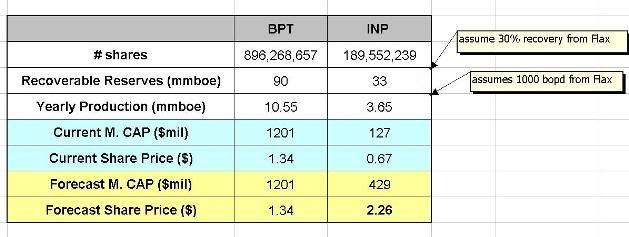

I decided to do a quick peer comparison of INP verses beach petroleum (BPT) to try and establish the expected value for INP once production from Flax is in full swing. Both companies have their major operations in the same area (cooper basin) and I assume that the produced oil quality (GOR, gravity, composition, water cut etc) should be similar for both companies. Both companies also sell oil to the same market and the cost of production will be similar which all together means we have a good 'apple to apple' comparison.

The BPT figures come from their 2007 annual report. I have only assumed the Flax field in this analysis - and that the field is 30% recoverable (110 mmboe total OIP) and will produce at 1000 bopd (from recent INP reports). The two most important things to compare are recoverable reserves and yearly oil production. The market capitalization most heavily weighs on these two factors. You will notice that BPT shares are heavily diluted compared to INP (probably due to many previous capital raisings). INP will not need to issue more shares to raise capital since they have $20-25 million in cash. Notice that the reserves and production of BPT is roughly three times that of INP. If the market treats INP the same as BPT (which it should) the market capitalization of INP should be the M.Cap of BPT / 3. Dividing this forecasted market cap by the number of shares gives us a forecast INP share price of $2.26.

Don’t forget that this price does not include other INP investments! Also, some of BPT reserves are offshore - and are much more expensive to commercialize. To me this is the most exciting buy I have ever made with a comfortable 'low risk' to 'high reward' payoff.

inp valuation vs bpt

-

- There are more pages in this discussion • 15 more messages in this thread...

You’re viewing a single post only. To view the entire thread just sign in or Join Now (FREE)

Featured News

Add ACN (ASX) to my watchlist

Currently unlisted public company.

The Watchlist

HAR

HARANGA RESOURCES LIMITED.

Peter Batten, MD

Peter Batten

MD

Previous Video

Next Video

SPONSORED BY The Market Online