as far as funding lithium projects). It took Lithium Americas (LAC) two years from competition of the DFS study to obtain a loan and that is still pending as they are waiting on General Motors (GM) to fund tranche two.

Digressions aside, the IRA loans have moved slower than anyone theorized. Thus lower lithium prices, consumers getting squeezed on housing and inflation, combined with slow government loans and on top of all of that you have the 2024 election looming. These factors have inserted large amounts of uncertainty into the traders' minds. This is not to say traders or investors are right or wrong. They are simply two different breeds of people but they operate in very different ways. Right now lithium is unloved by traders but this might not always be the case. I foresee a future where lack of capex investment (now on the supply side), combined with lithium demanding projects (such as battery factories) coming online will create a lithium shortage. I do not know when this will happen but I do see many lithium demanding projects coming online between 2027-2030. For the short term what matters most is overall economic health in relation to lithium demand and the subsequent price of lithium. Lithium And Oil

Remember a few years back, when most oil stocks simply imploded? Great names in oil were being given away for near nothing. It was tempting to think "I'll buy some once I see it recover". Yet, the recovery took place and I missed out. Why? Because, like boiling water, it happened very slowly and then the opportunity was gone. I should have bought in the rough times and simply held. Parallels to oil aside, should we invest in lithium? I think the story is sound. Are some companies pulling back some on lithium investments? Yes. Are some advancing forward at a rapid pace? Absolutely. Let's compare the two and try to get a feel for what the big boys are doing on the demand side. Rising Future Demand For Lithium

We need to look at the big picture of future lithium demand. Who is investing capital into lithium and who is stepping back some. Note the bulk of links below are from 2024 unless noted. Here is some future demand to ponder.

$65 billion - The amount Honda plans to invest in EV over the next 10 years. Of which $11 billion is set for a Canada expansion this year.

As a reader you really need to let that sink in for a moment. As of May 16th, 2024 Honda is investing $65 billion into EV. Per Bloomberg:

Column 1

0

Supply chain security is a core concern and Honda said last month it will spend $15 billion (US$11 billion) to build one in Canada, where it will start producing EVs in 2028. The automaker aims to reduce EV manufacturing costs by about a third and bring down battery procurement costs by 20 per cent in North America, according to Mibe.The company said it’s positive on its ability to secure enough batteries to produce about 2 million EVs per year. Honda also needs to build an EV factory in Japan, Mibe said, without providing further details.About a fifth of Honda’s planned spending this decade will go toward research and development into software to improve mobility. The company joined fellow legacy marque Nissan Motor Co. to collaborate on technology including software as Japanese automakers look to claw back market share in China. Japanese firms have been losing ground to domestic EV makers that are viewed by discerning local consumers as better able to meet their specific tastes."

Moving on we see additional future lithium demand via:

$4.1 billion - Panasonic battery plant in Kansas continues development. (A German company also joined in for $100 million). This plant is set to open Q1 2025.

Volkswagen - $2 billion for an EV factory in South Carolina.

$1.6 billion - Asahi Kasei investment in a battery separation plant in Canada.

We also see lithium supply projects reducing mine expansions or lowering investments (aka lower capex). Again, this could cause a lithium supply crunch a few years down the road. We may even see some small miners sell off assets during the downturn.

Albemarle (ALB) - Is focusing more on organic growth as opposed to M&A growth. They are even deferring spending in NC as of January (but increasing spending in Arkansas via a pilot plant application for a pre-existing bromine facility).

"Albemarle said it now plans 2024 capital spending in the range of $1.6 billion to $1.8 billion, down from about $2.1 billion in 2023. The company also plans to defer spending on a massive U.S. lithium refining project in South Carolina that was designed to be one of the world's largest processors of the battery metal." - Source: Reuters

Lake Resources (OTCQB:LLKKF) is cutting back operations.

Evaluation of Arcadium Lithium

Pulling up a chart we see the stock has been ravaged the last year like most lithium stocks. Post merger the company has taken a -49.19% loss which is impressive in a terrible way. Source: Google Finance

Column 1

0

ALTM Performance (Google Finance)

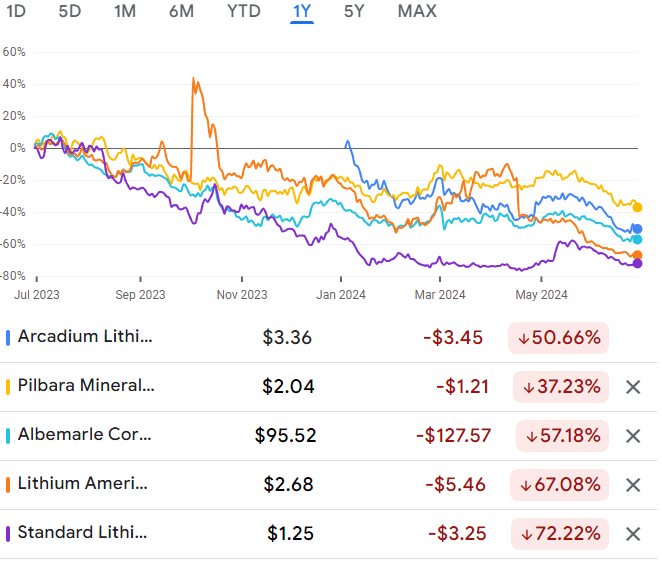

The share price destruction is on par with the industry though if we add other lithium companies to the chart.

Column 1

0

1 Year Sector Comparison (Google Finance)

If we look at ALTM we see a P/E ratio of 3.32 that stands out along with a market cap of $3.79 billion.

Column 1

0

ATLM Stats (Google Finance)

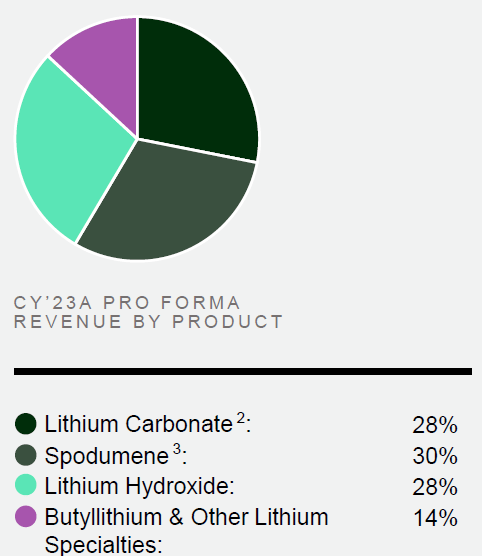

While product revenue is based around lithium it is interesting to see the types of lithium produced.

Arcadium Lithium Revenue Mix (Arcadium Lithium)

Arcadium CEO Paul Graves Speaks

Typically I try to avoid using long block of quotes but in this case you really need to read the views of Arcadium's CEO when he talks about the lithium market:

The supply chain is incredibly opaque for everybody, even for us, right? It's long. The signals being sent down the supply chain are off in the far distance, they're happening in Detroit or they're happening in Germany or even parts of China and they're not clear signals and so what we have is a supply chain trying to figure out we know that year-over-year growth in EV sales is about 20% to 25% still was in Q1 year-over-year was 25% higher year-over-year. So we know the growth is there, but there is a lot of confusion around technology roadmaps, there's a lot of confusion over IRA incentives, where Western Automotive are trying to build supply chains.

And so I think you've got the whole supply chain that's kind of a little bit frozen at the moment, and it's kind of sitting back waiting for clear signals about which way to go. I don't believe there was a massive destocking in lithium because I don't think there was ever a real big you know increase in inventory in the lithium space. I don't think we ever really saw in our supply chain customers with more than a couple of months of usable material on the shelves. So there wasn't really much they could do to destock. But what we're not seeing today is people producing cells, producing batteries, producing through the chain for next year's demand, which is what they typically would do. And so it's kind of a little bit frozen.

Now I think another interesting wrinkle, and this is why it's such an interesting, difficult industry sometimes to predict, is there is some pretty big geopolitical factors at work in my view. I think the US and Europe, and we saw it today with the tariffs in Europe, and we've seen it all through the IRA, if you flip it around and say in China, the message you're receiving is the Western world is trying to remove China's advantage in electrification, which is huge, right? It's a massive advantage in the entire supply chain. And the biggest weakness that China has, its Achilles heel, if you will, is it doesn't actually have any lithium resources of its own.

And so the simplest place, and maybe you could argue the same in other commodities, the simplest way to choke off China's leadership is to choke off the supply of raw materials. So not a surprise that they take what may appear to be economically irrational decisions, but are actually quite rational decisions to build their own captive supply chain to start processing very expensive Lepidolite, to start putting a lot of capital into a very inefficient supply chain in African Spodumene. This is really expensive stuff and but what the battery chain is saying in China, what the Chinese industry is saying is, we don't care that that is costing me $20 a kilo just to even make it myself, because I'm getting security of supply and I'm defending myself against some of these broader actions that the West is taking.

So I try and encourage people to not look at Lepidolite and not look at African Spodumene as supply that came into the market. Think about it more as demand that was taken out of the market by captively producing. China is basically saying I don't need to buy as much lithium. And that's where the oversupply comes from. And that's, look, it will correct. It always does. The growth rates are so high. I mean, total lithium demand in 2023 was where we thought it would be in 2025 when we did our IPO in 2018. So in the space of five years, we hit a seven-year target in five years, and it continues to grow at that rate. And it will get harder and harder for low-cost supply to come into the market.

We just think there's a natural tendency, there is a natural path upwards for the marginal producers' cost, and we think the price of lithium is will only creep up even from especially from where it is today. I don't think it'll go over $40. I don't think it'll stay below $20. I think it's just you look at the economics it's difficult to see how that happens." Arcadium Has Many Lithium Irons In the Fire

Looking over the various lithium projects Arcadium has it becomes apparent they can offer quite a mix of lithium chemicals to many geographic areas. In this section we are going to sort by the chemical produced. First off we have Lithium Carbonate production in Argentina.

Column 1

0

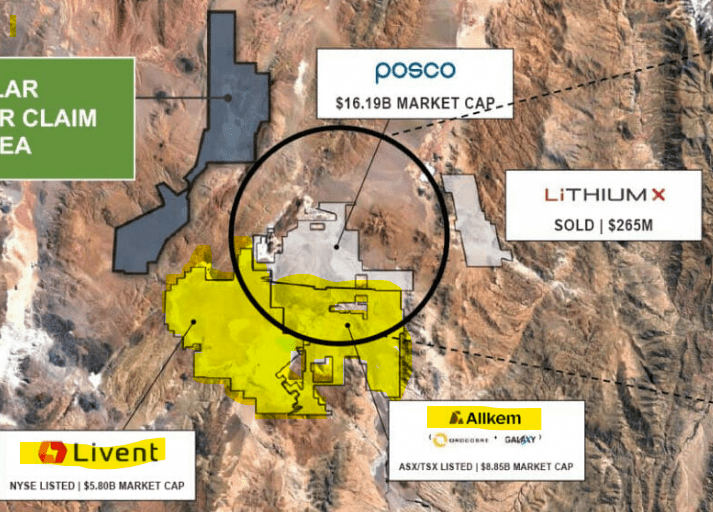

Lithium Carbonate: The 100% owned Fenix hombre Muerto. 66.5% owned Olaroz. 100% owned Sal De Vida. and lastly 100% owned Cauchari.

Here we can see some of the former Livent and Allkem properties in Argentina (noted in yellow) before they merged and became Arcadium Lithium. Do note the listed market caps in the picture below compared to Arcadium's current cap of $3.61 billion (at $3.30 a share). Quite the decline, yes? Quite the value play.

Alpha Lithium

Moving on we see:

Column 1

0

Lithium Hydroxide: USA - 100% owned Bessemer City. China - Rugao and Linhai Japan - 75% ownership in Naraha. Canada - 50% ownership, the Nemaska Lithium project (2 parts which is: Whabouchi and Bécancour.)

Ford And Arcadium Unite

Concerning the Nemaska project above, we see it has attracted a rather deep pocket partner in Ford (F). Per the CEO of Arcadium.

Column 1

0

Yeah, Nemaska's got 2 assets, as you know. There's the mine called The Whabouchi, and then there's the downstream hydroxide plant called Bécancour. Bécancour is the big capital commitment, over $1 billion of capital to build that. You talk about customer commitments, we've sold a very large proportion of the volume out of Bécancour to Ford. Ford made a long-term commitment to us and so kind of showed that the customers are there to support projects that they like. That project's completely on track. It's due to be completed in 2026. Takes six months or more maybe to ramp it up and get it producing, but we should have in volumes out of there by the end of 2026.

Lastly we have spodumene (hard rock):

Australia - 100% ownership in Mt. Cattlin and 100% ownership in Galaxy. Risk And Conclusion

Lithium stocks are at despondency levels. You might think of this as a reverse mania. Lithium is unloved, unwanted, and the entire sector is depressed. As a value investor I find this intriguing. Painful of course, but intriguing. Many great lithium stocks are on extreme discount. The risk however could be that lithium stays depressed for quite some time, maybe even years. Time value of money and inflation come into play. Also political risk is on the table. If Donald Trump wins the white house no one is really sure what he will do. Personally I think he loosen some of the environmental restrictions on cars.

Yet on the flip side Mr. Trump does have a business agenda. EV is the future and if the U.S. does not take leadership other countries like China will. Foreign legislation could make future ICE auto sales tougher and if the U.S. were unable to foster and cultivate a domestic EV production capability then the U.S. could find its auto industry severely hindered (and reduced to just the US market long term) vs foreign nations that do foster and build up an EV environment.

Pulling up the annual income statement we can see the income went up as lithium prices blasted north in 2022-23.

ALTM Income Statement (Google Finance)

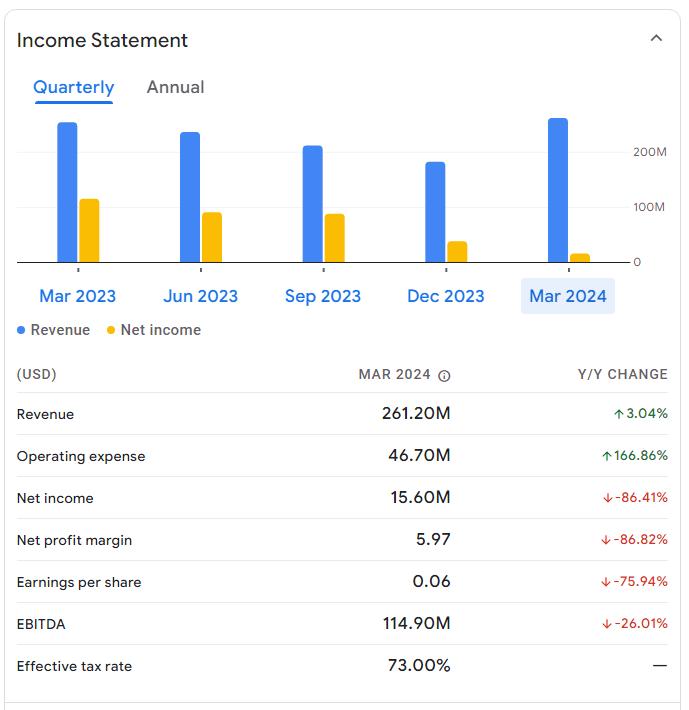

However, as lithium prices imploded to the $12-$20k range we can see the reduction in the quarterly income statement that includes 2024. This is reflected in the share price of a mere $3.36.

ALTM Income Statement (Google Finance)

Moving to the balance sheet we can see cash of $472.7 million and debt of $583.3 million.

Column 1

0

Arcadium Debt (Arcadium)

Given the net income implosion and sector decline, this might explain why the share price is so ridiculously low. Thus, can the company expand sales via bringing more production online? If lithium prices were to recover ALTM could rapidly improve. If not, they might have to delay or slow down expansions and to wait for favorable market conditions. I view the company as a buy for the investor with patience and who can maintain a degree of stoicism. I am increasing my position.

LTM Price at posting:

$5.36 Sentiment: Buy Disclosure: Held

ALTM Performance (Google Finance)

1 Year Sector Comparison (Google Finance)

ATLM Stats (Google Finance)

Arcadium Debt (Arcadium)

(20min delay)

(20min delay)