This paper, originally published in the Bayes Business School's Commodity Insights Digest, explores the performance and trajectory of the lithium futures market, which emerged to manage price volatility in the booming lithium industry

The global shift towards net zero emissions has significantly increased demand for traditional commodities and created new markets, particularly within the battery supply chain supporting electric vehicles and energy storage systems. This paper explores the performance and trajectory of the lithium futures market, which emerged to manage price volatility in the booming lithium industry.

Lithium futures, first launched on major global exchanges in 2021, have shown a pattern of growth akin to early iron ore futures markets. Initially, the market saw significant volatility, with spot prices fluctuating drastically.

Despite this, traded volumes and open interest in lithium futures have gradually increased, peaking in mid-2024, indicating growing market adoption and liquidity. A key challenge for the lithium market is achieving a level of liquidity observed in mature commodity markets.

However, for a very young market there are signs that lithium futures are on the right path to becoming a liquid futures market. Increasing participation, a more developed forward structure and multiple types of contracts available are all positive signs of a maturing market. Introduction

The global race to net zero has boosted demand for many traditional commodities and given rise to new markets. From environmental commodities through alternative fuels to metals and minerals, we are witnessing a change that commodity markets have not seen in decades. With this shift in the physical markets comes a raft of challenges and opportunities for financial commodity markets.

A key theme of the energy transition is the exponential growth of the battery supply chain supporting the electrification of the industry, predominantly in the electric vehicle and energy storage system space.

The lithium futures market is one of the newest markets that have emerged because of the booming battery supply chain.

In this paper I examine the performance of lithium futures since their launch in relation to markets that have certain similarities, as well as commodity futures that can help us assess the possible trajectory lithium futures may take in the coming years. The birth of lithium futures

Lithium futures that are available for trading on exchanges outside of China are cash-settled. This means there is no physical exchange of the underlying product upon expiration. Instead, the financial profit or loss from an expiring position is calculated as the difference between the traded price of the futures and the monthly average of all spot price assessments published in the spot month by Fastmarkets, a leading commodity price reporting agency.

Fastmarkets’ prices are used in physical contracts guaranteeing futures convergence to the spot price at expiry.

Today, cash-settled lithium derivatives encompass a suite of lithium futures and options listed on three major global exchanges. Lithium hydroxide futures are listed on the CME, the London Metal Exchange (LME) and on the Singapore Exchange (SGX); lithium carbonate futures are traded on the CME and SGX; and additionally, lithium hydroxide options are listed on the CME.

Lithium hydroxide was first to launch on the CME on Monday, May 3, 2021, followed by LME on Monday, July 19, 2021, and SGX on Monday, September 26, 2022. A short history of the lithium futures market

The launch of lithium futures came at a time when volatility in the spot market was picking up. The spot market popped from prices in the $10’s/kg to $85/kg in just about 18 months after the launch and dropped back down to mid-$10’s over the next 12 months.

Initially, this may have been a reason to cautiously enter the market, but it was also a trigger that futures must be used to manage price volatility. Beginning in mid-2023 we started to see a gradual increase in traded volumes and open interest both of which peaked in June 2024.

Together with the growing open interest, the US Commodity Futures Trading Commission’s (CFTC’s) Commitment of Traders report show that the number of traders with positions above the reportable level have also been gradually increasing over the past four quarters and currently that number stands at 45 traders.

It is worth noting that another cash-settled CME futures contract, the steel (hot-rolled coil) HRC contract, did not attract as much diversification in the first four consecutive quarters it consistently appeared in the Commitment of Traders report in 2013-2014.

The total number of traders with positions above the reportable level hovered around the 25-level mark. Lithium futures reached a lower level of concentration over the same time horizon. We can view this as a sign of increasing adoption and a market that is taking a positive trajectory in terms of its utility to the industry. Iron ore 2.0?

We often compare the evolution of the lithium market to that of the iron ore market in the early 2010’s. This is largely because the iron ore market made a shift towards spot-based, index-linked pricing mechanisms similarly to what we are seeing in the lithium supply chain today.

Another similarity was the emergence of a futures market in 2010 on the Singapore Exchange, creating a reinforcement loop between the physical and financial market supporting the growth of the spot market together with trusted risk management tools. Iron ore futures are also cash-settled, yet another parallel with the lithium market.

Simultaneously to the emergence of a futures market in Singapore, the Dalian Commodity Exchange launched a domestic Chinese future. The booming Chinese futures market created a spillover effect and instead of competing for volumes it supported liquidity on the SGX.

Yet again, another parallel can be drawn. A physically delivered lithium carbonate futures was launched by the Guangzhou Futures Exchange and almost overnight volumes exploded, contributing to an increase in liquidity on the CME Group’s COMEX exchange.

One of the challenges and comments that are often raised is the limited liquidity in lithium markets. Indeed, a liquid futures market is critical to support the forecasted demand growth. Banks need to be able to price risk to finance projects, consumers need to lock in commodity prices to price their end products securing profit margins, producers need to manage volatility to attract financing at the right cost of capital.

However, deep liquidity in futures markets is not something that is switched on and off like a light switch. It requires time, effort and an entire ecosystem to work together to grow these markets. Both on the physical and financial side. This means, exchanges, banks, brokers, producers, consumers, traders and the price reporting agency need to work in an almost concerted effort to build up liquidity.

To assess the current state of the market and gain insights into what may lay ahead, we can compare the lithium market to existing contracts that have common characteristics. Unlike the base metals derivatives, which are physically-settled, and have been trading for decades in many cases, the steelmaking supply chain derivatives launched more recently and the contracts are cash-settled. Therefore, I believe they are a better comparison.

Comparing the liquidity to that of today’s base metals markets such as aluminium and copper, or iron ore market will uncover lower liquidity compared to the more mature markets. But is it right to compare markets that have existed for over 14 years and in the case of base metals, more than 40 years, to a market that is only in its fourth year? I argue that we will gain more insights when making comparisons at the same point of maturity.

When assessing the derivatives market size and maturity, a measure that can be useful is the ratio between the derivatives volumes and physical market size. Even though the lithium futures market is only in its third full year of trading, we can estimate that this ratio will reach 0.13x the physical market, excluding Chinese domestic consumption, as we are comparing the seaborne market which the Fastmarkets assessment is reflective of.

Taking iron ore futures at the same point of maturity may reveal some clues as to how lithium futures are performing and what the possible trajectory may look like in the next few years.

That ratio was on similar levels as can be seen on the chart, and arguably lithium is taking a steeper path. Provided lithium futures continue to track with a similar dynamic as iron ore did in its first five years, we could see derivatives volumes reach 0.33x and 0.71x the physical market in 2025 and 2026 respectively.

Zooming out, today iron ore futures are trading at 3.5x the physical market and if this is any indication of the potential for lithium, we are just at the very beginning of this exciting market evolving to a mature futures market. The forward curve

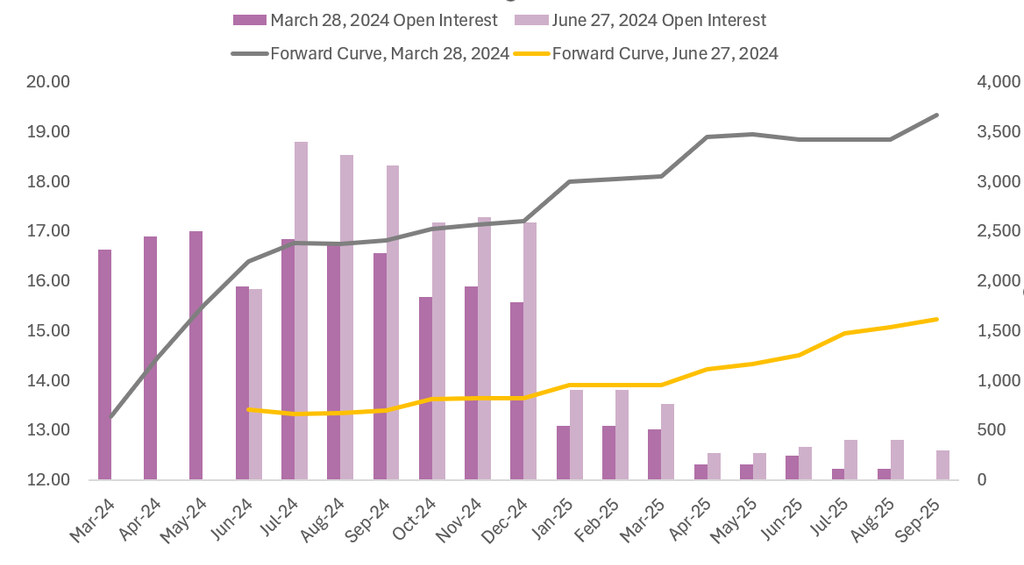

Trust in the futures market is often associated with the forward curve. Mature markets have forward curves that are, by and large, accepted as the market value of future expirations at current market conditions. At times the forward curve can take on a shape that market participants will not view as efficient.

This was the case with lithium, especially in Q1 2024. At the end of March 2024, there was a very steep contango in the market and consumers were finding it hard to justify buying forward at close to 40% premium over spot month for the March 2025 expiry.

As the market continued to grow and mature in Q2 2024 the steep contango flattened and currently we are seeing a much flatter curve. Open interest in the deferred months has also increased, which can be an indication that the shape of the curve is viewed as providing opportunities for consumers to hedge. This is another positive sign as the market continues to develop.

Forward curve. Source: CME Group What comes next?

The lithium derivatives market has all the necessary ingredients to continue its path to becoming a mature, liquid market. Demand growth, financing needs, bank participation, financial counterparties, broker engagement, consumer hedging are all necessary for the market to expand. What is needed is greater producer participation. More recently there are signs that producers are beginning to embrace the futures markets with leaders like Ganfeng Lithium indicating that they will be setting up a hedging desk. Naturally, this is another positive sign of a maturing market.

These are early days, and there are still many unanswered questions. Are all the tools available? Will new contracts emerge? Will the market structure resemble that of base metals with a single point of liquidity, like LME aluminium or copper, or will it be closer to the markets where pricing for different products in the value chain have independent futures markets, like the steelmaking chain, or energy and some agricultural markets?

While there is a case to be made for both paths, the recent drive from spodumeneproducers, the raw material used to produce lithium chemicals, to price spodumene independently of lithium is picking up pace. Many producers, especially in Western Australia, are openly vocal about the need for a more liquid and transparent spot pricing mechanism.

This trend lends itself to the establishment of spodumene futures. I believe it is a matter of time before we see these launch on commodity exchanges attracting new participants that will be able to minimize basis risk and use tools that are more aligned with the physical products they trade.

Lithium markets are without a doubt very young markets and it is easy to say that they are illiquid compared to base metals markets or other commodity markets. However, by analyzing how far this market has gone in its short existence we can see that the growth trajectory is taking a steeper path than markets like iron ore did in the same point of their maturity. This is reassuring for the prospects of one of the most exciting commodity futures launched in recent years.

PLS Price at posting:

$3.07 Sentiment: Buy Disclosure: Held

(20min delay)

(20min delay)