Fortescue, An Australia Iron Ore Pure Play, Is Attractive As a Value Stock

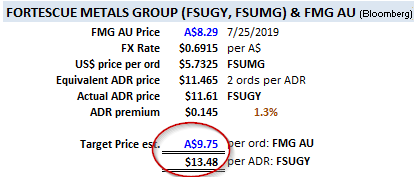

Fortescue Metals Group, (OTCQX:FSUGY) (OTCQX:FSUMF) a US$17.6 billion market cap iron ore stock (listed on the Australian Stock Exchange under the symbol "FMG" and which is listed on Bloomberg as "FMG AU" or "FMG.AU), is deeply undervalued. Based on my analysis, detailed below, the stock is estimated to be worth 18% more than the present price. My price target is A$9.75 per ordinary share or $13.48 per ADR.

Source: Hake estimates

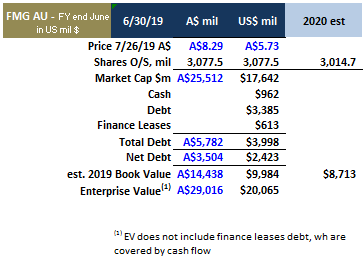

Source: Taken from company documents at www.fmgl.com.au

The stock yields 8.7%, is a pure-play on iron ore and also China's insatiable demand for the commodity, and is now focusing on increasing its dividends and share buybacks. Moreover, the dividend boosts and share buybacks are in the direct personal interest of Andrew Forrest, a West Australian mining entrepreneur who founded the company and controls one-third of the stock.

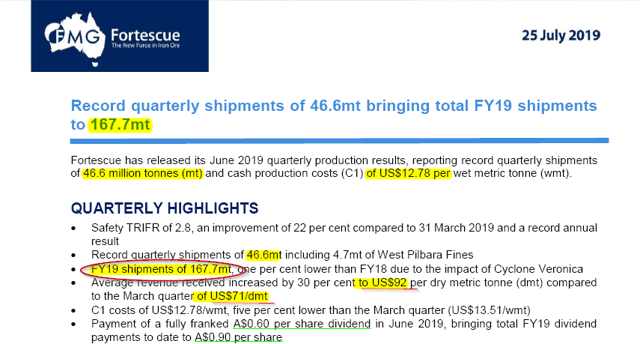

On July 25, 2019, FMG released its fourth-quarter 2019 production report for the quarter ending June 2019. (Note that virtually all Australian stocks have a June fiscal year-end, and usually just report their financial results twice a year, but FMG gives quarterly production updates on its iron ore mining results. Analysts can then project what the second half 2019 results are given those figures.) Here is a synopsis of the key points from that report:

Source: 7-25-19 FMG Quarterly Production Report

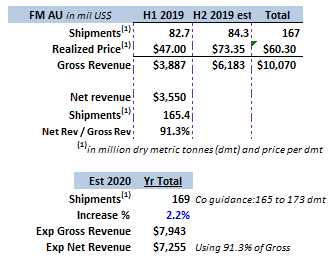

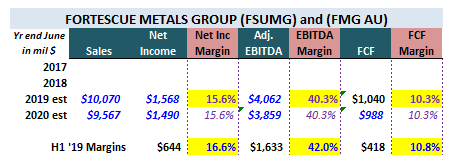

FMG produced and shipped 82.7 metric tonnes ("mt") of iron ore in the first half ending Dec. 31, 2018. The 167.7 mt of FY19 shipments implies that the second half was 84.4 mt. Also, the average price has risen to US$92 per dry metric tonne ("dmt") over the first-half (US$47). My estimate for 2019 and 2020 uses a percent of sales method based on the first half 2019 figures:

Source: Hake estimates

Source: Hake estimates

Based on this I calculated the value metrics of the stock using my estimates for FY 2020 in the various metric categories:

Source: Hake estimates

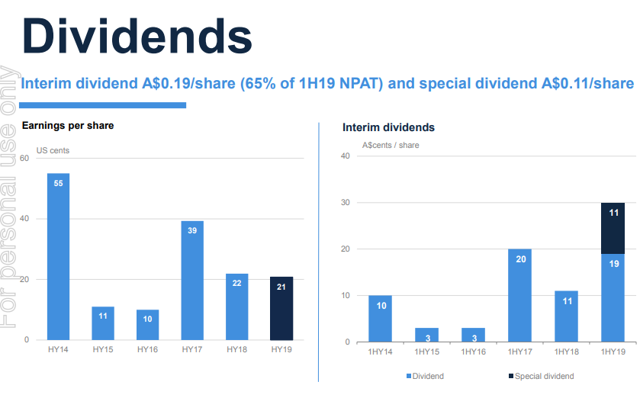

FMG's Dividends. FMG's dividend payments and estimated yield need explanation. FMG recently declared and paid two special dividends. The first, for A$0.19 was added to the first-half regular dividend of A$0.11 per ordinary share ("ord"), for a total payment of A$0.30 per ord. This dividend was paid out in March 2019.

Source: Company presentation, as listed on the ASX website

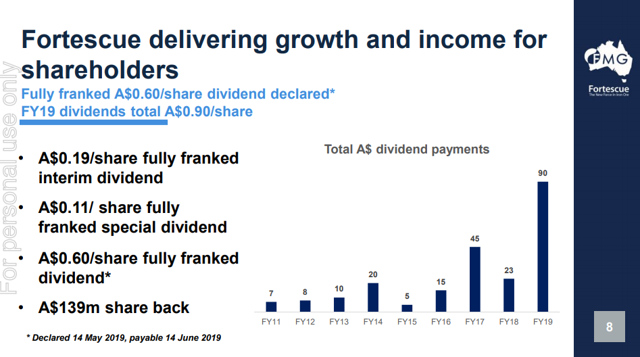

In May 2019, FMG announced a second special dividend for A$0.60 per ord, paid in June 2019. Total payments in FY 2019 (ending June 2019) have been A$.90 per ord ($1.214 per ADR from Citibank, the depository bank):

Source: FMG presentation on 5-14-19

Let's look at this more closely. My estimates (see above) show that for FY 2019 FMG will produce earnings of US$1,548 million. Since there are 3,220 million fully diluted shares outstanding, that implies that the full-year EPS will be US$0.49, or AS$0.68 to A$.70 per ord. Compare that the A$0.90 per ord in dividends for FY 2019. FMG has paid out A$0.20 more than it is expected to have earned on a net income basis at a payout ratio of 127.8% (A$0.90/A$0.70).

Keep in mind that the dividends are not paid on fully diluted shares, and also factor in buybacks by the company. So the real payout ratio is probably lower, at around 122%. For example, non-diluted shares outstanding is probably less than 3,077.5 million outstanding at the end of Dec. 31, 2018, given the company's buyback program. That means that the EPS on a non-diluted basis is probably closer to US$0.51 or A$0.74 per ord. Therefore the payout ratio for FY 2019 is closer to 122% (A$0.90/A$0.74).

Buyback and Dividend Policy Going Forward. These payouts and the buybacks completed in H1 2019 show that FMG has shifted its capital return policy to a more shareholder-friendly stance. Here is what the company said in its recent H1 2019 report (ending Dec. 2018):

Source: Half-year results of FMG to Dec. 31, 2018, as reported on ASX website

Source: Same as above

On May 14, 2019, FMG made a separate press release explaining the rationale for the A$0.60 per ord special dividend:

Source: May 14, 2019, FMG Dividend Distribution Announcement.

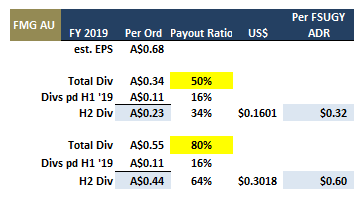

The last paragraph suggests that there will be another dividend payment in Sept./Oct. 2019 covering the second half of FY 2019. How can it do that without violating its 50-80% payout ratio policy? The answer is the two "special" dividends paid out so far this year are not counted as part of the normal payout by the company. Only A$0.11 of the expected A$0.70 earnings per ord expected for FY 2019 count in this policy, or about a 16% payout ratio. Since FMG is committed to paying out 50-80%, the remaining dividend to be declared in Sept. 2019 and paid out in Oct. 2019 could range from A$0.23 to A$0.44 per ord, or US$0.32 to US$0.60 per ADR (i.e. FSUGY share):

Source: Hake estimates

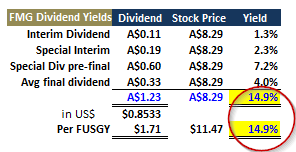

So the upcoming payment in Sept./Oct will have a yield of from 2.0% to 3.7%. Let's assume that earnings will be exactly the same for the next year (even though FMG is projecting higher mining production and shipments). And let's assume the same payments are made as in the past year:

Source: Hake estimates

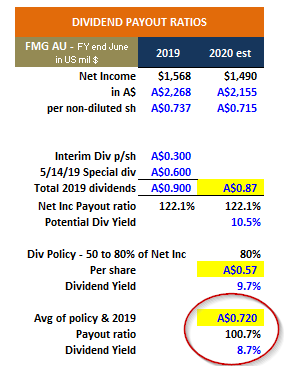

The stock could theoretically yield 15% (and a little less for the ADR due to fees) but this is not a sustainable yield as it can not be financed in the long term by FMG's earnings and would dramatically increase the company's debt ratios in the short run. Therefore, I have conservatively assumed that the FY 2020 payout ratio will be about 100%, including special dividends:

Source: Hake estimates

This shows that the stock can be expected to have an 8.7% - 10.5% yield over the next year. Can FMG afford these dividends and buybacks? What is driving the net income and cash flows of the company?

Fortescue Continues to Experience Strong Demand From China for Iron Ore

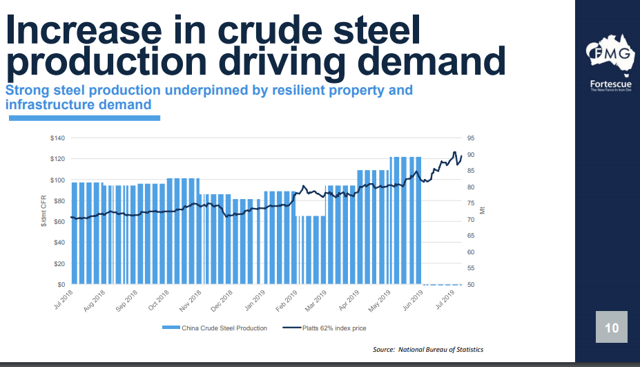

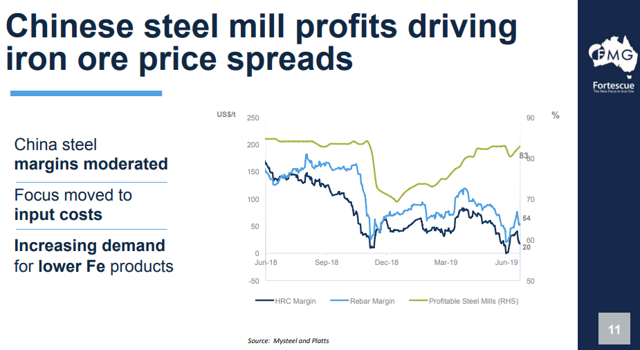

Demand. Chinese steel mill clients represent over 90% of FMG's revenue sources. Despite what some analysts are saying, Chinese steel mills are increasing their steel production and the iron ore price is staying near its highs. Iron ore prices for FMG shipments have been rising. On July 23, 2019, FMG made a presentation describing the underlying fundamentals:

Source: FMG presentation July 23, 2019, to AUSIMM Iron Ore conference

Source: May 14, 2019, FMG presentation to BAML Conference

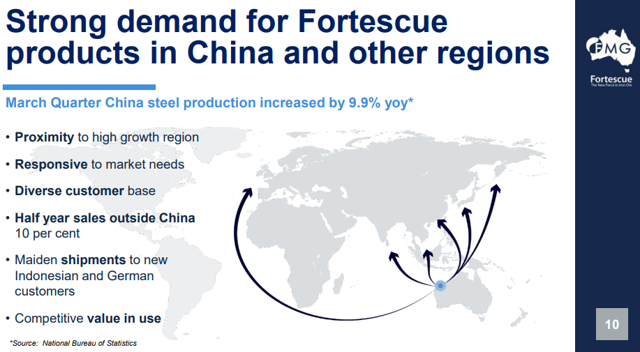

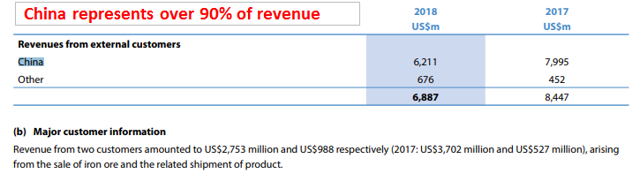

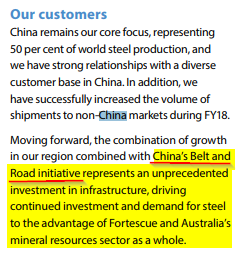

Despite Trump's Chinese steel tariffs, Chinese steel production and iron ore prices have sustained their price gains in the past 2 years. China represents over 50% of the world's steel production. FMG ships over 90% of its product to China:

Source: 2018 FMG Annual Report, page 72.

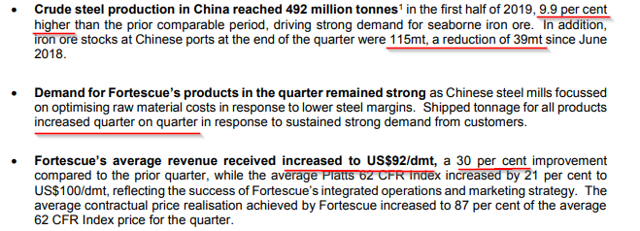

In its July 25, 2019, quarterly report, FMG reported that internal Chinese steel demand is still growing, affecting their demand for FMG's iron ore shipments:

Source: July 25, 2019, June Quarter 2019 Production Report

There is another extraordinary factor affecting Chinese demand for steel, in addition to its internal growth: the China Belt and Road Initiative. This is a massive infrastructure program that China is pushing to over 60 countries. There are estimates that the initiative could involve over $1.4 trillion in massive project investments over the next several decades. FMG is providing the iron ore for the steel projects that China is building in these countries. Here is what FMG said about this in its 2018 annual report:

Source: FMG 2018 Annual Report, page 17.

FMG says it's a major driving force for the demand for steel. It will allow FMG to experience high growth in revenue and cash flow for its iron ore over the next five years.

Supply. There was a major disruption in global iron production from the collapse of the Brazilian company Vale's (VALE) dam at its iron ore site in January 2019, unfortunately killing over 300 people. The problems from this disaster are continuing to reduce supply and hence raise prices.

Andrew Forrest Interview. On March 26, 2019, Andrew Forrest gave an interview with Bloomberg where he discussed FMG's fundamental growth factors from China as well as the iron ore shortage from the Vale disaster. He basically put to rest the notion that Chinese demand for iron ore and the price of the commodity would not stay strong:

https://www.youtube.com/watch?v=FGwihON8aaM

Source: YouTube: Fortescue's Chairman on Vale, Iron Ore Demand, China Slowdown...

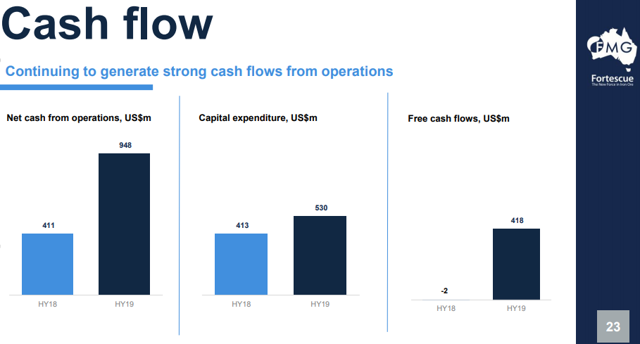

FMG's Cash Flow. FMG is experiencing very high free cash flow. In its half-year to 2019, the free cash flow margin was almost 11% of sales, and 65% of net income converted into free cash flow:

Source: FMG Half-year presentation as of Dec. 31, 2018

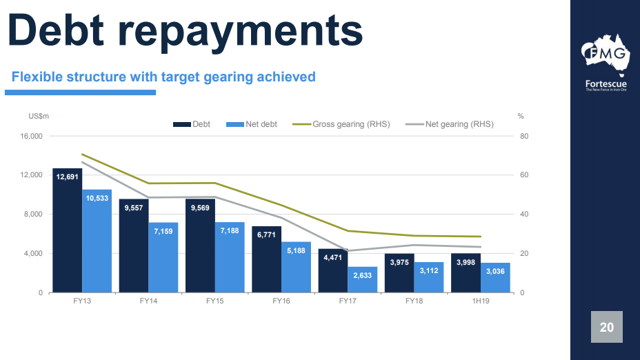

In addition, FMG has paid down its debt has been paid down to the point where its financial leverage is now close to the lowest it has been in the past few years:

Source: Same as above

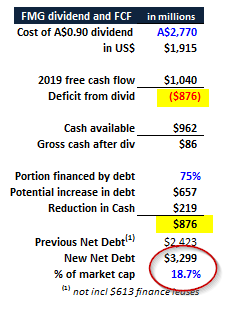

FMG will report its financial results for the year ending June 30, 2019, on August 26, 2019. The two special dividends may have used up most of FMG's free cash flow. I estimate the A$0.90 in dividends cost about US$86 million in a combination of new debt and gross cash reduction:

Source: Hake estimates

This shows that the dividends FMG has paid (and will likely pay in the future) are clearly affordable. Net debt will only be about 18% of the market value of the company, up from 13.7% at the half-year.

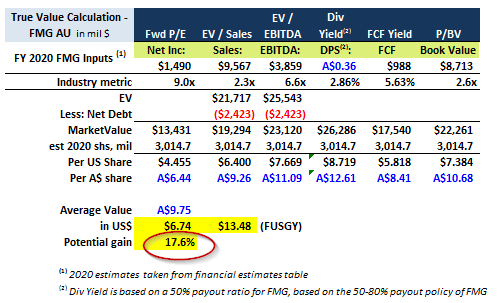

Fortescue is Estimated to be Worth 18% More Than Its Present Price

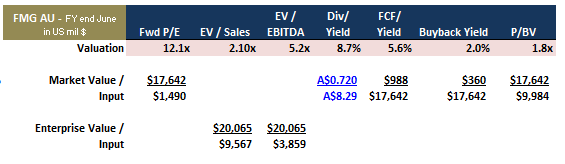

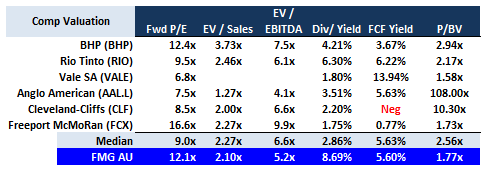

Based on a comparison with its iron ore mining stock peers, FMG is estimated by me to be worth 18% more than its present price on July 25, 2019. Look at this table which compares various value metrics with other comparable stocks:

Source: Hake estimates

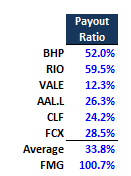

This table shows that FMG is undervalued compared to the median of its peers. As a result, FMG's true value can be calculated using the industry metrics multiplied or divided by the FMG inputs. Note that I lowered the dividend est. for FMG so that the metric is only based on the lowest payout ratio (50%) that FMG said it would use in the future. I did this so that the dividend yield metric would close to the other companies payout ratio, which ranges between 24% to 59% and averages 34% (see first table below):

Source: Hake estimates

This shows that the stock is worth A$9.75 per ord, compared to its present price of A$8.29. This equates to a US$ price of $6.74 per ord, and since there are two ords per FSUGY ADR, the US$ target price per share is $13.48, vs its present price of $11.61 per ADR.

Catalysts

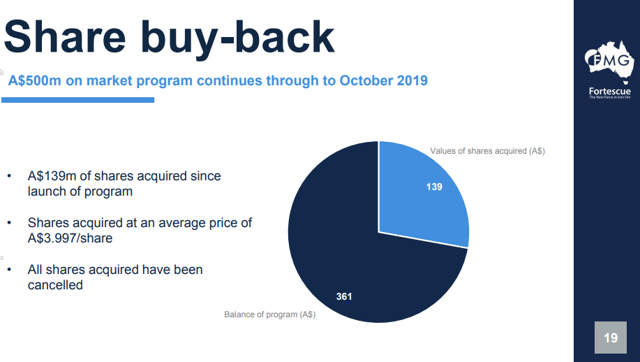

Buybacks. FMG still has over A$361 million of ordinary shares left to acquire as of December 31, 2018, in its $500 million buyback program:

Source: FMG Presentation for Half-year to Dec. 31, 2018

Andrew Forrest ownership. Mr. Forrest was the founder of FMG and still is its Chairman. He owns over a third of the stock. His major income is from dividends paid by the company, as it is unlikely he is going to sell his shares anytime. In addition, the share buybacks serve to increase his ownership in the company:

Source: 2018 Annual Report, page 72.

Conclusion

I recommend the interested investor buy the ordinary shares in their brokerage account rather than the US bulletin board ADR. The commonly used symbol in US brokerage systems for the ordinary shares is FSUMF, instead of FSUGY for the ADR. There is no need to own the ADR and pay the depository institution the ADR fees which are implied in the bid-ask spread for the ADR. The ordinary shares are almost always cheaper in US$ than ADRs given that there is a premium for the ADRs over the equivalent price for the same number of ordinary shares used to make the ADR. Lastly, your account will receive the exact amount of the dividends, rather than the amount the depositary bank uses to calculate the dividend payments.

I have shown that FMG is very cheap, has a high yield of 8.7%, is worth over 18% above its present price, for a potential total return of over 27%. In addition, there are plenty of catalysts that could push the stock to that target price.

Disclosure:I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

(20min delay)

(20min delay)