Stem cell therapies hold the promise to cure chronic diseases that currently cause a heavy economic burden on society but clinical development has been decades in the making.

Nevertheless, recent clinical results from adult stem cell therapies have yielded the first late-stage straightforward successes, proving that the technology can be effective.

When technologies reach maturity and start delivering convincing clinical results, it usually translates into a big uptake in valuation: is this "inflexion point" coming now?

With major sectorial catalysts expected, now might be a good time to get to know the field as we have never been closer to the first potential "stem cell blockbuster".

However, as with every investment opportunity, it takes a careful analysis of the sector to find out where the true potential lies.

Stem cell therapies are a key component of regenerative medicine, a medical field that holds many great promises. Thanks to some pretty dramatic technological advances observed in the last years, we might be right now on the brink of a new therapeutic age in which restoring tissues or organs, or even growing new ones by activating the body's own repair mechanisms will become common practice.

However, in terms of return on investment, let's face it, with a very few exceptions, most early investors in stem cell biotechs have been losing money. Some of the earliest commercial stem cell biotechs were founded in the late 1980s and went public during the next decade, and what was once seen as a very exciting investment opportunity led to many disappointments.

Clinical trials either did not live up to expectations or suffered important delays, burning large amounts of cash with few tangible results - as a striking latest example, stem cell pioneer StemCells, Inc. (NASDAQ:STEM) just announced the winding-down of its operations after more than three decades of research. As a consequence, investors might have decided to abandon the field entirely, losing all hope that stem cell products would actually make it to the market and generate substantial revenues.

As this article will show, while it is true that long-term returns are yet to materialize, one should not overlook the fact that developing a new technology and bringing viable product to the market takes a lot of time - in that, stem cell biotechs are not fundamentally different from any other biotech venture, as detailed in a previous article. Hence, as with many types of technological breakthroughs and especially in the healthcare field,there comes a time when technologies reach maturity and start delivering convincing clinical results, which usually translates into a big uptake in valuation. Is this "inflexion point" coming now? Recent developments show that things are falling into place for the stem cell industry and that we might never have been closer to the first potential stem cell blockbusters. However, as with every investment opportunity, it takes a careful analysis of the sector to find out where the true potential lies. Definition and quick historical perspective

The words "stem cell" are actually a generic term covering a wide range of different cell types, which share the same basic characteristics: stem cells are undifferentiated cells that can give rise to specialized cells and have a strong ability to divide and produce more stem cells - see here for more details.

While there are many different kinds of cells falling under this definition, one main categorization can be made into so-called "adult" stem cells and embryonic stem cells. Embryonic stem cells are "original" stem cells, which constitute the base material of every living being formed inside the womb. Those cells have the ability to differentiate into any kind of specialized cells in the body. While embryonic stem cells may hold the greatest therapeutic potential, someethical issues have been withholding the broad development of therapies based on those cells. Adult stem cells, while being less potent than embryonic stem cells, are much more widely available as they can be collected harmlessly from consenting adult donors - there are many sources, such as bone marrow, blood, fat, dental pulp and so on.

Historically, the first stem cells to be isolated in the 1960s were adult stem cells (see regenerative medicine milestones below). This was achieved by researchers at the University of Toronto, and the first successful bone marrow transplants followed only a few years later - this operation is now routinely performed in some blood cancer treatments. - Figure 1: Historical milestones of regenerative medicine

(Source: G. Bonfiglio, Proteus)

In the early 1980s, the first embryonic stem cells were isolated as well, raising hopes of developing "universal cures" and regrow whole organs. Building upon those academic findings, the first commercial stem cell biotechs were founded in the late 1980s, mostly in the U.S. Meanwhile, academic research continued to progress and lead to a "second wave" of biotech spin-offs which were launched in the 2000s, mostly in Europe, Israel and Australia.

Finally, about ten years ago, the latest major breakthrough in stem cell research was achieved when it was discovered that, under specific conditions, adult cells could be genetically reprogrammed to revert to an embryonic stem cell-like state - those are called induced pluripotent stem cells, or iPSCs. Lessons learned - A matter of time and scientific progress

The "first wave" of stem cell biotechs (founded between 1980 and 2000) comprised mostly U.S. companies that were founded as early as 1980, although some of them actually went public as late as 2007. All of those companies have been going through rough times, and all of them still are small-cap biotechs today. Companies which are still active today include Vericel (NASDAQ:VCEL), Caladrius (NASDAQ:CLBS), Osiris (NASDAQ:OSIR), Neuralstem (NASDAQ:CUR) and Athersys (NASDAQ:ATHX).

Besides, stem cell pioneer StemCells, Inc. just announced the winding-down of its operations, and Ocata (NASDAQ:OCAT) sold itself to Astellas(OTCPK:ALPMF) for $379 million in February 2016. Finally, Geron Corp.(NASDAQ:GERN), one of the earliest pioneers of regenerative medicine and the company responsible for the very first commercial stem cell trial in the U.S. chose to abandon its stem cell assets in 2011 - some of which were subsequently acquired by BioTime (NYSEMKT:BTX), which is now developing several stem cell product-candidates through its subsidiary companiesAsterias (NYSEMKT:AST) and Cell Cure Neurosciences.

The "second wave" of stem cell biotechs (founded between 2000 and 2015) comprises a majority of companies based outside of the U.S. This is a result of the increased transition from non-commercial academic research conducted in hospitals and universities to commercial companies (spin-offs) that occurred mostly in Europe, Australia and Israel during the last decade. Those companies include Mesoblast (NASDAQ:MESO), TiGenix (OTC:TGXSF),Cytori Therapeutics (NASDAQ:CYTX), Pluristem (NASDAQ:PSTI),Brainstorm Cell Therapeutics (NASDAQ:BCLI), Celyad (NASDAQ:CYAD),Capricor (NASDAQ:CAPR) and Bone Therapeutics (OTC:BNZPF). See tables in appendix for a comprehensive review and further details on public stem cell companies.

Typically, developing a new drug takes 10 to 15 years, which means that the earliest stem cell biotechs from the 80s should already have reached commercial stage with their first products. However, in this case, stem cells remained an emerging field for decades as it took a lot of time and research to understand how the cells actually work - dealing with living cells is an incredibly complex matter and the sheer diversity of technical and regulatory issues that had to be overcome was probably not anticipated from the beginning. These hurdles clearly had an impact on the valuation of early biotech pioneers, which turned down many investors, inducing a long lasting desertion of the field that is still felt today. In hindsight, the first stem cell biotechs were probably trying to find out how to use the cells based on very partially understood mechanisms - that led to a lot of misconceived and misconducted trials.

For example, recent research and clinical data show that paracrine signallingmight play a crucial role in most adult stem cell therapies - the complex chemical signals cells are sending to each other might be the key toreactivate endogenous stem cells and/or induce an immunomodulatory effect. As a consequence, it means that long-term engraftment might not be needed in most adult stem cell therapies, which encouraged biotechs to abandon the development of autologous products (based on the patient's own cells) and turn to allogeneic therapies (based on donors' cells) - and this is only one of the elements resulting from the dramatic progression of scientific knowledge in this particular field during the last decade.

However, regardless of specific technological challenges, the rise of biotechs breaking new ground in life sciences is bound to take time and money. There is a clear and successful historical precedent though, with the rise of biologics (large molecules produced within living organisms), which helped propel some early biotech pioneers such as Amgen (NASDAQ:AMGN), Celgene (NASDAQ:CELG) or Biogen (NASDAQ:BIIB) to stratospheric valuations. Although most of those companies actually had relatively higher valuations during their development stage than many stem cell biotechs nowadays, it nevertheless took around one decade to see lasting uptakes in valuations, and another decade to observe egregious profits supporting skyrocketing stock prices. - Why are stem cells special and what do they have to offer?

While it is important to have some historical elements in mind, the essential question remains: Where are we heading now with the development of stem cell therapies and what could justify investing in this field?

The coming of age of adult stem cells - A new treatment paradigm

Treating chronic or acute diseases with chemical drugs (small molecules) is relatively cheap but it has its downsides - dose-limiting toxicity and a relative inability to deal with complex targets. The advent of biologics (large molecules) helped treat serious conditions with relative efficacy but it is expensive and most of those drugs have unwanted systemic side effects, such as impairing the immune system and rendering patients weaker to (other) infections. Besides, most of the time, these treatments actually focus on treating the symptoms, not curing the disease.

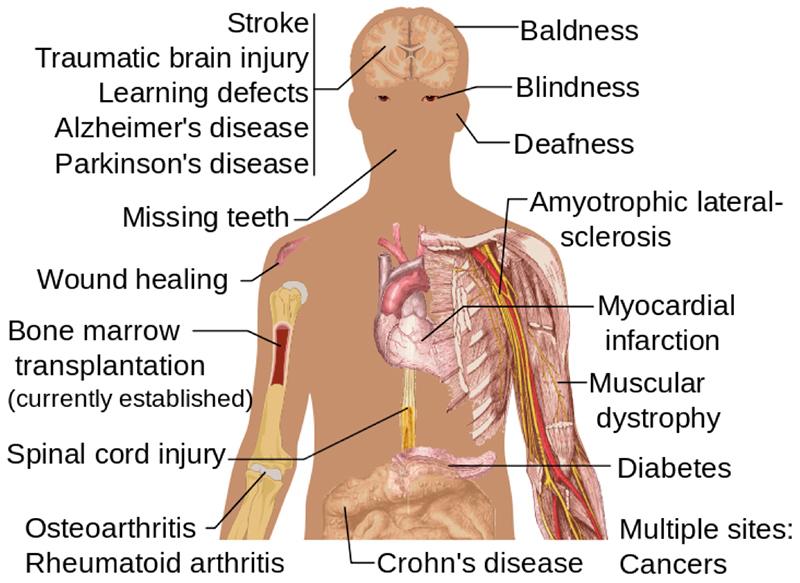

So far, after decades of research, adult stem cells have been proven to be generally safe and well tolerated, with no systemic side effect. Byenhancing the body's own repair mechanisms, stem cell therapies offer the opportunity to treat serious conditions, which have no effective cure today and cause a heavy economic burden on society such as strokes and heart attacks.

Additionally, thanks to their very safe immunomodulatory properties, some adult stem cells are worthy candidates to treat conditions resulting from systemic inflammation (sepsis, ARDS, autoimmune diseases, etc.). Both mechanisms of action offer attractive perspectives in the context of an aging population in industrialized countries, where the incidence of chronic diseases is bound to rise dramatically over the next decades. - Figure 3: Potential uses of stem cell therapies

(Image source:Medical gallery of Mikael Häggström, 2014)

This also introduces a new drug-development paradigm: Thanks to their safety profile, adult stem cell therapies are increasingly likely to be approved through smaller clinical trials (as the FDA is less inclined to require large control groups to account for potential side effects). Enrolling fewer patients means running cheaper clinical trials, and it means that overall development costs for adult stem cell therapies might end up being significantly lower than those of traditional drugs. As evidence of this, several recent developments are confirming the trend:

- Teva (NYSE:TEVA) recently obtained a substantial reduction of the enrollment target of its ongoing Phase 3 heart failure trial (based on Mesoblast's stem cell therapy), from 1,165 to 600 patients, thanks to demonstrated safety and hints of efficacy.

- Celyad's U.S. pivotal Phase 3 heart failure trial is set to enroll only 240 patients.

- TiGenix's U.S. pivotal Phase 3 trial in Crohn's fistulas is set to enroll 224 patients.

Those enrollment targets, considering that none of these indications are considered orphan in the U.S., are extremely low compared to industry standards - for reference, Novartis' (NYSE:NVS) heart failure drug Entresto was approved last year based on an 8,442-patient pivotal study.

Among stem cell therapies, adult stem cells are the most mature products- some have already reached the market and an increasing number of late-stage clinical results are being released (see clinical results and upcoming catalysts below). Embryonic stem cells - Early stage promises but still a long way to go

Compared to other cell therapies, human embryonic stem cell (hESC) therapies are still lingering in early to mid-stage development after years of struggle to overcome regulatory and technical issues - as of today, the ethical debate is not over.

The first clinical trial of hESC was authorized by the FDA in 2009 (Geron's spinal cord injury trial), only to be stopped in 2011 when the biotech chose to refocus its resources on other assets. Since then, Geron's stem cell assets were acquired and the spinal cord injury trials are being pursued by BioTime's subsidiary Asterias - a Phase 1/2a trial was started in 2015. BioTime is also developing hESC-based treatment for an eye condition (dry AMD), which is entering a Phase 1/2a trial.

The first (interim) results of a Phase 1/2 open label hESC trial for the treatment of eye conditions (AMD and Stargardt's macular dystrophy) werepublished by Ocata in 2014 and they seems to show that embryonic stem cells work slightly differently than adult cells - e.g. evidence of sustained engraftment has been observed several years after the intervention. Since then, Ocata was acquired by Astellas (OTCPK:ALPMY), which is poised to continue developing the biotech's hESC portfolio. Besides, another Phase 2 trial in AMD was recently launched by the University College London in the UK, with the support of Pfizer (NYSE:PFE).

Although preliminary results appear promising, these hESC eye therapies still lack definitive evidence of efficacy - no hESC product-candidate ever went as far as to deliver Phase 2b efficacy results and it might still take many years to reach commercial stage. However, the promise is huge as it would make it possible to give back sight to blind patients by regeneratingtheir retinal cells - a huge feature justifying continued development efforts.

(Imagesource:University of Utah Health Sciences) Induced pluripotent stem cells - The distant future

As the latest major breakthrough in regenerative medicine, iPSCs have generated a large amount of hope and discussions since their discovery in 2006, mainly because they provide a pragmatic solution combining the potential of embryonic stem cells without the controversy attached.

However, it might well take another decade or more before iPSCs-based therapies could reach the market - at present, the very first (academic) clinical trial using autologous iPSCs in Japan has been stopped pending further research and a probable restart using allogeneic stem cells, as a way to adopt an economically-viable approach which would not have been feasible, according to the researchers, with autologous iPSCs. -

(Source:University of Utah Health Sciences)

Autologous vs. Allogeneic - Developing a viable industrial model

Another important characteristic of cell therapies is the origin of the cells: Those can either come from a patient's own body (autologous therapies) or they can be sampled from healthy donors (allogeneic therapies).

On the one hand, therapies based on fresh or thawed autologous cells imply that samples must be collected and expanded from every patient before treatment, which takes time - that is essentially "personalized medicine" which raises important issues in terms of production costs and availability of products.

Even though efforts are being made to improve the cost/effectiveness profile of autologous therapies, structurally higher cost of goods will automatically require higher pricing to achieve profitability - in the context of soaring drug prices and pressured healthcare systems, this might be a lasting issue for this model. However, for certain chronic conditions requiring repeated administration, autologous cells might be the only feasible treatment because of the body building up immune rejection of donors' cells with time.

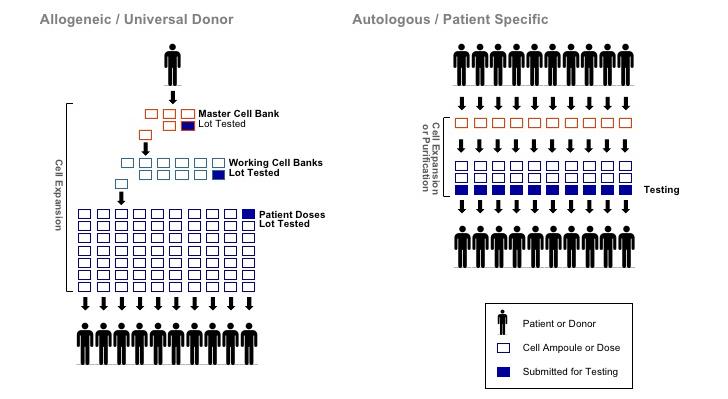

On the other hand, certain conditions require a very quick response: When it is a matter of life or death and the treatment has to be administered at the very onset of symptoms, for example in stroke, acute myocardial infarction or severe sepsis, allogeneic "off-the-shelf" therapies might be the only feasible way of providing a broadly and immediately available therapy to patients. Besides, cheaper and more reliable cell production methods allow for considerable economies of scale in terms of quality control (QC) and logistics - commercially, allogeneic therapies might well be the only viable economic solution in the long term. - Figure 6: Differences between allogeneic and autologous industrial production of stem cell therapies

(Source:Brandenberg et al., 2012)

To sum things up, dealing with allogeneic stem cells instead of autologous ones has several major therapeutic and commercial advantages: Simplified manufacturing processes - Most stem cells can be broadly expanded without losing their characteristics which means that samples collected from a single healthy donor could provide enough stem cells to manufacture thousands of product doses. This reduces production costs and facilitates production scale-up and distribution. On the contrary, autologous cell sampling and testing needs to be carried out independently for each patient, which induces a very high cost of goods and complex logistical issues. Standardization of product - Allogeneic cell samples can be carefully selected from a healthy donor and thoroughly tested before being expanded and packaged. This significantly reduces the risk of relying on the patient's own cells, which could be of variable or lesser quality and could carry the risk of failing QC procedures. Besides, these QC procedures can be robust and more consistent throughout the whole production process with allogeneic products. Off-the-shelf availability - Allogeneic stem cells can be prepared and packaged independently of a patient's need, thus suppressing the time required to expand autologous products before use, which usually requires several weeks (unless bedside devices are used to collect and sort cells, such as Cytori's Celution system).

The industrialization of cell therapies is a whole subject in itself, which will not be developed further in this article (see appendix below for material). However, there is a clear trend observed among biotechs and industry actors towards the "allogeneization" of cell products, based on obvious manufacturing advantages and anticipated gains in profitability.

To expand the scope, investors might also take note of some actors working to improve and industrialize cell production and storage processes, such as Lonza (OTCPK:LZAGY) or BioLife Solutions(NASDAQ:BLFS), which provide interesting exposure to the growth of the whole regenerative medicine sector thanks to their diverse collaborations with stem cell biotechs (including Mesoblast, TiGenix, Capricor, etc.).

Finding value in stem cell biotechs and upcoming catalysts

One of the keys to finding fundamental value in biotechs is to review available clinical data. One of the best ways to anticipate movements in the stock price is to look for upcoming catalysts, including projected data releases. The following tables aim to provide an overview of both past and upcoming announcements in the stem cell sector. Late-stage clinical results for stem cell therapies

In the last three years and for the first time in history, commercial stem cell therapies produced significant late-stage clinical successes. In 2015, the very first successful large-scale Phase 3 trial from an allogeneic stem cell therapy was announced by TiGenix, and many others might soon follow. - Table 1: Overview of late-stage clinical successes of commercial stem cell therapies

(Source: author's own research based on publicly available information)

These results, although still numbered, are essential to show that stem cell therapies can actually bring effective therapeutic answers to very different unmet clinical needs, even on top of current standard of care. Upcoming catalysts in the sector

With an increasing number of therapies having established "proof-of-concept" results in the last years, 2016-17 is bound to be filled with important sectorial catalysts - these will be pivotal years for late-stage clinical results.

One of the busiest areas explored by stem cell therapies is regenerative treatments for heart disease - this is a huge opportunity as an estimated 1.9 million people suffer from heart attacks (AMI) each year in the U.S. and Europe. Even if survival rates for heart attacks improved significantly, these events often lead to the onset of congestive/chronic heart failure (CHF), a chronic, progressive disease with 5-20% annual mortality rate and no existing cure besides heart transplantation. In the U.S. alone, the economic burden of treating heart failure patients was estimated at $31 billion per year and is expected to grow to $70 billion by 2030. The following table provides an overview of upcoming catalysts from heart disease regenerative therapies. - Table 2: Overview of upcoming catalysts of stem cell regenerative heart disease therapies in development (publicly traded companies, as of 2016)

MPCs (Mesenchymal Precursor Cells, bone marrow-derived)

allogeneic

(1) Phase 3 interim results inH2-2016, full results in 2018 (2) Phase 2b results (Class IV) by YE2017

5

Celyad

Cardiopoietic Cells (bone marrow-derived)

autologous

Phase 3 (NYSEARCA:EU) results in Q2-2016 Phase 3 (US) starting in 2016

6

TiGenix

AlloCSC-01 (cardiac stem cells)

allogeneic

Phase 2 interim results in Q3-2016, full results in 2017

7

Capricor Therapeutics

CAP 1002 (cardiosphere-derived cells)

allogeneic

(1) Phase 2 ongoing, 6-month topline results in Q1-2017(end 2022) (2) Phase 1 full results in Q3-2016 (following encouraginginterim results)

8

Vericel Corp.

Ixmyelocel-T (bone marrow-derived mixture of cells)

autologous

Potential partnering for Phase 3 following positive Phase 2 results

(Source: clinical trial database and author's own research based on publicly available information)

Besides heart disease, several other chronic and acute conditions will also have important late-stage results in the next quarters, as shown in the table below. - Table 3: Overview of upcoming catalysts in stem cell therapies (other than cardiac) in development (publicly traded companies, as of 2016)

(Source: author's own research based on publicly available information)

Other sectorial catalysts could also include new pivotal trials or approvals in Japan (where conditional or full approval may be granted following positive Phase 2 data) such as from Athersys' partnered stroke program with Healios or other new commercial deals. In terms of acquisition, it is interesting to note that Ocata was bought out last year for ~$380 million based on a mid-stage pipeline (Phase 2) while many more advanced biotechs are still valued much less despite tangible market perspectives - a sign that valuations in the sector are still relatively modest and could encourage further buy-out deals in the next quarters. The next big challenge - Commercial success

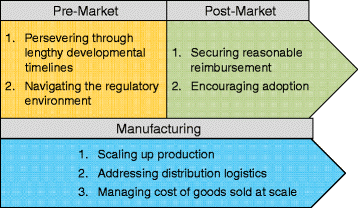

Given the diversity of conditions and cell types being explored, there's little doubt that more stem cell products will successfully reach the market in the coming years. However, as with most breakthrough therapies, there remain some challenges after market approval (see figure below).

- Figure 7: Key challenges of cell therapy development

(Source:P. Dodson & A. Levine, 2015) Widespread adoption - Regenerative medicine is a fast growing market - some reports even project a 33% CAGR or tens of $billions in global turnover by 2020. However, major regulatory agencies including the FDA are still in the process of defining rules for dealing with cell therapies and they are increasingly coming down on unproven claims by so-called "stem cell clinics," which is an encouraging move for the biotech industry but shows that there is still work to do to ensure favorable conditions for serious, clinically proven therapies. Reimbursement - At the moment, the essential question of the reimbursement model adopted for regenerative therapies remains largely unanswered in the U.S. and in Europe. Examples of cell products achieving reimbursement are numbered and often produced mixed results because of high procedure costs which were not necessarily offset by obvious economic benefits (mainly due to the scarcity of data obtained from small trials and/or conditional approvals).

However, the release of increasingly solid clinical data should help making payers agree to higher and broader coverage of cell therapies. Leading the way is Japan, which adopted a cell-therapy friendly regulatory environmentin the last years, granting conditional or full approval and reimbursement upon Phase 2 data demonstrating safety and hints of efficacy (pending completion of post-marketing Phase 3 trials).

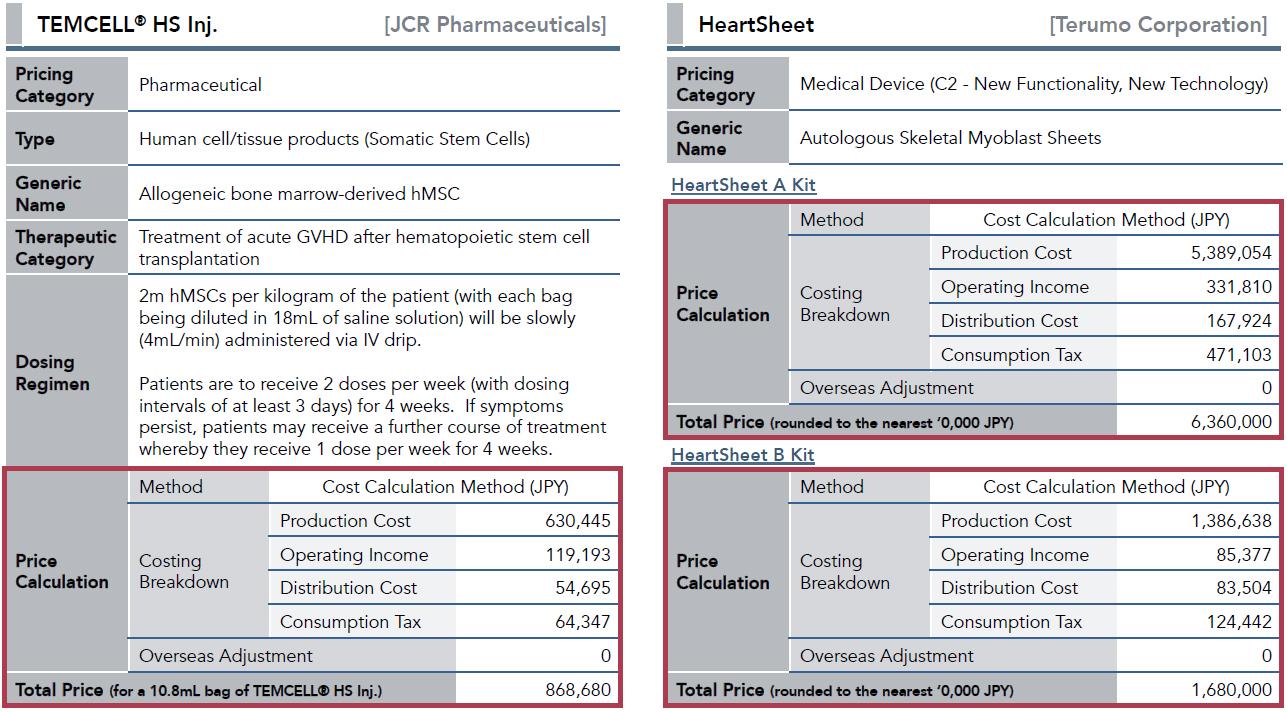

As a result of this orientation, two stem cell therapies were approved and received favorable reimbursement conditions based on Japan's "cost calculation method" (see figure below): TemCell (aka Prochymal, distributed by Mesoblast's partner JCR Pharma) is priced ~$115k to $170k depending on dosage and HeartSheet (produced by Terumo) is priced ~$120k. Depending on insurance plans, Japanese patients will still have to pay anything between 5% to 30% of this price out of pocket. In Europe, TiGenix (with Cx601) and perhaps Celyad (if C-Cure's Phase 3 results are positive) will have to set a highly-anticipated precedent in 2017 - it will be very interesting as both therapies are expected to enter the U.S. market just a few years later.

- Figure 8: Examples of pricing breakdown of cell products approved in Japan based on the "cost calculation method"

(Source:CJ-Partners) Scaling up production and logistical issues - The issues of achieving robust and upscalable production methods and controlling logistical costs for stem cell therapies are intrinsically linked to the two previous challenges (adoption and pricing). Without going into too many details of cell therapy manufacturing, allogeneic therapies are clearly in a more favorable position over autologous products in this matter - for example, TiGenix will be able to provide 2.400 doses of Cx601 in Crohn's fistulas starting from one single liposuction, up to 10.000 doses of Mesoblast's Prochymal (aka TemCell, in pediatric GvHD) can be produced from a single donor and Athersys even claims to be able to generate "millions of doses" of MultiStem from one donor's sample. On the other hand, autologous-based therapies might also have a margin of improvement in terms of scalability - Celyad will be usingautomated systems to produce its patient-specific therapy. Big pharma involvement - To achieve optimal market penetration, one could argue that stem cell biotechs will need the financial and logistical support of big pharma companies. While big pharma involvement in stem cell therapies might have appeared limited during the last years, it has effectively been increasing - among other collaborations, there have been some significant deals such as:

- Teva's partnership with Mesoblast in chronic heart failure (Phase 3 trialongoing)

- Celgene's $45 million investment in Mesoblast in addition to the company's own product, Cenplacel-L (PDA001, placenta-derived stem cells) which has been tested in stroke, Crohn's disease, RA and sarcoidosis

- J&J's (NYSE:JNJ) $337 million option to license Capricor's cardiac stem cell therapy and the company's own ongoing Phase 1/2 trial in AMD with umbilical tissue-derived stem cells

In brief, while there remain challenges, things seem to be finally moving for the cell therapy industry and Japan might be leading the way - the country's aging population is one of the main drivers behind the favorable consideration of regenerative medicine, and Japan is not alone in the industrialized world to be faced with this drastic demographic evolution. This is a pressure neither the FDA nor EMA can ignore much longer - some proposed new regulation in the U.S. would have the country adopt a very similar approach to Japan's regulatory environment, and regulators seem to be well aware of the need to adapt the regulatory framework of regenerative medicine therapies (see this Bipartisan Policy Center report).

Regarding profitability, the high reimbursement prices achieved in Japan might be encouraging for biotech investors in the short term, but this might not be a sustainable system in the long term for healthcare payers. Excessive price tags will limit the uptake of cell therapies, and this is an issue that U.S. regulators are well aware of as reported by the White House itself. In this view, the development of allogeneic stem cell platforms gives hope of achieving reasonable CoGS and affordable selling prices. Meanwhile, Mesoblast confirmed in its latest quarter report that it had just received the first royalty payments for TemCell's sales in Japan... Conclusion: the inflexion point?

The advent of stem cell therapies has been decades in the making. Although developing a new drug typically takes 10 to 15 years from early preclinical work to market approval, early-stage stem cell clinical trials were surrounded by a lot of hype, but unfortunately, convincing efficacy results did not materialize immediately. This had a lasting negative impact on many investors' consideration of the sector as a whole. The technology had to progress further and therapeutic goals had to be adjusted - stem cells were not actually going to cure cancer and heart attacks overnight.

However, as shown in this article, things are really moving on and regenerative therapies are finally getting out of the clinic, offering relevant treatment options for chronic and acute conditions. While there remain some uncertainties regarding the full commercial transition of cell therapies, the industry is progressing in the right direction and good data is starting to pile up. Besides, the global regulatory environment is becoming less harsh for cell products and the first commercial stem cell therapies have secured very high reimbursement prices in Japan.

So, is it really the right time to invest in stem cell biotechs? While small-cap biotechs generally remain very risky bets, now might be a good time indeed to get to know the field as the more advanced stem cell biotechs appear still cheap despite commercial perspectives that have become very tangible. Several promising products will arrive on the market very soon (Mesoblast's Prochymal in the U.S. in 2018, TiGenix's Cx601 in 2017 in Europe and 2019 in the U.S., etc.) and major Phase 3 results are expected in the coming months, with another string of late-stage data expected in the next 2 years: this might be the inflexion point the stem cell industry has been waiting for ..............................-Vin

MSB Price at posting:

$1.92 Sentiment: Buy Disclosure: Held

A personalised tool to help users track selected stocks. Delivering real-time notifications on price updates, announcements, and performance stats on each to help make informed investment decisions.

(20min delay)

(20min delay)