Borrowed from another thread, a good read

Lithium Investing: Chinese EV Growth Drives Investment In The Lithium Industry

Jan. 11, 2018 1:18 PM ET

|

4 comments

|

Includes:

BYD

,

F

,

FMC

,

GM

,

ILHMF

,

LACDD

Livio Filice

Long-term horizon, Growth, momentum, Deep Value

(767 followers)

Summary

Chinese government mandates 8% new energy vehicles in 2019; 10% 2020.

Battery manufacturers have moved to increase output to meet growing demand.

Tight supply of lithium carbonate has increased prices in China to $18,000 T LCE.

Chinese companies have moved to acquire lithium assets in Argentina to secure supply.

Looking to 2018 and beyond, it is clear that China will play a critical role in advancing the electric vehicle industry as the political landscape is forcing a change within the automotive industry. At the highest level, the government continues to implement policies that will force automakers to offer electric vehicles or purchase credits from other automakers to ensure they are compliant with new standards. These policies have activated a number of events throughout the supply chain, which are assisting to shape the demand for various components required for the building of the lithium batteries that are now in high demand. In December 2017, the Chinese government extended a credit that returns up to 10% of the purchase price back to buyers.

The policy shift towards the widespread adoption of electric and plug-in hybrid vehicles in China has begun to place pressure on the lithium supply chain, which has propelled investment in the space. In December 2017, Ford (NYSE:

F

) announced a major expansion plan that will see the company offering 15 electric vehicles in China starting in 2019.

GM

(NYSE:

GM

) will meet the mandates by offering five crossovers, two minivans, and seven SUVs within the next 18 months and will expand to include 18 electric vehicles over the next five years. The company has disclosed that it is purchasing battery cells at $145 per kWh with a vision to bring pricing below $100 per kWh. Battery cells are packaged to form battery modules, which are then managed by an intelligent battery management system. In 2016, sales of electric vehicles reached a total of

336,000

units and it is estimated to increase to 800,000 in the next few years. China, in the near future, will be the largest global market for new energy vehicles.

Chinese domestic pricing for lithium carbonate reach $18,000 T LCE

In direct response to these events, the price of lithium carbonate has risen from $5,000 T LCE in recent years to around $13,000 T LCE in CYQ4 2017 (See:

Lithium Prices Reach Record High In China

). It is my opinion that the current trends in the Chinese domestic automotive business are going to continue to be a driver for increasing demand for lithium carbonate, which is already in tight supply. The strong emerging demand from China will ensure that prices remain exceptionally strong until new supply enters the market. If new lithium supply enters the market, it is still unclear when it could arrive, at what chemical grades or the amount of supply that is forthcoming. Therefore, based on strong underlying policies in the Chinese automobile industry, I believe that demand for lithium carbonate will be in a short position until new, meaningful supply arrives into the market, which will likely not occur until after the end of the decade. Until then, battery manufacturers will expand production capacity, requiring a buildup of activity throughout the supply chain, including stockpiling of lithium carbonate, to ensure the material manufacturers have sufficient levels of supply to keep production lines operational. Inherently, this will put pressure on non-Chinese battery manufacturers to move to secure lithium supply and will drive outside China sales contracts to match inside China sales contracts, meaning that lithium carbonate prices will likely continue to climb to $18,000 T LCE.

This will directly translate into higher selling prices for the few lithium carbonate producers, leading to a higher gross margin per tonne produced and significantly higher profit margins. This will certainly translate into higher stock prices for key lithium producers, which will assist in further propelling shares higher in 2018 and well into 2019 (See:

Lithium Mining: Understanding The Emerging Supply Landscape

). For junior lithium exploration companies that have good properties, with strategic partners in place to assist with bringing projects to commercial production, they will be able to recognize higher values for their assets. In 2017, the market valued in-ground brine deposits at around 10% of market values of LCE, so a higher market value for finished goods will translate into higher valuations for in-ground assets. Based on the above thesis, it would be possible for advanced junior lithium exploration companies to be valued at around $1,800 T LCE in ground in 2018.

China: 10% of sales from new energy vehicles in 2019; 12% by 2020

In late

Q3 2017

, China announced that it would delay the new regulations around the introduction of new energy vehicles but would increase the mandates for 2019. The original mandate was for automakers to produce an 8% quota in 2018, which has been delayed by one year. The auto industry in China pushed back as they knew they would not be able to meet the 2018 requirements, which was obvious considering that strategic material, such as lithium, is currently in tight supply and battery manufacturers had not added enough production capacity in the past years. Now, automakers that produce more than 30,000 vehicles per year will need to have 10% of their sales coming from new energy vehicles in 2019, with the rate increasing to 12% by 2020. Automakers that are not able to meet the quota will have to acquire credits from other companies. Fortunately, there is an increase of lithium carbonate coming from Argentina and Chile, while Australian companies have done well to increase concentrates being shipped to China for processing (See:

Lithium Investing: All Roads Lead To Argentina

).

According to

BYD

(OTCPK:

BYD

), a major Chinese battery and automotive manufacturer, the 2019 requirements are only a reflection of the total potential of the Chinese new energy vehicle market. BYD believes there is a possibility that all vehicles in the country could be electrified by 2020, including a range from full electric to hybrid.

In the month of

September 2017

, total passenger vehicle sales in China amounted to 2.71 million units. In the short term, even the 10% requirement for new energy vehicles would represent monthly sales of around 200,000 electric vehicles, with some targets

suggesting

2 million annually. To compare, in the first six months of 2017, the entire American new energy vehicle market amounted to 103,000 units. This clearly illustrates that China will remain the leader in this market and will create the baseload demand for the lithium battery supply chain.

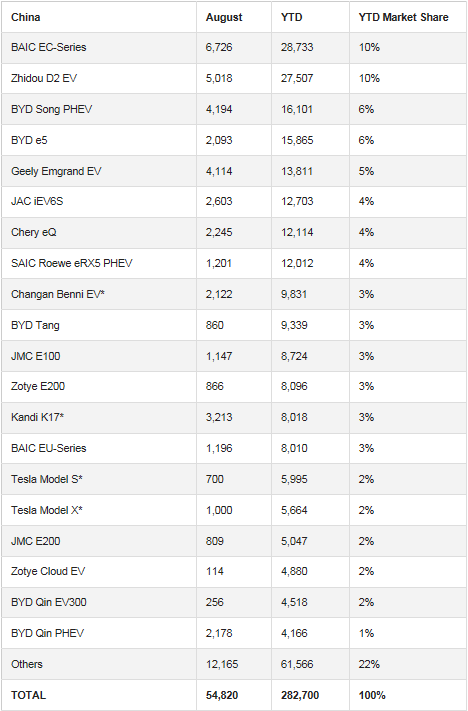

China EV & PHEV sales total 282,000 in CY H1 2017

Chinese battery manufacturing capacity is expanding

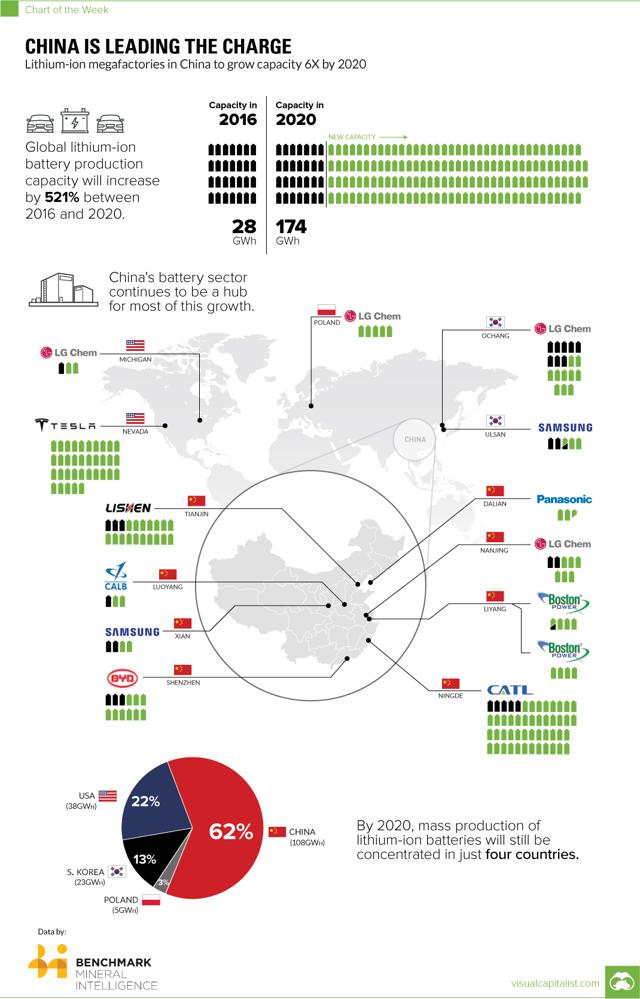

China's battery manufacturing capacity is

presently being increased

to ensure that production is available to meet the growth from the automotive industry. CATL is a leading domestic lithium battery manufacturer with a total production capacity of 7.7 GWh, with plans underway to increase output to 50 GWh annually. In Q4 2017, the company

disclosed

plans to undertake an IPO valued at $2 billion to fund the expansion efforts. BYD, which builds a wide array of advanced products such as electric buses, cars, and batteries, has 20 GWh of battery cell capacity and is China's largest battery maker. The growth in battery manufacturing capacity will ensure that the Chinese industry is competitive enough to win international business over Japanese and Korean rivals. These major undertakings will also lead to battery prices dropping below the $100 per kWh price, which will contribute to the success of secondary applications such as stationary energy storage systems and electric buses. The chart below

illustrates

the rapid growth in lithium battery production in China, which will assist with global production as it increases from 28 GWh in 2016 to 174 GWh in 2020. Panasonic (OTCMKTS:

PCRFY

), LG Chem (OTCMKTS:

LGCLF

), Boston Power, CATL, LISHEN, CALB, BYD, and Samsung (OTCMKTS:

SSNLF

) are all presently increasing production capacity within China.

Beyond Chinese companies, LG Chem has

recently

opened a production facility in China to supply 50,000 electric vehicles or 180,000 plug-in hybrid vehicles. LG has secured 16 carmakers as customers for the company's batteries. Even automotive companies, such as BMW, have

announced

a domestic presence to assemble battery packs to meet demand from their automotive business.

Material sourcing through strategic investment

Sometimes the simplest way to secure a strategic material or component is through acquisition of select targets. It came as no surprise that, in 2012, Talison Lithium Ltd.

announced

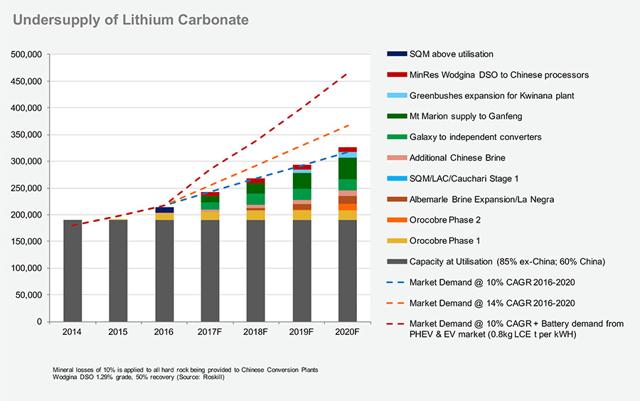

it was being acquired by China's Chengdu Tianqi Industry Group Co., Ltd. in an all-cash transaction that valued Talison at approximately $848 million on a fully diluted basis. Talison Lithium Ltd. owns and operates the Greenbushes hard-rock mine in Australia and is amongst one of the top lithium producers globally. Based on the "Undersupply of Lithium Carbonate" graph, the Greenbushes is undergoing an expansion that is expected to be fully operational by 2020, assuming no delays.

As illustrated in the graph above, the Chinese lithium producers from brine are not going to contribute in a significant way to the overall global supply of lithium carbonate. This will certainly lead to additional transactions in the lithium brine space, which will likely occur in Argentina. One trend that will occur is direct investment from Chinese firms into companies that are actively exploring and developing projects in the Lithium Triangle. If China actually wants to increase their outlooks to 100% new energy vehicles by 2030, then the necessary investments will need to take place throughout the entire lithium supply chain including greenfield lithium brine projects, which take nearly half a decade to bring to market. This will not be a new trend, but an ongoing series from existing events.

The most notable event from China was an investment from Ganfeng Group into Lithium Americas (OTCPK:

OTCQX:LACDD

), which will finance the construction of their lithium brine project in Northwestern Argentina. For those unfamiliar the

Ganfeng Group

, it was established in 2000 and has grown to become the largest integrated lithium producer in China. Today, the company has a total capacity of around 30,000 tonnes per annum of LCE. Ganfeng's products include lithium metal, lithium hydroxide, lithium carbonate, lithium fluoride, and lithium chloride. Ganfeng Lithium is listed on the Shanghai stock exchange with a

quoted

market capitalization of around $60 billion. Most recently, the company

announced

plans to invest $30 million into the construction of a next-generation, solid-state lithium battery facility in China.

Lithium test ponds at Cauchari (November 2017 Lithium Tour)

In 2017, Ganfeng and Lithium Americas reached a financial

agreement

that will see Ganfeng invest over $190 million into the Cauchari basin to build out the necessary plant and property in exchange for around 19% of the outstanding shares of Lithium Americas. The funds were made available through two financial vehicles: the first was a private placement for around $50 million and the second was a $125 million project debt facility, which will allow Lithium Americas to quickly move into construction in 2019.

Ganfeng is also working on another Argentine lithium brine project in partnership with the microcap lithium exploration company, International Lithium (OTCPK:

OTCPK:ILHMF

). In April 2017, the company's reported

maiden resource estimate

for the Mariana lithium brine project showed an estimated 749,000 T LCE at a 60% recovery rate. The project is now moving toward the completion of a preliminary economic and pre-feasibility study.

Another scenario that will become increasingly popular over the next few years is direct investment into junior lithium exploration companies. NRG Metals (OTCMKTS:

NRGMF

), a recent start-up focused on the development of lithium brine assets in Argentina, has recently attracted a Chinese battery material producer through closing on a $1.4 million private placement to fund ongoing exploration activities in Argentina and the potential, as an Off-Take producer, for future lithium products extracted. NRG Metals has two projects, with the most significant project being the "Homebre

Muerto North Project"

or HMNP. HMNP is located in the Salta and Catamarca provinces and comprises a total property package of over 3,000 hectares encompassing six concessions. The company has

reported

good surface sample collections, magnesium to lithium ratios, and is located across from Galaxy Resources (OTCMKTS:

GALXF

) Sal de Vida lithium development project. Most importantly, the project is within 20km of FMC Corporation's (NYSE:

FMC

) well established

Fenix lithium brine project

.

Junior lithium plays provide maximum exposure

Blue chip chemical companies such as SQM and FMC will provide some exposure but investors looking to take more risk within the space should consider junior lithium exploration companies. Although there is significant risk to the space, there is a large number of publically traded junior lithium exploration companies primarily focused in Argentina. In December 2017, Lithium X (OTCMKTS:

LIXXF

), a junior exploration company operating in the Northern Argentine province of Salta, was

acquired

for over $250 million in an all-cash deal by NextView. NextView has established a US$1.5 billion nature resource fund to acquire overseas mining assets with a focus on the new energy and resource sectors. Considering that there are only a handful of low cost lithium producers in the world, it is not surprising that NextView acquired an advanced junior exploration company in the prolific Lithium Triangle district of Argentina. It could be possible for Chinese and other Asian companies to acquire additional resource exploration companies as the demand for the white metal becomes increasingly important to the Chinese automotive business for reaching their targets. In addition, should the Chinese not have direct access to low-cost, high quality lithium supply then they will be fighting with the Koreans and Japanese as they also seek out supply security.

In addition to my holdings in Orocobre, Advantage Lithium (OTCMKTS:

AVLIF

) has been a company that I have championed for the past months. Advantage Lithium is a junior lithium exploration company that is actively advancing their flagship Cauchari project, which straddles the boundaries of Orocobre and Lithium Americas. Over the past few months, the company has been actively reporting their drill results, which indicate a strong lithium deposit at Cauchari. Shares in the company have experienced a dramatic increase but I believe there is still significantly more upside in the company's share price. In a previous document, I outlined why I have taken a position in the company and continue to peg a mid-term share price of around $1.90 - $2.00 per share. Considering that Orocobre and Lithium Americas have successfully been able to draw investment into the region, there is a high probability that other players are looking to enter the basin, which would place Advantage Lithium under the spotlight.

If you enjoyed this article than be sure to receive future material by clicking on the "Follow" tab at the top of this page or on my profile at:

here

.

Disclosure:

I am/we are long OROCF, AVLIF.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

(20min delay)

(20min delay)