Ok, the AGM presentation pretty much summarises where the company is at right now, but included below are the points I found interesting enough to note down before and during the meeting.

I turned up early, and managed to get a quick chat in before the meeting, with the the CFO Kerry Parker and Lambertus De Graaf.

All business went as planned, every resolution was passed, and it will now take around two weeks before the name change to Panax gets ASICs tick of approval, and the ASX code changes to PAX. Soon after this, expect a roadshow to hit the major cities. I left with a stronger impression that we as shareholders are lucky to have secured someone on Mr Parker's experience and caliber (previously the CFO for AOE, where he helped take the company from a valuation in the tens of millions to the multi-billion dollar company it is today)

Beyond the resolution voting, it looks like the Maharashta deal is not as attractive as initially hoped for. De Graaf specifically mentioned that he is not ready to pursue those tenements, though they remain an option to be considered in the future. As announced today, the Puga and Krishna-Godavari Geothermal Projects are of far more interest anyway, and the Geosyndicate Power Private Limited (GPP) who granted PAX the right lends an enormous amount of expertise and financial backing.

The potential of these projects are massive - absolutely huge. Outside of volcanic regions, I have never heard of such extreme thermal gradients as in the Puga region, with temperatures of over 125C @ 300m (!!!!) and 250C at 1200m. The strategy is very much emulating that which De Graaf displayed with GDY - find the best thermal resource, demonstrate the ability to support massive scale, and allow resource size to attract the necessary infrastructure.

Just because I put so many exclamation marks next to it in my notes, let me say that again:

250C at 1200m, giving the highest confirmed HFR gradient in the world.

Magnetotelluric surveys show the entire geological unit is saturated in an extremely high-pressure brine solution, confirming that this vast project if indeed HFR style. PAX have rights to acquire a 49% interest in the project for $6M expenditure. During his recent trip to the region, De Graaf met with development banks who he said were very interested in helping to develop the resources in the region through financial assistance and georisk/political risk insurance.

With out rambling about Puga further, it is an isolated project with absolutely massive potential, and could feasibly become a regional energy hub is a heat exchanger can be engineered. Priority targets need to be identified using existing data, with the project ready for commercial-scale drilling immediately after. The geological risk is very very low, though full-scale development risk is an obvious detractor until further funding is secured.

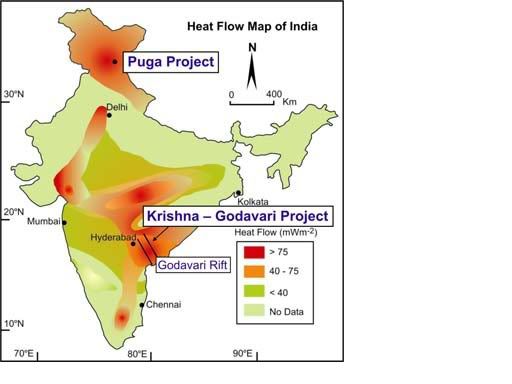

The Krishna-Godavari Geothermal Project (pictured below, hopefully!) is equally as interesting, at an earlier stage, though a more attractive business potential.

As can be seen in the image, the highest known thermal gradients in the region exist within the Krishna-Godavari Basin. PAX has been issued to rights to a 32% operating stake with the expenditure of $6M. Through geochemical analysis, temperatures of up to 215C are expected at depths of 2500m. The region is known to be saturated in brine, qualifying the project for HFR status. The area has the highest heat flow in India, and numerous incentives are in place to encourage development, such as a $100/MW hand-out by the government (!!!!), a 10 year tax holiday, and further carbon credits. The tenements are adjacent to a producing gas field (hence the well-understood geology), and are intersected by good infrastructure.

The Krishna-Godavari has every indication of being one of the most economically attractive geothermal projects in the world. This project on it's own could be a company maker, but of course there is also Kyrgyzstan.

An extra tenement has been added to the Kyrgyz portfolio (due to the nature of the JV with Kentor, PAX receives instant rights to any tenements they acquire), bringing the total tenement count to 5. Infrastructure is adjacent to the project, and is used to export electricity to China nad other several other adjacent countries. Geologically, the region is well understood, with gradients of 100C/km being indicated through years of Soviet drilling. While in the region, De Graff met with the world bank, who had "great interest in seeing the resource developed".

PAX is currently considering the options for further assessment and development of the site, including World Bank Political Risk Insurance. While the capacity of the existing infrastructure is not high, it will support initial development and can be upgraded as the scale is increased (with potential scale dwarfing anything that could ever be possible in Australia). Dr. Graham R. Beardsmore, the leading expert on geothermal heat flow, is currently compiling a report on the scale and nature of the Kyrgyz resource, to be released to the market in the near future (a matter of weeks it seems, would be an excellent little bit of reading to carry around on the roadshows....)

Any one of these projects offers absolutely MASSIVE upside the the current valuation of PAX, yet there is of course the Limestone Coast Geothermal Project.

The LC conventional project is extremely well understood with regards to geology and potential production scale. The resource is vast, covering thousands of square kilometres, with heat distribution equally well understood. Current indicators suggest a huge output of 10MWe per well are readily achievable and with the current understanding of the porosity/permeability of the region, the figure is remarkably reliable. De Graaf speculates that the resource can support hundreds of MW capacity, and the highest heat zone is directly adjacent to the ocean, allowing for geodesal to be a very real (and -acknowledged- ) option for future commercial operations.

Drilling will be matched by Labor on a dollar for dollar basis, up to the value of $5M per well for two wells (total $10M), meaning URO has enough funds for two full-scale commercial wells (cash position is $10.5M as of yesterday).

At the end of the presentation, De Graaf mentioned that a current priority is to secure a bankable geothermal reserve in the region of 50MW-100MW capacity to use as a cash cow to fund continuing commercial development and scaling excercises for the other projects. The reserve is to be low risk and readily developed. Due to being absolutely screwed over by Quantas (cancelled flight, rescheduled to leave about 30 minutes after the meeting finished!), I had to leave just as the meeting concluded. As I literally opened my mouth to ask for more details, one shareholder in the back row felt it was time to ask her question. It went something like this:

"Now, I'm not a technical person, but I feel like the direction of the company is changing a bit. I thought this was a Uranium company but it's starting to look like we are a 'geostring' (yes, she really called it geostring!) company. I feel you are not focusing on uranium anymore"

De Graaf looked as incredulous as I felt, and the entire team spent those precious 5 minutes explaining to this batty shareholder that the resolution was resoundingly passed with a resounding vote of support at the last EGM. What a waste of question time, just so she could go home and explain the situation to all 27 of her cats.....

Nutters aside, the future of this company looks very strong, and very unique. The quality of the projects is, in the literal sense, unparalleled. The scope for the company is huge, and I left the meeting considerably more confident that PAX is set to deliver returns that cannot be readily emulated by the other low-cap GEOs. De Graaf is a company-building powerhouse, and has compiled a portfolio of projects that provide short-term SP upside and long term mega-viability (I had to invent that word to express my sentiment!). The ability to implement a heat exchanger and attract funding is a very real risk for all the international projects (LC is known to be viable), but the shallow nature of all the resources allows for an accelerated exploration and commercialisation plan.

A great company, with the strongest business position of any low-cap GEO company. Upside is as extreme as the thermal gradients, and downside is capped by the known commercial viability of the LC project. Cash position is excellent, and several major JV partners are known to have expressed interest in the Australian project.

URO Price at posting:

0.0¢ Sentiment: Buy Disclosure: Held

A personalised tool to help users track selected stocks. Delivering real-time notifications on price updates, announcements, and performance stats on each to help make informed investment decisions.