The broad decline across the US sharemarket underscores a fresh risk-off move in global financial markets as bond yields climb before forecasts of Federal Reserve interest rate increases this year.

All sectors but energy fell in US trading on Tuesday, dragging the S&P 500 into negative territory. Tech stocks weighed heavily on the benchmark.

The action left “investors with nowhere to run or hide”, warns NAB analysts, as bond yields climb, creating a “sea of red” across the equity markets.

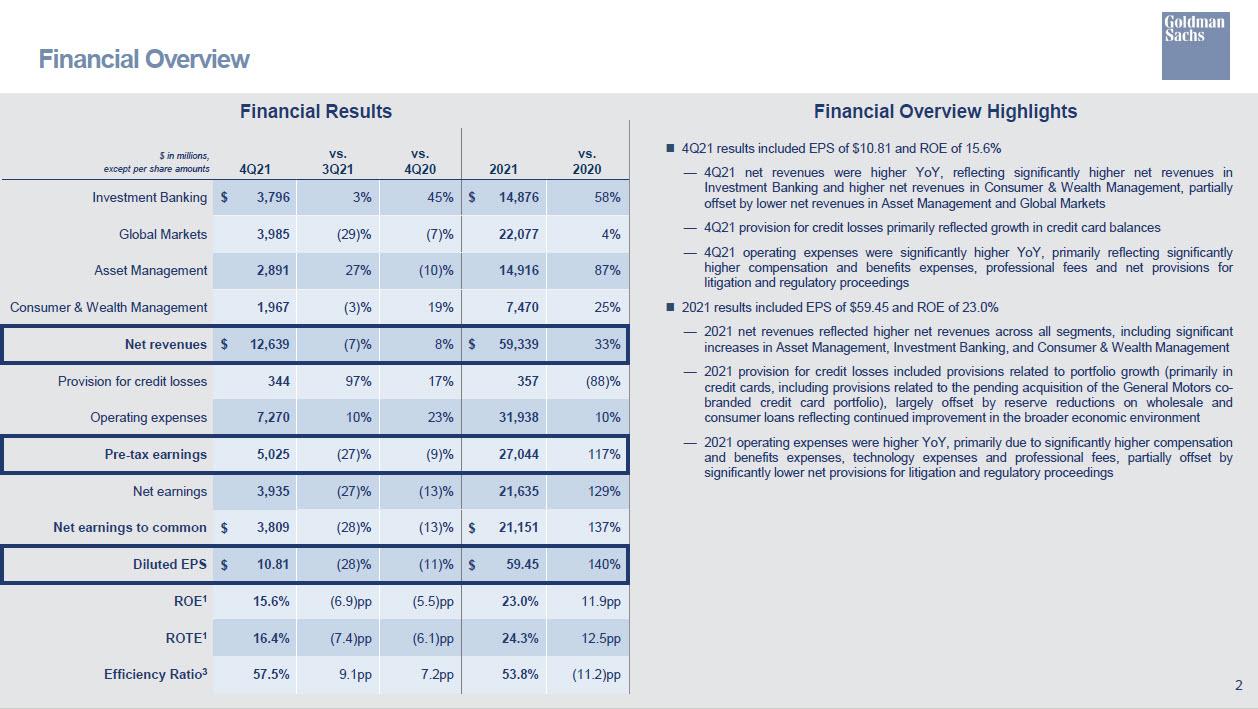

“A broad rise in US Treasury yields has been one factor dampening sentiment while a disappointing Goldman Sachs earnings report weighed on financials,” NAB says in a morning note.

US bond yields hovered around two-year highs on Wednesday morning in Sydney, as investors begin to price in four rate jumps by the Fed, with a chance of a fifth and also growing potential for a 50 basis point rise in March, double the typical increase.

Psaki Says Russia Attack On Ukraine Coming "At Any Point"; US Sanctions 'Pro-Russian Agents'

BY Zero Hedge

TUESDAY, JAN 18, 2022 - 04:10 PM

White House Press Secretary Jen Psaki in a Tuesday afternoon daily press briefing said "We believe we're now at a stage where Russia could at any point launch an attack on Ukraine. I would say that's more stark than we have been."

She confirmed that Secretary of State Antony Blinken will meet with Ukraine's President Volodymyr Zelenskyy in Kiev this week, just after it was recently revealed that CIA Director William Burns did the same last week. "What Secretary Blinken is going to do is highlight very clearly that there's a diplomatic path forward,” Psaki said. "It is the choice of President Putin and the Russians to make whether they are going to suffer severe economic consequences or not."

"No option is off the table" if #Russia "further invades Ukraine," @PressSec tells @WhiteHouse reporters. "We're now at a stage where Russia at any time could launch an attack on Ukraine." pic.twitter.com/mTEesS4oCg

— Steve Herman (@W7VOA) January 18, 2022

Goldman lost money while the S&P500 made record highs? Goldman Lost $500MM Trading Stocks In Q4 As It Quietly Sold Even More Billions In Equities

BY Zero Hedge

TUESDAY, JAN 18, 2022 - 01:05 PM

While most analysts and traders were digging through Goldman's disappointing Q4 earnings report which missed on EPS and trading revenue, and focusing on the investment banking and markets (i.e., commission-based flow trading ) results as well as the ominous surge in expenses...

... which sent Goldman stock price plunging, for the second quarter in a row there was troubling disclosure in the bank's Asset Management division, formerly known as Goldman Prop.

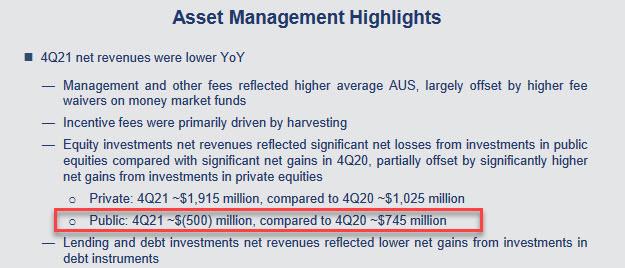

Here, after a stellar Q2 in which Goldman generated a record $5.132BN, more than double the $2.1BN in Q2 2020 and driven by "significantly higher net gains from investments in private equities, driven by company-specific events, including capital raises and sales", and after a very disappointing Q3 which saw a $820 million loss from the trade of public equities, Q4 saw a continuation of this bizarre underperformance, with net revenues sliding 10% from a year ago, with revenue from Equity Investment plunging 20% Y/Y to just $1.417BN.

According to Goldman's investor presentation, for the second quarter in a row, "equity investments net revenues reflected significant net losses from investments in public equities compared with significant net gains in 4Q20, partially offset by significantly higher net gains from investments in private equities."

Goldman further breaks down the equity revenue, and notes that whereas investments in private equity brought in $1.915BN, more than even the $1.755BN in Q3, public equities actually led to a whopping $4500 million loss in Q3, compared to $745 Million profit a year ago, and a $820 Million loss in Q2.

Wait, "significant losses" from investments in public stocks in Q4, a quarter in which after a few modest drawdowns, the S&P soared to a new all time high on Dec 31 courtesy of a furious Santa Rally. Or... was Goldman short the market as it ripped higher in Q3?

Surely someone on the Goldman call would or should ask this question, although we doubt it - in fact, this will be the second quarter in a row in which not a single person inquire as to how Goldman - the most powerful and influential bank in the world - has lost hundreds of millions from trading stocks.

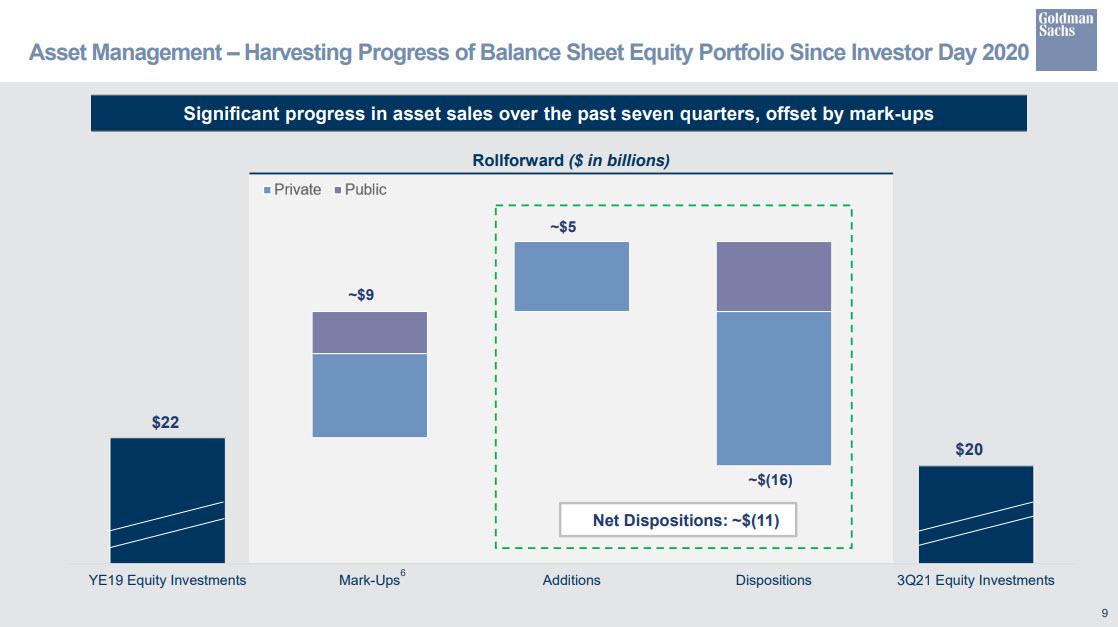

But if they don't ask about how Goldman lost half a billion trading stocks, surely someone will ask why the bank keeps dumping stocks, pardon "harvesting" gains, hand over fist. After all, this is the third quarter in a row this has taken place.

Recall, two quarters ago we reported that "Goldman Has "Aggressively" And Quietly Liquidated A Quarter Of Its Equity Investments" showing that "having started the year with a $20BN equity portfolio which has enjoyed a $5BN increase in market prices, Goldman dumped a whopping $5.5 billion of its equity assets so far (excluding a modest $1.5BN in purchases) or more than a quarter of its entire portfolio as of Dec 31. "

Then, last quarter, the infamous "harvesting" slide was back if with some adjustments. First, Goldman no longer used YE20 as the starting point for its asset sales bridge, and instead has picked YE19 as the starting reference. Back then the bank had some $22 billion in equity investments, $2BN more than the $20BN at YE 20. What we also found is that unlike Q2, when the bank showed it has sold a whopping $5.5BN in stocks in the first half of 2021 (excluding a modest $1.5BN in purchases), this time the bank went even bolder and sold a total of $16 Billion (presumably split between equities and debt, although whoever did the chart forgot to add the table). This number was offset by $5 billion in equity additions, for a total Net Dispositions amount of $11 billion, or "harvesting" since the bank's 2020 Investor Day.

So fast forward to today, when the "Harvesting Progress" slide is back and shows that the bank sold an additional $2BN gross in Q4 (the dispositions number since YE19 rose from $16BN to $18BN), offset by an incremental $1BN in purchases ($6BN in Q4, up from $5BN in Q3). In other words, all else equal (and as the slides above and below show that's more or less the case), Goldman liquidated, pardon "harvested" an additional gross $2BN in Q4 offset by $1 billion in the bank's equity portfolio, for a total Net Dispositions amount of $12 billion, or "harvesting" since the bank's 2020 Investor Day (up from $11 billion last quarter).

Who is Goldman selling to? Anyone who will buy, but here we would wager that retail investors - who were on tilt buying in 2021 - have been the proud recipients of billions in Goldman sales, especially those reading the permabullish notes from Goldman's chief equity strategist David Kostin (curiously, Goldman's "harvesting" asset management group did not get access to those). This, in the financial literature is called the "distribution phase."

Unfortunately, with the investor call now over, there were virtually no discussion of harvesting this time. At least two quarters ago some analyst asked a question about Goldman's efforts to reduce its equity investment portfolio, to which the bank said that it it has "made progress on improving its capital efficiency and is moving 'aggressively' to manage equity positions, especially since the environment is supportive."

What does that mean in English? Simple: in Q4, Goldman continued to "aggressively" dump its positions which are in the money in an environment that is "supportive", i.e., in which the dumb money is providing a constant bid into which whales such as Goldman can sell.

The last time Goldman was "aggressively" selling into a "supportive" market? Well, we have to go back all the way to 2007 and 2008 when Goldman was busy creating the very CDOs which its prop desk would then "aggressively" short. We all remember how prophetic that particular move turned out to be.

As to what was behind Goldman's unexplained $500 million equity loss, one wonders if Goldman's wasn't one of those who were steamrolled by the sequence of powerful, if increasingly rare, short squeeze observed during the past quarter... ironically just as predicted by the bank's very own flow traders.