There has been some decent discussion on here wrt BEOT accumulating or re-accumulating. Reviewing all the credible Lit plays, trading volumes are pitiful atm, thus trading ranges are tight. I have know idea when this slow grind will finish, and obviously in a low volume environment, its will take the BEOT longer to accumulate their fill. I know its frustrating, that's exactly what our enemy want's.

There has been so much hype, pushing all the battery metals to highs, it was frothy, and thus needed to consolidate. However, over the past few weeks, the bubble has burst for some of those battery material hopefuls, which has created a lot of noise, and because the battery supply chain is relatively new and not well understood, that noise has spread across the overall chain. While said noise relates to nickel and to a lesser extent copper, it seems lithium sentiment is being dragged down with those two metals, but certainly not because there has been a change in fundamentals, as they remain strong.

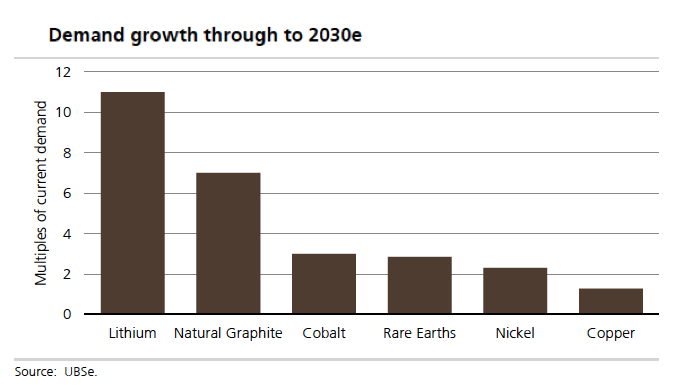

So, in case you have forgotten why you initially invested in the lithium sector, please take a deep breath and soak up what's coming over this decade, courtesy of UBS revised forecasts. I have added my 2 cents, in blue text;

UBS upgraded its already rosy forecasts, which were only made last November, and the bank is now among the most bullish on EV penetration and battery raw material demand through 2030:

- EV adoption rate is upped from 17% to 20% by 2025 (~18 mill EV units) and from 40% to 50% in 2030 going from just over 3m vehicles last year to 46m. Note this is just EV lithium consumption, thus EV battery grade lithium needs to more than triple in the next 4 years, then grow by 150% again by 2030.

- Average battery size is forecast to increase from 47kWh to 94kWh in 2030 as full electric cars take over from hybrids and range requirements increase. When the pick up truck and semi trucks are properly addressed across all market segments, is quite possible the battery pack size in road transport will rise to an average of 94kWh, or 78kg of lithium per vehicle. That's 3.58 mill tonnes of EV battery grade lithium in 2030 (i.e. 46 mill EV's x 78kg / 1,000)

- “Cost parity of BEV’s with ICE equivalents is now in sight”: Battery pack costs to ~$70/kWh by 2025 is achievable on cheaper cells and better pack integration. No arguments from me.

- Lithium-ion battery demand jumps 17-fold to 4,605 GWh by 2030 with energy storage making up around 6% of the total. 4.605twh includes all batteries apps, phones, tools, EV's, etc. checks out.

- Overall lithium demand to lift 11-fold from ~400kt in 2021 through to 2030 by which time batteries will account for 94% of demand, from half now. “Industry feedback tells us that the most we could expect in recycled lithium by 2030e is ~80kt LCE”. Good Luck to the EU, they'll need it, if world will be fighting over 80kt of recycled LCE units in 9 years time.

- Natural graphite demand grows by a factor of seven by 2030 (assuming 45% synthetic graphite into the anode and “conservative view” of silicon use) to roughly 5.9mt

- Demand for nickel grows from ~2.6mtpa now to 5.8mtpa by 2030. “Overall battery demand for nickel is somewhat offset by an increase in our estimate of LFP chemistry into the cathode mix”. Nickel price forecast lifted to $9.00/lb ($19,840/t) in 2023 before returning to $6.00/lb by 2025, “based on a break-even price for HPAL production which we view as the marginal cost of production long term. We think that China’s battery/automotive industry will invest in large scale HPAL capacity in Indonesia over time to secure nickel units and do so with little regard to returns.”

- Neodymium (Nd) and praseodymium (Pr) face “a step change” in demand from ~30ktpa now towards ~100ktpa in 2030 with EVs representing some 80% of the total.

- NdPr price forecast to peak at $100/kg in 2024 to reflect the “looming deficit and rising supply anxiety,” before returning to ~$70/kg by 2027, a greenfields incentive price. “The NdPr price spiked beyond US$100/kg in 2011 in part due to a reduction in exports from China at that time. This supply shock remains a real risk too.”

- Cobalt demand to expand by ~13% over the next decade from around 120ktpa to over 400ktpa by 2030 “partly offset by a migration to lower cobalt battery chemistries (LFP,NCA, NCM 811) with the average cobalt content on an EV falling by ~50% by 2030.” 2021 cobalt price forecast upped by 45% and 2022–25 forecasts by 14% to roughly $25/lb in line with the long-term average price since 1950 and the incentive price for cobalt mines to be built outside the DRC. A deficit of ~170kt of cobalt by 2030. This equates to some 10 “large” cobalt mines in the DRC (producing 15-20ktpa like Katanga, Mutanda, Tenke, RTR or Mutoshi).

- By 2030, copper consumption in EVs (avg 90kg vs 20kg in ICE vehicles) will represent 4.4mt of copper demand or around 13% of the total. That represents growth of around 3% per year – above the long term historic trend of 2.4% CAGR (1976-2019).

(20min delay)

(20min delay)