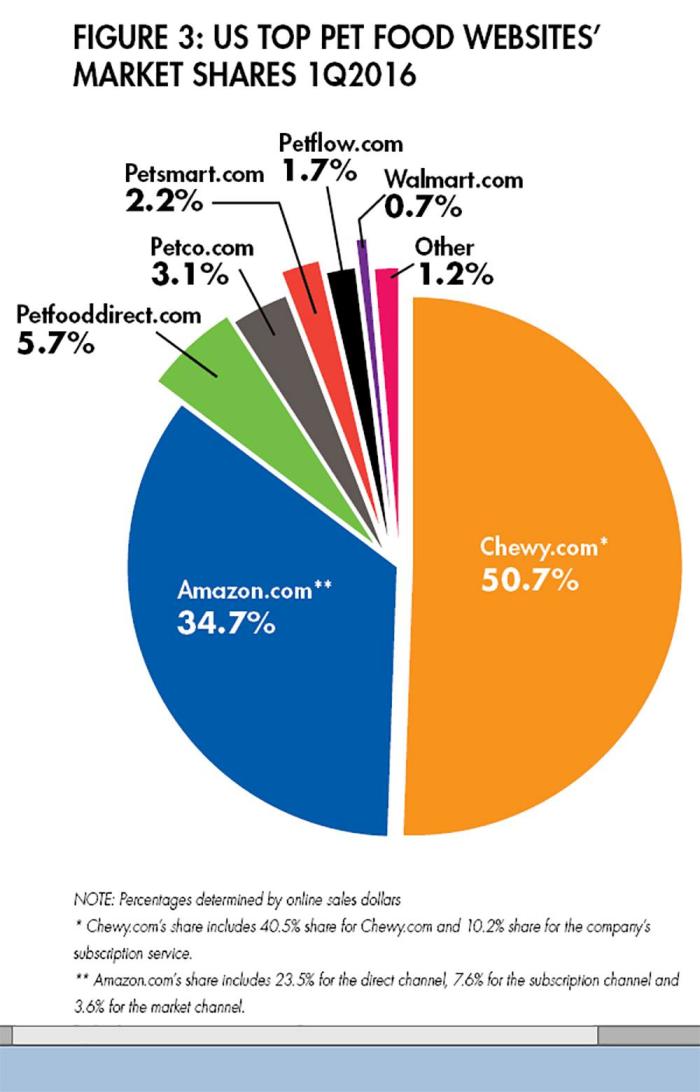

According to this graph, in 2016, Amazon and Chewy have ~85% of total sales in the online pet food sector.

I'm not sure about offline but I am quite confident that majority of pet food sales offline is generated in grocery stores like Walmart where people buy their groceries WITH their pet food instead of going to a pet store to specifically stock up on pet food.

On pet food brands,

In 2017, Leaps and Bounds generated $6m in sales. Less than 1% of market share.

What we need to look at is this sector is dominated by two companies, Mars and Nestle. They control 50% of the market in Australia.

Can GXL compete with these two brands?

Can a retail pet company take market share from two global food companies?

Next is retail and eCommerce in general.

I work in this industry and I know how retail margins are getting squeezed and it is going to get worse with Amazon. Hence, I'm not as optimistic as you if GXL continues to put their growth focus in this area.

Here's what management has to say about Amazon and building a competitive advantage in their latest 2017 annual report,

"Despite increased competition, I believe that our Company is extremely well placed to consolidate and grow its market share, which is currently still less than 10%. A lot has been made recently of the potential impact of Amazon on the Australian retail landscape. In response to this discussion, I think it is worth pointing out that our business has many unique features which differentiate us from our online and bricks and mortar competitors. Our Group is the largest employer of vets in Australasia, with over 650 vets. In a world where pet consumers are increasingly seeking professional advice on medical and nutritional issues for their pets, our unparalleled veterinary expertise is a valuable asset which sets us apart from others."

What I took away from this is management is using vets as their main differentiating factor which I totally agree 100%.

However, I would like management to put more focus on vets and building a competitive advantage there instead of retail. Heska comes to mind. FYI, Heska provides veterinary point-of-care diagnostic instrumentation, laboratory services, blood analyzers, heartworm testing, allergy assessment, intranasal vaccines, IV pumps, and renal health screening.

With Amazon on retail and eCommerce side,

With Mars and Nestle on the pet food brand side,

With Coles and Woolies on the pet food distribution side,

I'm a hold.