http://seekingalpha.com/article/377...ay-result-in-better-outcomes-for-shareholders

Sunshine Heart: Ironically, A Cash Crisis May Result In Better Outcomes For Shareholders

Dec. 22, 2015 5:26 PM ET | 3 comments | About: Sunshine Heart, Inc. (SSH), Includes: NVS, STJ

Disclosure: I am/we are long SSH. (More...)

Summary

As a project, Sunshine Heart remains an outstanding financial prospect, with its C-Pulse addressing an unmet need in a large market of 5.2M HF patients.

Slow enrollments may have increased the time to achieve PMA, but capital requirements to get there remain very modest compared to potential end value.

The problem facing existing shareholders is circumstances have pushed the market cap, and thus share price, down to a fraction of project worth.

At current share prices, existing shareholders face massive dilution in any public offering of equities.

“Poison Pill” provisions have excluded possibility of unwanted takeover bids. It is arguable, a sale of the enterprise now may yield better outcomes than continuing to go it alone.

Sunshine Heart (NASDAQ:SSH) is in a difficult situation with a need to secure additional funding in the near future, possibly as early as Q1 2016, in order to continue operations. On 30 November, Mr. John Erb was appointed Interim CEO and President and retains his position as Chairman of Sunshine Heart.

The scenario I see unfolding is one where, at short notice, the company needed to change focus. It needed a CEO with strong capabilities working both "in" and "on" the company as per my article, "CEO Dave Rosa Departs Sunshine Heart: New Skill Sets Are Required At This Stage". Not an easy task to attract a highly qualified candidate, at short notice, with the company facing an impending cash crisis, and a need to get up to speed in an impossibly short time frame. Fortunately, Sunshine Heart already had an experienced Chairman with the attributes required (see here), already up to speed, and as the saying goes, he would be able to just "plug in" and be fully operational from day one.

The focus of taking the company all the way to commercialization of its C-Pulse System might not necessarily have been altogether abandoned, and could be continued if the present funding issue were to be resolved by negotiating an upfront payment under some form of partnership or licensing deal.

But I would think the primary and likely sole focus will be negotiating a sale of the company to any one of what I would expect would be very many interested parties. Before going into detail, in regard to potential partners/licensees and potential acquirers, it is firstly useful to give some background to how the company finds itself in a cash crisis, and where it is in its development stage. I will do this under the following headings:

Background to development of the current cash crisis

- Background to development of the current cash crisis

- Mr. Erb certainly has something to sell, as there is something special about C-Pulse

- Quantifying the cash situation

- The C-Pulse Fully Implantable Model (FIM) will become about as common as an ICD Pacemaker

- The value of the opportunity to be exploited and how best exploited

- The Massive Upside Potential

- "Go it alone" case valuation for the project

- "Bidding War" case valuation for the project

- An acceptable outcome for the project/company entity does not necessarily equate to the best outcome for shareholders

It all started with slow enrollments causing a long and sustained run of falling share prices throughout 2014 ($10.10 at beginning and $4.24 at end of 2014). In support of that contention, here is what PropThink, which has shown belief in the C-Pulse technology, had to say about Sunshine Heart's shares on its website:

we believe the stock is dead in the water; there's little reason to own SSH until management can prove that a plan for improving enrollment is actually working. Sunshine Heart is in the penalty box, and we'd prefer to miss out on some upside in order to confirm that enrollment is speeding up before recommending investors again buy the stock.

I have to agree that was very sound and valuable advice from PropThink. I am sure it was not alone in this thinking, and many sell-side analysts and individual investors have been adopting a similar approach. And with Sunshine Heart seeking independence from large interests, supported by "poison pill" arrangements, its source of capital from its limited investor base has virtually dried up. Beyond 2014, Sunshine Heart had a rough start to 2015, with its Pivotal trial halted as a result of 4 deaths in the treatment arm, subsequently adjudicated as non-device related. The result of the halt has been devastating, with negotiation of protocol changes triggering all 23 activated centers at the time having to again go through the IRB process. These delays resulted in only 15 enrollments in the first nine months of 2015, against an expectation of quarterly enrollments accelerating above the record 14 for Q4, 2014. Activated trial sites now number 27, with a further 13 undergoing the activation process, enrollments look set to pick up, and the first in human implant of the fully implantable C-Pulse model is scheduled to take place in the EU in second half of 2016. Animal trials for the applicability of C-Pulse to treating Pulmonary Arterial Hypertension have been commenced, adding another potential therapy along with angina and the primary focus heart failure (HF) (see here). But the advice to hold off until enrollments are seen to actually pick up is as current now as in 2014, thus cutting off the major source of Sunshine Heart's capital needs.

Even if enrollments are seen to pick up, the poor cash position is enough to continue to depress the share price. Attempts to raise just $20M in a public equity issue right now could further depress the share price and require a doubling of the number of issued shares. The market might not even be able to absorb that many new shares at any price. I understand the difficulties experienced with enrollments, for reasons explained in my article referenced above. Clearly, increased time (duration) to realization of investment adversely affects project returns, but in this case, I believe it must be seen as an unavoidable cost of achieving truly superlative returns, despite the time factor.

Mr. Erb certainly has something to sell, as there is something special about C-Pulse

The C-Pulse was designed to provide counter-pulsation therapy in a similar manner to the intra-aortic balloon pump (IABP), but outside the bloodstream. This was to avoid the dangerous blood clots, stroke and bleeding that plague devices in the bloodstream, such as the IABP and the LVADs from St Jude's (NYSE:STJ) HeartMate II and III and HeartWare's (NASDAQ:HTWR) HVAD and MVAD. Medical researcher interest in the C-Pulse is growing due to the surprisingly good functional outcomes for heart failure patients implanted with the device, far greater than might be expected from an IABP. Sunshine Heart's Chief Scientific Officer, Dr. Georgakopoulos, is gathering data on the mode of action of the C-Pulse and the therapeutic benefits it provides that enable such good functional improvements in patients. His video presentation on Hemodynamics to C-Pulse clinical trial investigators in May this year and his presentation to the TCT Conference in October revealed some of what is being learned about how the therapy is so effective. The IABP is necessarily placed inside the descending aorta distal to the sub-clavian artery and proximal to the renal arteries to avoid occlusion of these arteries. Being outside the aorta, the C-Pulse does not have these restrictions on placement and is in fact positioned on the ascending aorta proximal to the aortic root. And what continuing research is finding is this unique positioning results in magnification of its therapeutic effects far beyond that available from an IABP. The ability to turn the device on and off during optimization is uniquely allowing real time observation of strong baroreceptor activation (achieves neuromodulation), and measurement of hemodynamic effects of the device, in a manner that is not possible with a drug.

In the Sunshine Heart 3rd quarter conference call, it was disclosed the results from the OPTIONS HF study indicate, in addition to its mechanical action, C-Pulse therapy has this neuromodulation mechanism of action, identified as being critical for myocardial recovery. In light of this, the current OPTIONS HF European post market study is to be modified to include patient recovery and weaning endpoints. The new study is expected to start in early 2016. That should be very exciting news in an area of health care where other available therapies can at best only slow progression of HF.

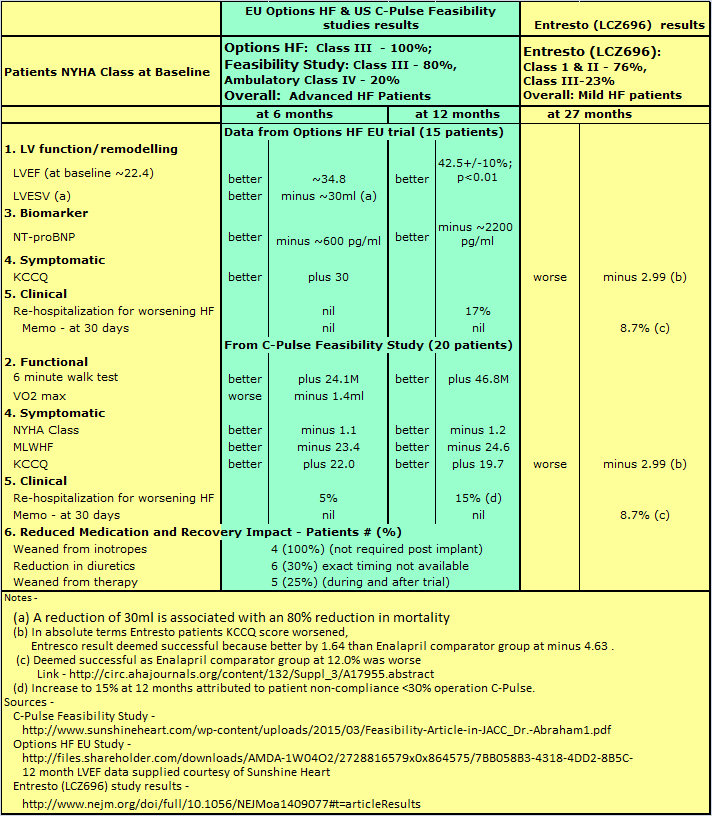

Sunshine Heart is utilizing data from patients in the EU trial to expand and fill out data on C-Pulse efficacy, as shown in Table 1 below. Limited data available from the Novartis Entresto (LCZ696) trial is shown for comparative effectiveness purposes.

TABLE 1

(click to enlarge)

Although the trial numbers for C-Pulse are small, the efficacy is outstanding. The efficacy signals are now being supported by Sunshine Heart's Chief Scientific Officer, Dr. Georgakopoulos, and an increasing number of interested researchers. Being able to turn C-Pulse on and off enables direct confirmation and measurement of changes in hemodynamics. This overcomes to a very great extent the limitations on validity of trial results based on a relatively small number of patients to date.

The term "Paradigm Shift" as used in relation to Novartis' (NYSE:NVS) Entresto is based on the addition of a new drug which, for the first time, potentiates beneficial elements in heart failure rather than inhibiting maladaptive elements. No one is claiming that Entresto will halt the progression of heart failure, just it will slow the worsening compared to Enalapril. The term "Paradigm Shift" as used in relation to Sunshine Heart C-Pulse relates to the ability it has shown to halt and reverse heart failure, with some patients becoming asymptomatic for HF. And that is something special about C-Pulse.

Another something special is the fully implantable model (FIM) due to be implanted in humans for the first time in the EU in 2016. It was always intended that the product to be commercialized would be an FIM, thus eliminating the percutaneous interface lead (PIL). Discussions have been initiated with the FDA regarding expedited access pathway to market. Looking at the results for C-Pulse in Table 1 above, and comparing to MedaMACS data on rehospitalization rates (30 days MedaMACS 24.7%, C-Pulse nil%; 6 months MedaMACS 36%, C-Pulse nil% in EU trial and 15% in Feasibility trial due in part to patient non-compliance), it appears that the Pivotal trial could be found to lack equipoise. One has to wonder at the possibility of equipoise requiring, well ahead of trial interim review point, the trial be granted FDA approval and control arm patients switched to the device arm (see here for the case of FDA accelerated approval of cancer drug bevacizumab due to clearly superior efficacy).

Quantifying the cash situation

As per Table 2 below, at end of Q3, 2015, Sunshine Heart had cash balances of $27.9M and a loan payable of $8M. Amended loan terms require Sunshine Heart to maintain 8 months of cash or equivalents on its balance sheet in place of a requirement to achieve equity funding of $20M by March 31, 2016. The amended requirements are reflected in Table 2 below.

TABLE 2

(click to enlarge)

Possibilities for buying time by pushing an equity capital raising back from Q1 to Q2 2016 -

The capital raising of $7M in Q1 2016, per Table 2 above, might not be required. SVB might still agree, if the EU NUB application is successful and enrollments improve in January and February, to advance a further $7M to bring total loans to $15M ahead of March 31, 2016. If not, Sunshine Heart could prepay the present loan balance of $8M to cancel its obligations under the loan agreement with SVB. Either course of action would still require the $8M capital raise in Q2 2016. If the sale of the enterprise is pursued, having an established relationship with SVB could be beneficial should bridging finance be required during the period of consummation of a sale.

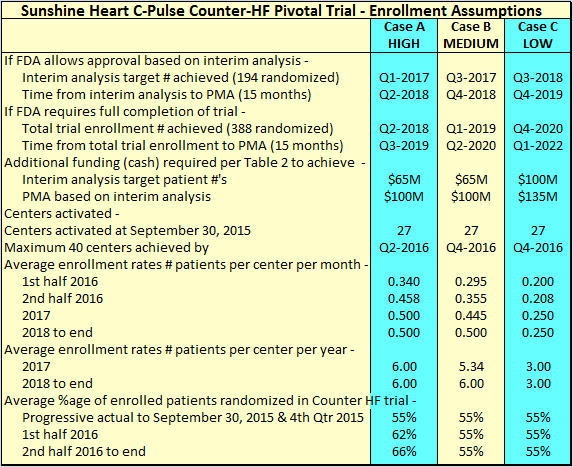

TABLE 3

Sunshine Heart has been targeting average patient enrollment of 1 patient every 2 months, which equates to 0.5 patients per month. The best rate achieved was in the 4th quarter of 2014, when 14 patients were enrolled with 21 centers active, a rate of 0.22 patients per month. That is likely understated taking into account some of the sites were only activated during the quarter. For the LOW Case C, I have assumed a rate of 0.25 patients per month once all 40 proposed sites are activated and fully operational. At this point, I will just register my concern that the low rate of 55% randomization from enrolled patients was only disclosed in the 3rd quarter 2015 conference call. I understand detailed assessment of patients is only done immediately prior to randomization, and for example, a patient might just fall outside the criteria for walk distance by being slightly over or under the upper and lower range in meters. The up and down cycle of HF for patients means these enrollees could qualify for randomization at a later stage. I expect the company to announce randomization alongside enrollments in future. The future percentages of patients randomized compared to the 55% assumed above will be a KPI to watch because increases above the percentages shown above will accelerate trial completion. For MEDIUM Case B, I have assumed balance center activation rate similar to LOW Case C, but with average enrollment rate gradually increasing to 0.5 patients per month. For HIGH Case A, I have assumed all 40 centers are activated by 2nd Qtr 2016, average enrollment rate of 0.5 patients per month, and higher randomization rates of 62% by 2nd quarter 2016 and 66% by 2nd half 2016.

The C-Pulse Fully Implantable Model (FIM) will become about as common as an ICD Pacemaker

In support of the heading -

In the 1960s, industry forecasts predicted all-time worldwide sales of some 10,000 pacemakers but by the 1990s an estimated 350,000 pacemakers were being implanted worldwide each year.

And from this 2002 article in Circulation -

There are about 3 million people worldwide with pacemakers, and each year 600 000 pacemakers are implanted. With rare exception, implantation of a pacemaker does not change the recipient's activities or lifestyle.... Almost all pacemakers are implanted to treat slow heart beating, which is called "bradycardia".

The ICD is designed to shock the heart back into rhythm. Neither the pacemaker nor the ICD actually do anything to improve the health of the heart. Rather, the pacemaker makes the heart beat fast enough and the ICD gives the heart an electrical shock to get it back to work. Contrast this to C-Pulse, which provides the many therapeutic benefits per Table 1 and more, and assists to restore heart health. The C-Pulse FIM is close to the size of an ICD pacemaker and will be implanted in a similar minimally invasive operation. Eliminating the lead through the skin will drive acceptance of the C-Pulse FIM in a way not possible with the current PIL model C-Pulse being used in the Pivotal trial. There is every reason to believe, following FDA approval, the number of Sunshine Heart C-Pulse devices implanted will show rapid growth, as pacemakers have done in the past and continue to do so, and reach the hundreds of thousands per year. The decision for a patient will be akin to accepting the need for a pacemaker and having it implanted in a minimally invasive operation. With the fully implantable C-Pulse II, it will be far less critical a decision than for bypass surgery, which patients readily accept. What also has to be said is, once approved, C-Pulse can be expected to be listed under "Medical Procedures and Surgery" on the National Institute of Health's guidelines for heart failure treatment. I think it is not generally understood how much easier it was for HeartWare's device to gain acceptance in trials due to it being just a smaller and potentially better device than the Thoratec device, which was already encompassed in the NIH guidelines. Once C-pulse is in the guidelines, cardiologists will need to heed the words of Dr. Milton Packer in this video,

We studied that kind of patients, patients that Physicians see every single day. And what Physicians need to understand is, that apparent clinically stable patient is not that stable. And they still have a very meaningful rate of progression, no matter how you record progression: quality of life progression; hospitalization progression; mortality progression. And so it is really important to reduce the risk of worsening over time, even if patients are clinically stable and it looks like they are doing well.

Dr. Packer was, of course, talking in support of Novartis' new drug Entresto (formerly LCZ696) which has proven in its Pivotal trial to slow the progression of HF compared to existing drug therapy, but he makes no claim Entresto will even halt, let alone reverse progression as is being seen with C-Pulse per Table 1 above.

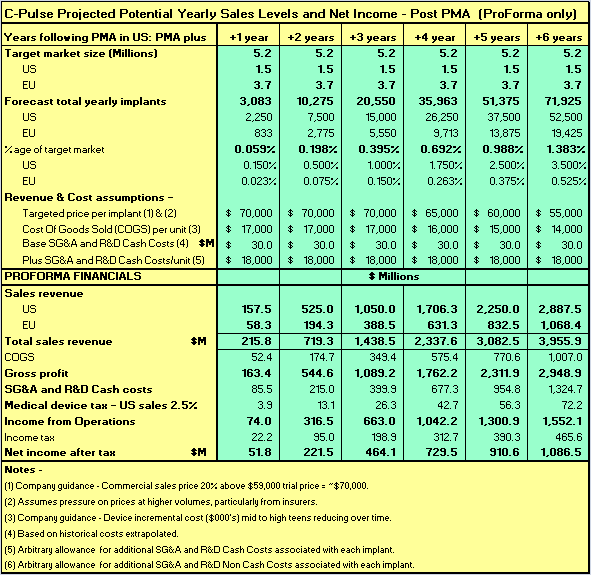

For all of the reasons given above, I believe the projections of C-Pulse FIM implant numbers, 6 years post PMA approval by FDA, as shown in Table 4 below, will in time prove to be quite conservative in the same way as the early Pacemakers forecasts.

The Massive Upside Potential

Sunshine Heart's C-Pulse has a target market of 5.2M HF patients in the US and EU in NYHA Class III and ambulatory Class IV heart failure (see slide 3 of Corporate Presentation).

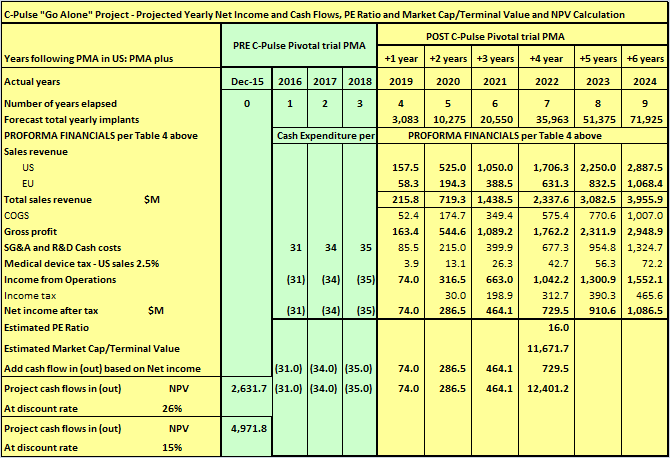

Table 4 below shows estimated growth in yearly implant numbers, revenues, costs and net income for Sunshine Heart C-Pulse FIM in the years immediately following FDA PMA approval. It is necessarily assumed in the projections that Sunshine Heart will have previously gained approval in both the EU and US for its fully implantable model C-pulse.

TABLE 4

The value of the opportunity to be exploited and how best exploited

Sunshine Heart's board and management have in the past given indications they intend to go it alone with C-Pulse. In particular, there is a "poison pill" arrangement in place to prevent unwanted takeovers. It needs to be said that the "poison pill" arrangements are possibly contributing to the current low share price. Shorts and other speculators can go about their business without fear of a serious takeover offer coming out of left field and causing a sudden spike in the share price. Despite the "poison pill" arrangements, there is nothing to prevent approaches to acquire the company on terms satisfactory to Sunshine Heart and without the threat of any form of coercion. I will just give three scenarios of a possible future valuation of Sunshine Heart, one based on going it alone, and the other two based on what a bidding war might do for Sunshine Heart and its C-Pulse.

"Go it alone" case valuation

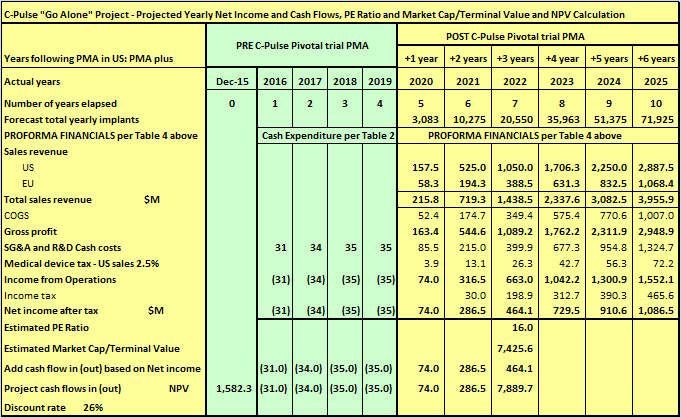

Going it alone is a tough proposition for a small enterprise like Sunshine Heart. So I will assume PMA is achieved in Q4 2019 as per the "Case C LOW" in Table 3 above. In all cases, I will assume PMA based on Interim Analysis because the evidence of efficacy to date strongly supports that assumption.

Table 5

(click to enlarge)

A risk adjusted discount rate of 26% has been adopted to reflect the risks involved for a small operator with a project with long lead times. At a 26% ROR, the initial investment would double every three years. The NPV result of $1.58 billion is not too far away from what the market ascribed to HeartWare over the last couple of years. C-Pulse addresses a far larger market than HTWR, is not in competition with another device, and will not have the need for continuing costly expenditure on R&D in a leap frog race with a competitor.

At the time Boston Scientific (NYSE:BSX) won a bidding war against Johnson & Johnson (NYSE:JNJ) to take over Guidant for ~$27 billion, Guidant's annual revenues were ~$3.7 billion and growing ~20% per year (see further on Guidant below).

"Bidding War" case valuation

Boston Scientific famously, or perhaps infamously, won a bidding war against Johnson & Johnson to take over Guidant for ~$27 billion. That was primarily to gain access to Guidant's defibrillator technology, a technology that in fact does nothing for the health of the failing heart. So, both of these companies are likely to be following closely the progress of Sunshine Heart's C-Pulse, which has shown the potential to actually reverse heart failure.

St Jude, through its acquisition of Thoratec, has observer rights at Sunshine Heart's board meetings. Perhaps this is with a view to being in a knowledgeable position for a future takeover offer which might lead to a bidding war where due diligence would be critical. I see a possibility for Novartis AG to bring a very strong enrollment ability to the negotiating table, through its strong communication ability with cardiologists. And it is cardiologists who are the primary referral source for enrollment of patients for C-Pulse. Novartis is currently in the news with its new drug Entresto that slows the progression of heart failure compared to existing drug regimes. But as mentioned above, Novartis is under no illusions that Entresto might halt the progression of HF. Why would it not want to acquire a simple, fully staffed and operational "bolt on" Medical Device Division that has a therapy to take over where Entresto leaves off? That would also go some way to address concerns of possible side effects from Entresto with long term use, particularly where the patient's condition is worsening.

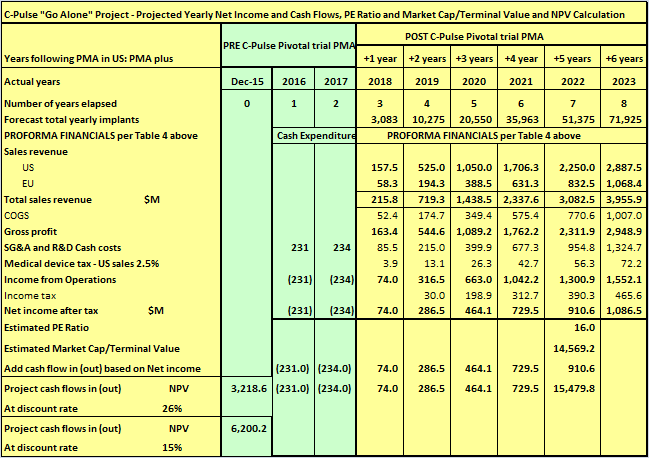

In the hands of Novartis, I believe enrollments could be achieved at the rate for "Case A HIGH" in Table 3 above. But for the sake of conservatism, I will go with "Case B MEDIUM" as reflected in Table 6 below -

Table 6

(click to enlarge)

As can be seen, by just getting the trial completed one year earlier, the NPV, the current valuation of Sunshine Heart C-Pulse project, increases by ~ $1 billion from $1.582 billion to $2.631 billion (discount rate of 26% and time to terminal value of 7 years unchanged). On top of that, in the hands of Novartis, many of the risks associated with the project would be greatly lessened and their internal discount rate for valuing a project such as this might be say 15%. As can be seen in Table 6 above, that would result in the valuation increasing by a further $2.3 billion to $4.971 billion.

And a large company, such as Novartis, with the funds available to throw at enrollments (and fast track the C-Pulse FIM), would go out of its way to achieve PMA by say beginning of 2018. Table 7 below reflects an increase in funding of the C-Pulse project PMA by $200M per year with a view to achieving PMA by beginning of 2018.

Table 7

(click to enlarge)

Once again, bringing forward PMA by one year has significantly increased the current value of the project to a large company with the financial and other resources available to really push things along. To Sunshine Heart, based on Table 5 calculations and assumptions, Sunshine Heart C-Pulse is worth $1.6 billion. Using the same underlying project assumptions, to Novartis or other similar large biotech, Sunshine Heart C-Pulse could be worth in a range from $2.6 to $6 billion.

It should be understood the projections above are primarily to show that value in a project opportunity such as this depends largely on the ability to exploit the opportunity to the greatest degree. In the case of the C-Pulse project, a large biotech is likely to be able to pay the full value that little Sunshine Heart could extract from the project, and still be paying way below the value of the project to the company.

An acceptable outcome for the project/company entity does not necessarily equate to the best outcome for shareholders

In Table 5 above, the projected NPV valuation of Sunshine Heart is calculated at $1.582 billion. But that is on a whole of company basis. By definition, shareholders have a share of the company. For existing shareholders in total, that share is 100% of the existing issued shares of 18.3M shares. But also in Table 5, there are projections of $135M in equity issues in order to complete enrollments and enable the opportunity to be exploited. By the time that equity was issued, the existing shareholders might only own 15% to 20% of the shares in the company. So while the total value of the company might have increased to ~$1.6 billion, at a reduced 15% share, the existing shareholders' shares would only be worth $240M or $13 per share. Note that $13 per share still is ten times the current share price trading around the $1.30 mark.

Conclusions

It is clear from the analyses above that a larger biotech with the resources to more adequately exploit this C-Pulse opportunity could so enhance the potential project returns that existing Sunshine Heart shareholders would be better off with a sale now rather than to go it alone. It will almost certainly require more than one interested bidder to extract full value from a sale now. But I expect there to be many interested parties, whether or not they bid, including Novartis AG, St Jude, Medtronic (NYSE:MDT), Baxter International (NYSE:BAX), Boston Scientific, Johnson & Johnson, Abbott Labs (NYSE:ABT) and Fresenius (NYSE:FMS).

There are some interesting tensions that are likely to come into play here affecting the market price of Sunshine Heart's shares. If the share price stays low, the company is virtually forced to entertain offers for the sale of the company. Even a hint of sale discussions and the share price will likely rise. If the share price rises sufficiently, the ATM facility could be used to relieve the current cash crisis. If the cash situation is relieved, that could result in a further increase in share price. Having faced a crisis, even if solved temporarily, there is likely to have developed a sense in management of the sale of the business being the best way forward. Announcement of a license agreement for the EU with an associated up front payment could trigger further increases in share price.

As detailed above, even if the existing shareholders were diluted down to a 15% share of the company, and under the worst case valuation scenario, the share price calculated of $13 per share is ten times the price at which SSH's shares are currently trading.

I wonder if, at this moment, PropThink is rethinking its advice to its clients (see further above) to hold off on buying Sunshine Heart's shares until enrollments are seen to pick up? Other events than increasing enrollments could now overtake that good advice at the time. Of particular interest to watch will be the ongoing release of data from the EU Options HF trial, expanding the reporting of outstanding data as per Table 1, the results of the EU NUB application due February 1, 2016, and of course, 4th quarter 2015 enrollments and randomization. Announcement of a license agreement for the EU with an associated up front payment to help resolve the cash situation would not surprise either.

Disclaimer: The opinions in this document are for informational and educational purposes only and should not be construed as a recommendation to buy or sell the stock/s mentioned. Past performance of the company/s discussed may not continue and the company/s may not achieve any projected earnings or dividend growth. The information in this document is believed to be accurate, but under no circumstances should a person act upon the information contained within. I do not recommend that anyone act upon any investment information without first consulting an investment advisor as to the suitability of such investments for their specific situation.

Additional disclaimer: This information does not supersede original manufacturer's specifications nor constitute medical advice or advertisement. Trademarks and logos belong to their registered owners. I neither practice medicine nor provide medical services. I am not a licensed physician, so I am not qualified to provide any kind of medical advice.

Editor's Note: This article covers one or more stocks trading at less than $1 per share and/or with less than a $100 million market cap. Please be aware of the risks associated with these stocks.

Ironically, A Cash Crisis May Result In Better Outcomes For Shareholders

Add to My Watchlist

What is My Watchlist?