Wow not bad AL3

https://nextinvestors.com/articles/aml3d-asx-al3-our-tech-pick-of-the-year-for-2024AML3D (ASX: AL3) - Our Tech Pick of the Year for 2024

https://nextinvestors.com/articles/al3-announces-11m-sale-to-us-navy-supplier-us-traction-growingToday we are announcing our 2024 Tech Pick of the Year.

It’s been a while since we have added a new tech Investment.

We have looked at a lot of tech stocks over the last couple of years...

Our last “Tech Pick of the Year” was Oneview all the way back in 2021.

(and we haven’t seen a tech company we like enough since then).

(and due to this growth is currently our largest position).

Obviously we want to try to repeat this success with our next tech Investment.

... but remember that the past performance of Oneview is not an indicator that AL3 will do the same.

Today we add AL3 to our Portfolio as our 2024 Tech Pick of the Year:

AML3D

AL3 fits the same formula we had when we first Invested in Oneview.

Think of it like printing.. but with metal.

And the printed parts are harder, better, faster, stronger than traditional casting or forging.

(just the spot where we like to swoop in and Invest).

We especially like that AL3 has blue chip clients in:

The US NavyAustal (the ~$900M capped Australian shipbuilder)US oil & gas giant ChevronAnother US oil & gas giant - ExxonBAE Systems (the $77BN capped UK defence contractor)And Boeing.We also note that AL3’s new US expansion strategy is gaining traction surprisingly fast.

AL3 started its push into the US back in early 2023.

And the push is already yielding deals in the US...

The hub will help service AL3’s main deals in the USA...

The existing core of the sales pipeline for us is AL3’s deals with the US Navy.

AL3’s 3D printing system is called ARCEMY.

And AL3 received media attention and mentions in a couple of US defence publications:

It already appears that the US Navy is influencing its manufacturing suppliers to use AL3’s tech.

Here is what has happened in the last twelve months:

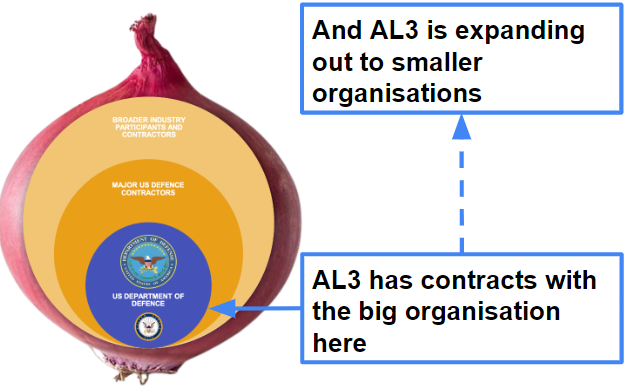

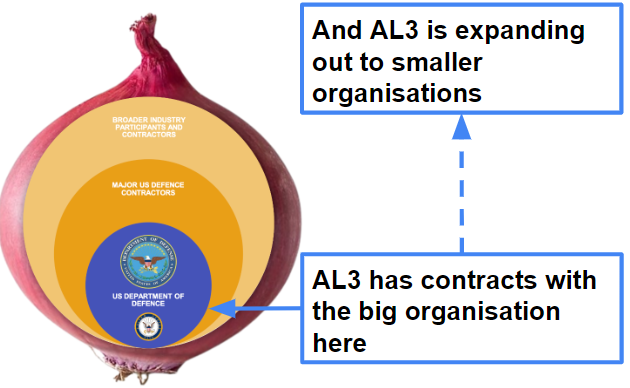

AL3 Enters US Defence Industry with ARCEMY Sale () - February 2023, this was the “seal breaker” deal that opened up the market for AL3. The US Department of Defence made its first purchase for the US Navy. They clearly liked what they saw...ARCEMY Ordered for the US Navy's Center of Excellence () - July 2023, a $1.1M order from the US Navy for its Additive Manufacturing Center of Excellence (AM CoE) in Danville, Va through the Philips value added reseller agreement, just four months after the first sale.US Navy Component Supplier orders AL3’s ARCEMY System () September 2023, this was a smaller dollar value of $270K to lease the product, but the first example of a smaller organisation following the lead of the US Navy.As Shrek once may have said, the defence supply chain is like a giant onion.

To do this though, printed product qualifications are very important.

Particularly for major organisations like the US Navy and other blue-chip customers.

These certifications are provided only after stringent testing and are not easily obtained.

This is through a US government program called AM Forward which was launched in 2022. ()

(“AM” stands for Additive Manufacturing, which is another way to say 3D printing)

Here are the heavy hitter companies that signed up to the AM forward program:

(some nice “onion centres” for AL3 to go after in this list)

This includes access to capital, purchase commitments and targets, training and research.

Why 3D printing now, and why AL3?

Again, AL3’s revenue is on course to ~10x over the last 12 months relative to last year...

The share price hasn’t moved...yet.

So we took the opportunity to Invest.

These are the basic components of what we think will substantially re-rate AL3:

More AL3 3D printing systems soldMore recurring software revenue attached to these system salesAccelerate US expansion (more US deals)Macro trend towards redomiciling manufacturing by adopting 3D printing(sometimes we get it right, sometimes we don’t and end up having to patiently hold for a while).

Also, the key changes we like in AL3’s strategy over the last two years are:

Switch focus to the giant US marketSell the entire 3D printing system, instead of AL3 just custom printing parts for customersAdding a recurring revenue component to the 3D printing system salesWith that in mind, here is our upside scenario for our AL3 Investment :

Our AL3 ‘Big Bet’:

Here are the 8 key reasons we Invested in AL3...

3D printing product at the forefront of manufacturing innovation - AL3 sells large scale modular 3D printing systems to industrial manufacturers. Its product, ARCEMY, provides a better solution to manufacturing parts for complex industrial machinery.Blue-chip client base including US Department of Defence - AL3 has a range of high-profile customers including the US Navy, US Department of Defence, Austal (the Australian military shipbuilder) as well as oil & gas giants Chevron and Exxon. These customers provide validation for AL3’s product in future sales as well as a network of potential smaller suppliers for AL3 to target.Tiny EV for AL3 with proven tech with sales - At 7.3c AL3 has a market cap of ~$22M, with ~$8M in the bank has an Enterprise Value of ~$14M. AL3 is already at ~A$6.6M in revenue for the first 9 months of FY24. AL3 has invested over ~$30M building out its tech.New sales strategy already driving revenue growth - AL3 has moved from a “sell the 3D printed parts” to a “sell the 3D printing system” strategy. This new strategy means bigger contracts for AL3 and gives customers what they want because the parts are made closer to where they are needed.“Sell the 3D printing system” strategy opens up yearly recurring revenue - For new orders of the ARCEMY system, AL3 will now build in ARCEMY services to include software and services fees on a recurring revenue basis. This includes software licensing fees, hardware maintenance, and tech support. This is an untapped stream of revenue for AL3 and a potential source of upside for the company as the company grows.Strong US focus as AM Forward Program rolls out - In 2023 AL3 commenced its US focused strategy. The US spends more on its defence than the next 9 countries combined and as such is easily the most lucrative defence market jurisdiction to operate in. In 2022, the US has also launched the AM Forward Program to support 3D Printing across the industrial manufacturing sector. We think that the US is the right place for AL3 to grow its business.US distribution partner Philips has proven its ability to sell AL3’s product - AL3 has a value added reseller agreement with ~$35BN capped Philips Corporation. Philips’s sales team has already helped AL3 make two US sales, including an ARCEMY sale to the US Navy Centre of Excellence which we see as the first signs that Philips is an engaged partner and we expect their sales team to help drive the marketing of AL3’s products.US Navy to help to push AL3 to its parts suppliers - the early signs are there. We want to see AL3 expand into smaller US Navy parts suppliers who are following the US Navy’s lead. In September 2023, a Navy parts supplier called Laser Welding Solutions leased the ARCEMY product from AL3 - we hope the first of many contracts for AL3 from this type of smaller organisation.So how exactly does AL3’s tech work?

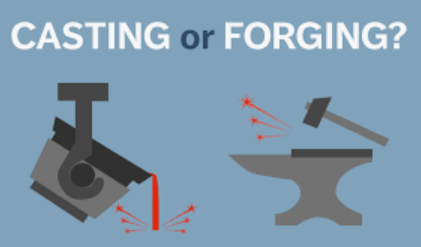

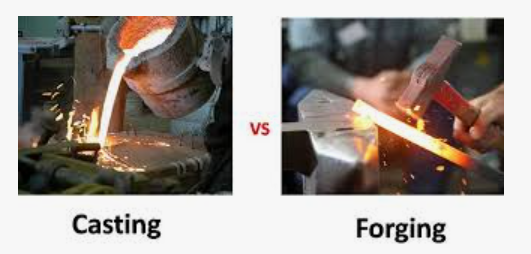

3D printing is not a new technology.

Traditionally, industrial parts are created using a technique called “casting” or “forging”.

(sort of like medieval blacksmiths you see in the movies).

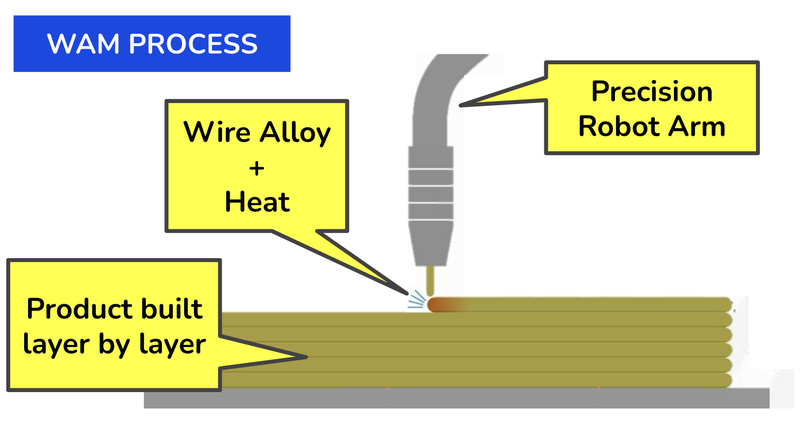

AL3’s technology on the other hand uses a system called Wire-arc Additive Manufacturing (or WAM).

This video shows the WAM process in action:

What are the benefits to users of AL3’s 3D printing system?

AL3’s 3D printing is better in almost every way than traditional “casting” or “forging”...

The 3D printed parts are harder, better, faster, stronger.

AL3’s tech can make parts up to:

75% faster than forging or casting30% stronger than a cast or forged part50% more resistant to metal fatigue95% less material waste costsHow does AL3 make money?

(we are big fans of yearly recurring revenue growth)

ARCEMY 3D Printing system sales: ARCEMY is the name of AL3’s 3D printing system that customers can use to 3D print desired parts on site. These sell for between $1M-$2M and are big contracts.ARCEMY software & services recurring yearly fees: For customers that have purchased an ARCEMY 3D printing system, AL3 provides annual support through maintenance, product support and a software licensing that enables customers to use the facility. This is the Annual Recurring Revenue (ARR) side of the business.Manufacturing Deals: AL3 sells specific 3D printed parts to various organisations. These sales contracts are generally smaller and proof of concept that will hopefully lead to repeat business. Product testing and certifications expand the library of products that AL3 can sell in this way.As we mentioned, before late 2022 AL3 was mainly focused on “manufacturing deals”.

(essentially doing the 3D printing themselves in one-off custom contracts to various customers).

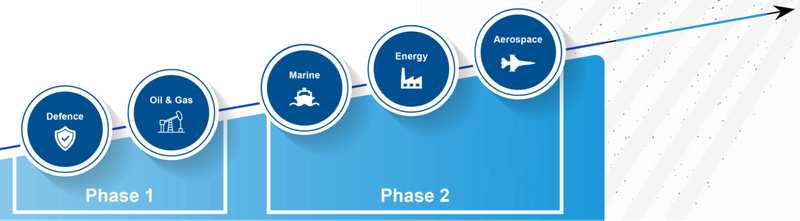

Who is already using AL3 and who is the target market?

DefenseOil & Gas / Mining ServicesMarineEnergyAerospaceIn this calendar year the company has already secured ~A$12M in contracts and purchase orders.

This $12M in contracts has been split between sales of the ARCEMY and Manufacturing Deals:

It would be great to see some of these manufacturing contracts convert to an ARCHEMY sale.

How big is the market AL3 is going after?

The market size for AL3 is big and set to grow even bigger.

It is currently US$2.6 billion and forecast to grow at a CAGR of ~20% through to 2030:

How will AL3 capture a share of this market?

There are a number of key ways in which we see AL3 growing its revenue:

Direct sales - “in-house” sales from an expanding US sales team and opening a local manufacturing facility in Ohio (expect in the next 3 months)Philips partnership - a value added reseller agreement to drive US deals with a large US team and contact network to help make Philips a leader in 3D printing (already has demonstrated sales traction)Big organisations push suppliers to use AL3 - the US Navy clearly likes the product and smaller parts suppliers should follow the US Navy’s lead. Early signs of traction and we hope to see more Navy parts suppliers adopt AL3.AM Forward Program - AM Forward provides funding and tax incentives for smaller organisations to take up additive manufacturing technology like AL3’s and we want to see this reflected in more widespread adoption from parts suppliers in the US industrial base.Investment Memo: AML3D ()

What does AL3 do?

What is the macro theme behind AL3?

Why did we Invest in AL3?

3D printing product at the forefront of manufacturing innovationBlue-chip client base including US Department of DefenceTiny EV for AL3 with proven tech with salesNew sales strategy already driving revenue growth“Sell the 3D printing system” strategy opens up yearly recurring revenueStrong US focus as AM Forward Program rolls outUS distribution partner Philips has proven its ability to sell AL3’s productUS Navy to help to push AL3 to its parts suppliersWhat do we expect the AL3 to deliver?

Objective #1: Hit $12M in revenue

According to the March quarterly AL3 will hit ~$7M revenue for FY24

We think that if they can back that up with beating $12M revenue in FY25 it would be a huge result.

Objective #2: More sales of ARCEMY

We want to see AL3 sign more large contracts via sales of their ARCEMY system (3D printing system).

New ~$1M contract (New customer in US defense industry)

New ~$1M contract (New customer in non-US jurisdiction)

Objective #3: Prove recurring revenue from ARCEMY Services Deals

AL3 has built a recurring revenue component into its business model.

Add new recurring revenue of $500K

Add new recurring revenue of $1M

Stretch target: Add new recurring revenue of $1.5M

Objective #4: More sales from manufacturing and prototype deals

In addition to the ARCEMY product, AL3 sells specific 3D printed parts to various organisations.

Product testing and certifications expand the library of products that AL3 can sell in this way.

5 new manufacturing / prototype deals

10 new manufacturing / prototype deals

What could go wrong?

Sales risk

Partner risk

Funding and dilution risk

Technology and Intellectual Property risk

Key personnel risk

Accreditation risk

Market risk

What is our Investment Plan?

AL3 announces $1.1M sale to US Navy supplier - US traction growing

An early, strong start to the new financial year.

And hopefully AL3 can keep up this momentum.

We announced AL3, as our newest Investment last week.

What got us most interested in AL3 was its change in sales strategy towards:

Switch focus to the giant US marketAdding a recurring revenue component to the 3D printing system salesSell entire 3D printing systems, instead of AL3 just custom printing parts for customersAnd today, AL3 announced a $1.1M deal to back up the strategy change.

And there is potential for AL3 to do it again with the same customer...

Here is what an ARCEMY system looks like:

And here is the system in action:

How this announcement impacts our AL3 Investment Memo:

We think today’s deal is important news for the company for three key reasons:

1. High $ value relative to full year revenues

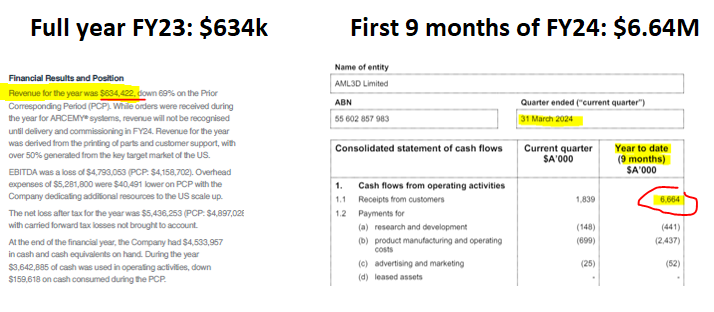

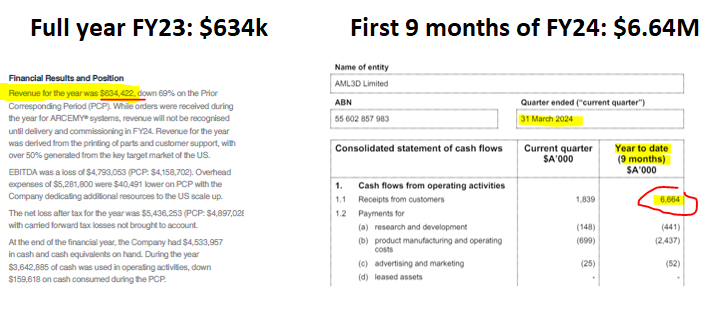

AL3 had $634K in revenues for FY23 and ~$6.64M in cash receipts for the first 9 months of FY24.

The $1.1M deal is material relative to both of those numbers.

So it’s a good early start so far to the revenue objectives we want to see AL3 deliver in FY25.

2. Large upfront capital commitment from inside the US Defence industry

It also validates the AL3 strategy of selling into a larger subsector of the defence industry.

3. Outright purchase + service/maintenance revenues attached to the deal

New sales strategy already driving revenue growth

AL3 has moved from a “sell the 3D printed parts” to a “sell the 3D printing system” strategy. This new strategy means bigger contracts for AL3 and gives customers what they want because the parts are made closer to where they are needed.Source: AL3 Investment Memo 27 June 2024The new sales strategy means AL3 is able to sign deals that are as big as ~$1.1M.

So future sales of bigger systems could mean deal sizes even bigger than the $1.1M announced today.

“Sell the 3D printing system” strategy opens up yearly recurring revenue

For new orders of the ARCEMY system, AL3 will now build in ARCEMY services to include software and services fees on a recurring revenue basis. This includes software licensing fees, hardware maintenance, and tech support. This is an untapped stream of revenue for AL3 and a potential source of upside for the company as the company grows.Source: AL3 Investment Memo 27 June 2024Up until March 2024, the company’s business model didn't have a recurring revenue component.

US Navy to help to push AL3 to its parts suppliers

The early signs are there. We want to see AL3 expand into smaller US Navy parts suppliers who are following the US Navy’s lead. In September 2023, a Navy parts supplier called Laser Welding Solutions leased the ARCEMY product from AL3 - we hope the first of many contracts for AL3 from this type of smaller organisation.Source: AL3 Investment Memo 27 June 20248 Key reasons why we Invested in AL3:

3D printing product at the forefront of manufacturing innovation - AL3 sells large scale modular 3D printing systems to industrial manufacturers. Its product, ARCEMY, provides a better solution to manufacturing parts for complex industrial machinery.Blue-chip client base including US Department of Defence - AL3 has a range of high-profile customers including the US Navy, US Department of Defence, Austal (the Australian military shipbuilder) as well as oil & gas giants Chevron and Exxon. These customers provide validation for AL3’s product in future sales as well as a network of potential smaller suppliers for AL3 to target.Tiny EV for AL3 with proven tech with sales - At 7.3c AL3 has a market cap of ~$22M, with ~$8M in the bank has an Enterprise Value of ~$14M. AL3 is already at ~A$6.6M in revenue for the first 9 months of FY24. AL3 has invested over ~$30M building out its tech.New sales strategy already driving revenue growth - AL3 has moved from a “sell the 3D printed parts” to a “sell the 3D printing system” strategy. This new strategy means bigger contracts for AL3 and gives customers what they want because the parts are made closer to where they are needed.“Sell the 3D printing system” strategy opens up yearly recurring revenue - For new orders of the ARCEMY system, AL3 will now build in ARCEMY services to include software and services fees on a recurring revenue basis. This includes software licensing fees, hardware maintenance, and tech support. This is an untapped stream of revenue for AL3 and a potential source of upside for the company as the company grows.Strong US focus as AM Forward Program rolls out - In 2023 AL3 commenced its US focused strategy. The US spends more on its defence than the next 9 countries combined and as such is easily the most lucrative defence market jurisdiction to operate in. In 2022, the US has also launched the AM Forward Program to support 3D Printing across the industrial manufacturing sector. We think that the US is the right place for AL3 to grow its business.US distribution partner Philips has proven its ability to sell AL3’s product - AL3 has a value added reseller agreement with ~$35BN capped Philips Corporation. Philips’ sales team has already helped AL3 make two US sales, including an ARCEMY sale to the US Navy Centre of Excellence which we see as the first signs that Philips is an engaged partner and we expect their sales team to help drive the marketing of AL3’s products.US Navy to help to push AL3 to its parts suppliers - the early signs are there. We want to see AL3 expand into smaller US Navy parts suppliers who are following the US Navy’s lead. In September 2023, a Navy parts supplier called Laser Welding Solutions leased the ARCEMY product from AL3 - we hope the first of many contracts for AL3 from this type of smaller organisation.Check out our deep dive into AL3 from last week here:

Our AL3 ‘Big Bet’:

How today’s news impacts our Investment Memo objectives for AL3:

Objective #1: Hit $12M in revenue

According to the March quarterly AL3 will hit ~$7M revenue for FY24. We think that if they can back that up with beating $12M revenue in FY25 it would be a huge result.Source: AL3 Investment Memo 27 June 2024Objective #2: More sales of ARCEMY

We want to see AL3 sign more large contracts via sales of their ARCEMY system (3D printing system).

AL3 already has good traction with the US Navy via the US Department of Defence and we also want to see an expansion in jurisdictions and industries.

It also has a value added reseller agreement with ~$35BN capped Philips Corporation which has a large reach in the US

Milestones

total 8x new ARCEMY contracts (✅)

New ~$1M contract (New customer in US defense industry)

New ~$1M contract (Aerospace)

New ~$1M contract (O & G)

New ~$1M contract (New customer in non-US jurisdiction)Source: AL3 Investment Memo 27 June 2024Objective #3: Prove recurring revenue from ARCEMY Services Deals

AL3 has built a recurring revenue component into its business model.

For each client that purchases the ARCEMY facility, AL3 has built in ongoing fees for providing ongoing support which includes software license fees of $150K a year, hardware maintenance fees of $50k a year, and tech support of $50k a year.

Milestones

Add new recurring revenue of $500K

Add new recurring revenue of $1M

Stretch target: Add new recurring revenue of $1.5MSource: AL3 Investment Memo 27 June 2024To see all the other objectives we want to see AL3 achieve check out our .

What are the risks?

Every investment carries risk. An investment in AL3 is no different.

In the short term, the key risks we are conscious of for AL3 are “Sales risk” and “Market Risk.”

We mention several other risks as part of our AL3 Investment Memo, including:

Partner riskFunding and dilution riskTechnology and Intellectual Property riskKey personnel riskAccreditation riskTo see our key risks expanded check out our .

Our AL3 Investment Memo:

In our , you can find the following:

What does AL3 do?The macro theme for AL3Our AL3 Big BetWhat we want to see AL3 achieveWhy we are Invested in AL3The key risks to our Investment ThesisOur Investment Plan

Wow not bad...

Add AL3 (ASX) to my watchlist

(20min delay) (20min delay)

|

|||||

|

Last

16.5¢ |

Change

0.005(3.13%) |

Mkt cap ! $62.55M | |||

| Open | High | Low | Value | Volume |

| 17.0¢ | 17.0¢ | 16.0¢ | $153.3K | 913.2K |

Buyers (Bids)

| No. | Vol. | Price($) |

|---|---|---|

| 4 | 1808399 | 16.5¢ |

Sellers (Offers)

| Price($) | Vol. | No. |

|---|---|---|

| 17.0¢ | 103000 | 1 |

View Market Depth

| Last trade - 16.10pm 18/10/2024 (20 minute delay) ? |

| AL3 (ASX) Chart |