I've written extensively on Genworth and been wrong every time. Here I discuss some reasons why I was wrong.

I also update readers on recent developments at Genworth over the last 6 months and update my views on the stock.

On balance, I think expected return for Genworth is substantially positive, but there is a lot of risk.

It's not something I'd buy now if this were my initial decision, so I'm selling half my stake.

To date, I've written three articles on Genworth Financial (NYSE:GNW). The first was a bullish article on December 9, 2013 when the stock was at $15. Next, I wrote a neutral article on August 15, 2014 when the stock was at $13. And most recently, I wrote a very bullish article this past May when the stock was at $9. Needless to say, my track record with this stock has been horrendous. I'd owned GNW on and off prior to my most recent article, but come away with gains somehow. But at the time of my last article, I took a 10% position which I still hold and am substantially in the red on. I'm writing now because I think there is a lot of value in being transparent on mistakes and because writing helps me think more objectively. I've taken this approach since watching Aswath Damodaran's powerful post-mortem on Vale (NYSE:VALE) a few months ago. Here I will attempt to:

Update readers on developments at Genworth since my last article

Update my thoughts on Genworth

Discuss how I could have avoided this mistake

Developments

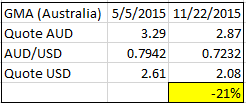

Since my last article, Genworth stock is down 40%. Genworth has reported 2 quarters of results since then without too much in the way of positive or negative business developments, at least relative to the prior LTC reserve increase. The stock of Genworth Mortgage Insurance Australia (OTC:GWRHF) ("GMA"), traded on the ASX, has declined 13% in AUD, but exchange rates have further decreased the USD value to GNW:

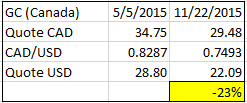

Genworth Canada (OTC:GMICF) ("GC") is traded on the TSX and is down a similar amount in USD terms:

This is quite significant as most of the value of GNW is in these two stakes. The decline resulted in a ~$500mm decline in the value of GNW's combined stake or 20% of the company's current market cap. According to GNW's management team, GMA and GC both have had exceptionally strong loss ratios this year, but have increased recently toward a more normalized level and toward management's expectation for the full year. Genworth Canada is being pressured by the decline in energy prices as energy is a very significant piece of the Canadian economy and the ripples impact home prices in Canada. GNW management thinks Canada will continue to be pressured in 2016, but maintains that both GMA and GC are quality businesses that are undervalued.

GNW's CFO Marty Klein resigned in October to accept a position at Athene Holding, a private life insurer focused on annuities and reinsurance founded in 2008 and sponsored by a subsidiary of Apollo Global Management (NYSE:APO). Athene appears to be growing quickly. It had $19.2B of GAAP assets at the end of 2012 and now advertises $59B of statutory assets (different accounting, but still highlights growth). The transition at Genworth appears to have been orderly as one of Klein's deputies and former Controller / Accounting Officer, Kelly Groh, was named his replacement in the same announcement and Klein stayed on until the company reported its Q3 results October 30th.

Management has been buying back bonds in the public markets that trade at a substantial discount. A few of the maturities are trading close to 10% YTM. They bought back $50mm in Q3 and said they may continue to go this route as part of their plan to reduce parent company debt by $1-2B over the next few years.

Finally and probably most importantly, with the Q3 results management said that LTC is performing in line with the 2014 ALR expectations and the all-important premium increases are also being executed in line with the assumptions announced in February.

Thoughts

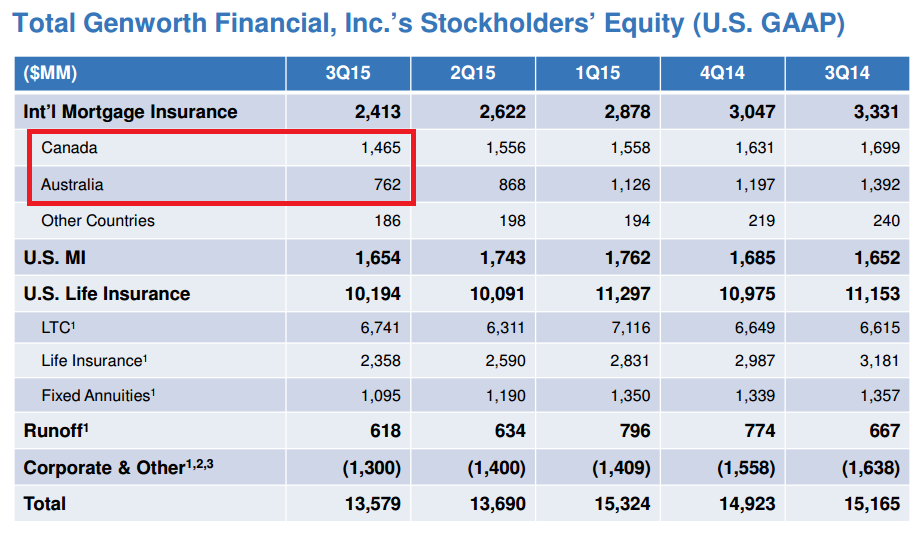

There is a large disparity between the quality of the two international mortgage insurance businesses (GC and GMA) and all of the US businesses. Genworth is truly a holding company with diverse holdings and holding companies are best valued by using the sum-of-the-parts ("SOTP") methodology. That methodology also has the major advantage of GMA and GC being publicly traded and Genworth providing extensive disclosure which allows for a clean SOTP valuation. Genworth owns 57.3% of GC and 52% of GMA. At current quotes and exchange rates, the combined stake is worth $1.867B USD. Pulling out the equity GNW has in each leaves $11.352B of equity.

(click to enlarge)

Source: Q3 Investor Presentation

This includes AOCI and intangibles, however intangibles are now negligible post-impairment and AOCI is mostly composed of unrealized gains on the investment portfolio. I'd rather the investment portfolio marked-to-market, so I'd prefer to leave the remaining equity unadjusted. Further, the value I will assign to the remaining equity in the form of a P/B multiple hinges on ROE, where the full equity is the denominator, so the decision to leave in AOCI and intangibles or not is actually not that consequential.

First, it's helpful to know what ROE Genworth ex. Canada and Australia ("GNW ex.") is earning. The run-rate for 2015 is $192mm NOI, which works out to an ROE of just 1.69%. The other thing worth knowing is what value and in turn, P/B is being assigned to the remaining equity if you take out Canada and Australia at their market values, which trade at much higher P/B multiples than Genworth consolidated. At $5.06 per GNW share, and assuming 510mm diluted shares outstanding including some but not all equivalents that aren't included on the recent quarterly income statements because of antidilution, the market is assigning just $714mm to the remaining $11.4B of equity, or valuing it at a P/B multiple of 0.063x (6.3%). At that low a multiple, it's essentially saying the rest of Genworth is worthless.

Before I go any further, I want to echo what has been said by many analysts and in many SA articles - Genworth needs to separate its stakes in GMA and GC from the US businesses as soon and as cleanly as possible, so that the market recognizes this value. Management seems very reluctant to touch Canada but has talked about further reducing its stake in Australia. On the Q3 call, they said they thought Australia was undervalued and didn't want to sell shares until that changed. Since the call, GMA stock is up 8%. If it keeps increasing, GNW could pull the trigger and that would be a huge catalyst for GNW stock.

But there may be a problem. What happens to the proceeds once the stakes are sold? Do they just get sucked up and destroyed by LTC? Does LTC need more capital? Is it worth less than zero? Based on what value the market is ascribing to it, that is the key question. I think, but am not entirely confident, that it is worth more than zero. I think there are two important things to keep in mind re. LTC.

First, the 2014 LTC review did not look at all of LTC as one unit. Pre-1996 acquired blocks of LTC were split up from the rest. The review determined that there was a negative margin on the pre-1996 acquired block of ~$700mm, and so reserves had to be increased on that block with a new zero margin assumption. That means GNW only expects to break even on this block and it is at risk of further reserve charges if there is even slight adverse developments. However, the review also found that the rest of LTC had a positive margin of $2.3B, meaning that LTC in aggregate is still expected to be profitable and no reserve increase would have been needed if LTC had been analyzed together.

The other important thing to note is probably the most significant assumption underlying the 2014 ALR modeling of LTC. GNW assumed it would be able to achieve an additional $525-625mm of annual premium increases over the next 15 years. They've achieved $380-470mm to date with existing rate actions from 2007 to present, but this is entirely incremental to that. This incremental premium increase assumed has not even been filed or approved by regulators. And some in the insurance industry, like Moody's, think regulators are becoming less open to premium increases. The present value of this assumption is $4.9B of margin. In other words, if GNW didn't assume any further rate increases in their analysis, they'd have to take $2.6B more of reserve increase charges and that's assuming LTC breaks even for the next 15+ years. I do think they'll be able to get further rate increases approved, but how much? The increases from 2007 to present work out to $47mm/yr. The new assumption calls for $38mm/yr over the next 15 years.

Another thing that's really troubling to me is that the CFO who explained all of this to investors no longer works for the company. Why would he give up on the opportunity to see the turnaround through if he thought it'd be successful?

On balance, I think GNW will be able to get further rate increases and that LTC is worth more than zero. I do still think GNW is cheap.

But there are so many moving parts. What if the dollar continues to strengthen and/or the stocks of GMA and GC decline? What if regulators don't approve further rate actions? What if trouble develops again in US mortgage insurance. And again, probably most importantly, what if LTC is worth substantially less than zero and all the capital outside that business gets thrown on the fire and destroyed with it? By no means am I trying to imply in the table above that downside is limited to $3.66.

Mistake

And I think I am very non-objective here. I've been wrong on the stock too many times and lost too much money on paper owning it. There's a great deal of emotional stimuli and it's hard to shut that all out and be rational.

In short, I'm very conflicted and desperately want to sell this and rid myself of the cognitive dissonance. However, I'm not sure if I should given current expected return, which I think is substantially positive.

Going back to my decision in May, I think there were a few things that caused the mistake. For one, I was significantly affected by GNW's price movement. The stock was climbing in the week post-earnings and subconsciously I didn't want to miss the boat. So I rushed my analysis. I rediscovered the stock, did all my research, wrote the article, and bought the shares within 2-3 days. I've noticed this is a common aspect of many of my poor decisions. They are rushed. There's a reason great investors like Buffett move very slowly.

The other thing is that I didn't appreciate the extent to which GNW is outside my circle of competence. Genworth is a complicated web of insurance companies, and although I've followed Genworth in the past, following is not knowing and I don't know insurance. I am not an actuary and can't tell how adequate GNW's reserves now are. An investor on VIC said it best:

"The key question for investors is whether GNW's LTC reserves are now adequate. Regrettably, only time will tell."

We're basically relying on management's word. I think highly of Thomas McInerney, but I don't think an investment thesis predicated on his word is a very good one.

Conclusion

The market is currently ascribing almost zero value to Genworth outside of its stakes in Genworth Canada and Genworth Mortgage Insurance Australia, and there is a feasible path to triple digit returns at Genworth, but there are also a lot of moving parts associated with that upside and a quite a bit of risk too.

As I write this, I'm still uncertain what I think of Genworth. Maybe I don't have a real conclusion.

One thing is for certain though: I was very wrong and that's tough to deal with as an investor when you still need to make tough decisions on the stock you were wrong about. It's very difficult to remain objective here. Hopefully this is helpful for other investors in similar situations with stocks outside their circles of competence.

I suppose the key question is: if I did not own this stock now, would I buy it? For me the answer is a resounding no, but I don't know if that is reason to sell out completely, because not all of my reasons for answering no now are about the facts of the case, and I can't divorce myself from the experience I've had with the stock over the past 6 months.

Given all of this, I think I will sell half my stake and continue to mull the decision and the company's prospects.

Write your reply here

A personalised tool to help users track selected stocks. Delivering real-time notifications on price updates, announcements, and performance stats on each to help make informed investment decisions.

(20min delay)

(20min delay)