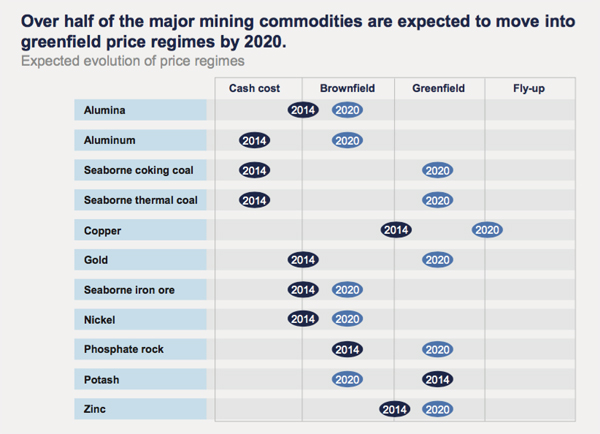

Thanks to another poster for this. It really puts CSD in an enviable position, with huge copper resources ready to go when required and tin (not on the list) to carry the project forward to that date. Zinc is also expected to become interesting and has kept company in a reasonable position for the near term, thanks to the Aussie dollar.

This table sums up the outlook for each commodity and shows even the most downtrodden commodities like coal, iron ore and nickel have sunny outlooks, while copper could soar.

Cash cost – price levels are close to the cash cost of the marginal producer, and there is minimal incentive to invest.

Brownfield inducement pricing – high enough to justify extending the life of existing mines.

Greenfield inducement pricing – would justify investing in new greenfield projects.

Fly-up pricing – demand grows so fast and capacity utilization is so tight that prices temporarily soar well above levels dictated by the cost curve.

The poster is from the RVR thread and I believe article is from MineLife? Apologies if incorrect, iPad glitches.

Thanks to another poster for this. It really puts CSD in an...

Add to My Watchlist

What is My Watchlist?