...the trauma that Powell went through in Christmas 18 when he had to do a complete U turn after hiking rates causing a market collapse probably remains with him...so what he is doing is buying time just as he did with "transitory" hoping for inflation to peak and go lower so he does not have to be as hawkish. Signaling to the market that we can have two 50bps rate hikes over coming 2 months with no 75bps in the horizon and doing a more modest $47B QT immediately and deferring the larger $95B QT into Sept is pushing the can down the road and certainly makes the final quarter a likely quarter that we could see a market crash.

...in the interim he would be hoping the market does not get too exuberant on the news to be in a position where a market crash becomes more imminent.

...plus dont forget this is a crash the US Govt would want to avoid leading to mid terms

Stocks Soar To Best Fed-Hike-Day Performance In 44 Years

BY Zero Hedge

THURSDAY, MAY 05, 2022 - 06:00 AM

Tl:dr: This was the biggest gain on a Fed day since Dec 2008 (a rate-cut day), but this was the greatest upside-day for the S&P 500 on a Fed Rate-Hike day since Nov 1978!!

And here's what happened last time the S&P rallied this much on a Fed rate-hike day... (we made new lows)

* * *

"Inflation is much too high," warned Fed Chair Powell in his opening words, in an effort to assure the American people - and the markets - that they are really really serious this time, pinky-swear, about hiking even if the market pukes its guts out... (or not).

Powell: "It is important that they know that we know how painful it is."

You mean the pain you caused when you said it was transitory for 9 months straight!?

— zerohedge (@zerohedge) May 4, 2022

The market did not like that news (stocks fell, yields rose, rate-hike-odds rose)

But then Powell tried to assuage fears of a 75bps hike:

"A 75 basis point increases is not something the committee is actively considering," but noted that the "next couple of meetings" will be 50bps hikes.

The market loved that news (stocks surged, USD dumped, yield curve steepened with short-end yields plunging)... monkeyhammering all the risk away (VIX crashed to a 24 handle)...

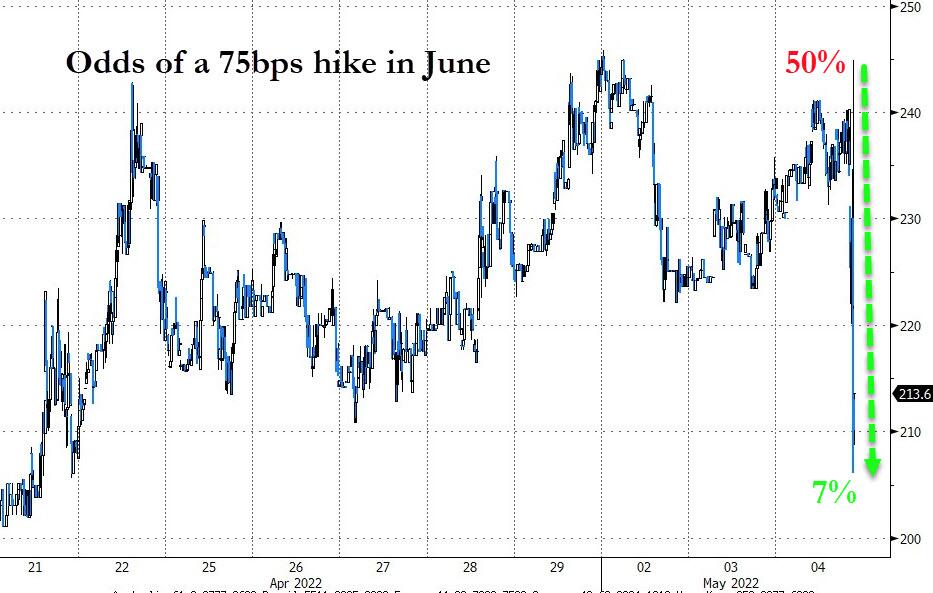

STIRs immediately priced-out the odds of a 75bps hike in June...

Source: Bloomberg

And the rate-hike-trajectory also dropped on Powell's more dovish tilt...

Source: Bloomberg

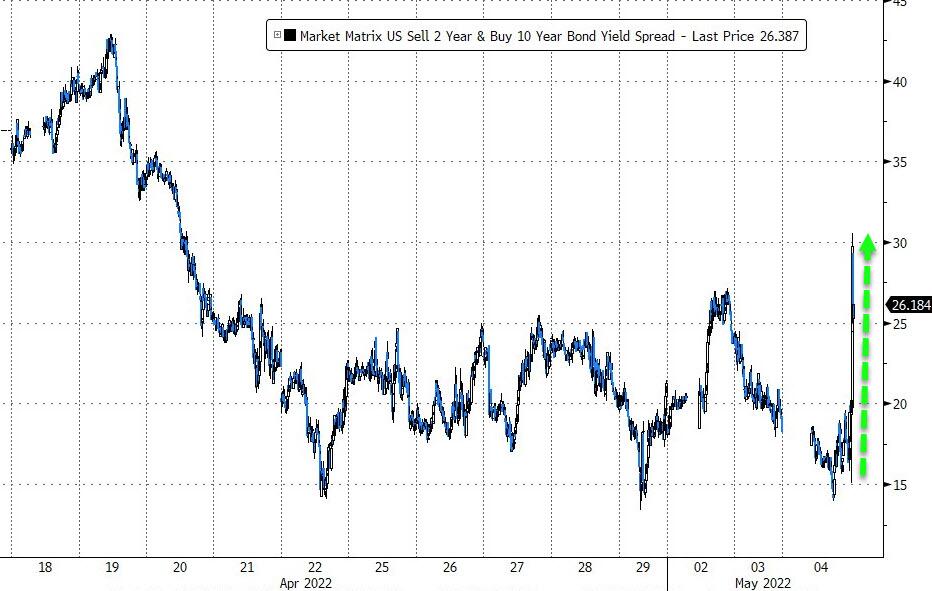

The short-end of the yield curve collapsed (2Y -13bps, 30Y -2bps)...

Source: Bloomberg

...and the yield curve steepened drastically...

Source: Bloomberg

Notably Bloomberg's Ira Jersey warned that "The market may be interpreting the lack of a 75-bp move incorrectly as ‘dovish’ given the strong rally in the front end of the yield curve. A string of 50-bp hikes, without a 75-bp move, could actually mean a higher terminal rate and over time may not mean much for the short end of the yield curve. There could be an opportunity building in the curve.”

Additionally, Powell warned The Fed could act "expeditiously" - which could easily mean more than three 50bps-hikes are in order if inflation remains high.

10Y Yields reversed once again at 3.00% (exactly where they did in Dec 2018 before Powell folded)...

Source: Bloomberg

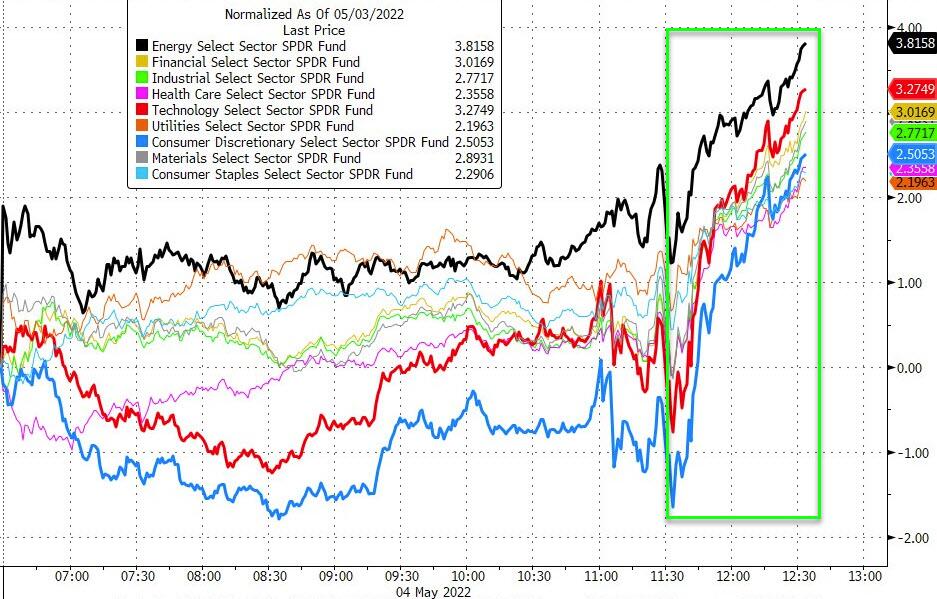

Stocks went utterly vertical on the 'lack of 75bps move' (as the dramatically oversold/over-hedged positioning unwound again)...Yes, the Nasdaq exploded 3.5% higher on the day (from down 1.5% this morning)....

'That escalated quickly..."

All the sectors shot higher, led by tech and discretionary (but energy was best on the day)...

Source: Bloomberg

...apparently ignoring the fact that they are not at all priced for a series of 50bps hikes...

Source: Bloomberg

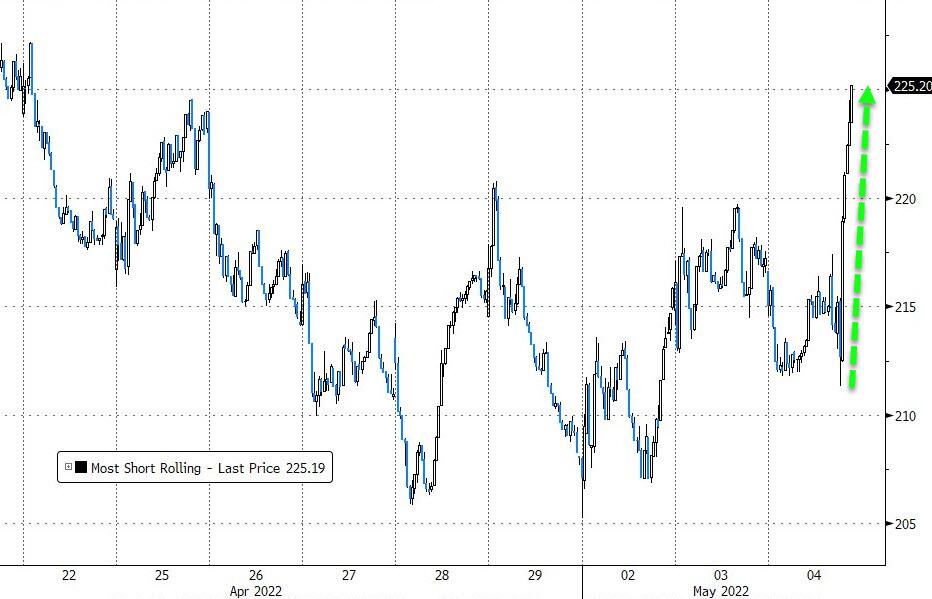

The chart above shows what happened after the last FOMC meeting - will we see another melt-up squeeze? This afternoon saw a serious short-squeeze begin...

Source: Bloomberg

So that's it then... The Fed has the problem in hand and a soft landing is now priced in (and a hard landing, in case we dip again).

At this rate, stocks will be at ATH by Friday and Fed speakers will be throwing around emergency 100bps rate hikes

— zerohedge (@zerohedge) May 4, 2022

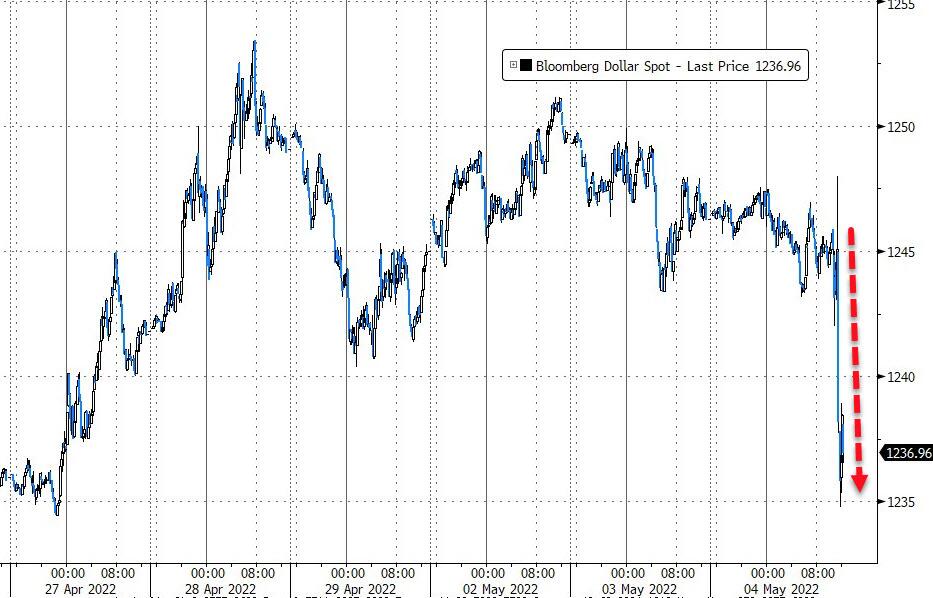

The dollar tumbled during the press conference...

Source: Bloomberg

The Ruble soared to its strongest relative to the USD since Feb 2020...

Source: Bloomberg

Oil prices soared on the day on the heels of EU embargo headlines - erasing all of Biden's 'improvements' in price...

Finally, Powell admitted that The Fed is useless:

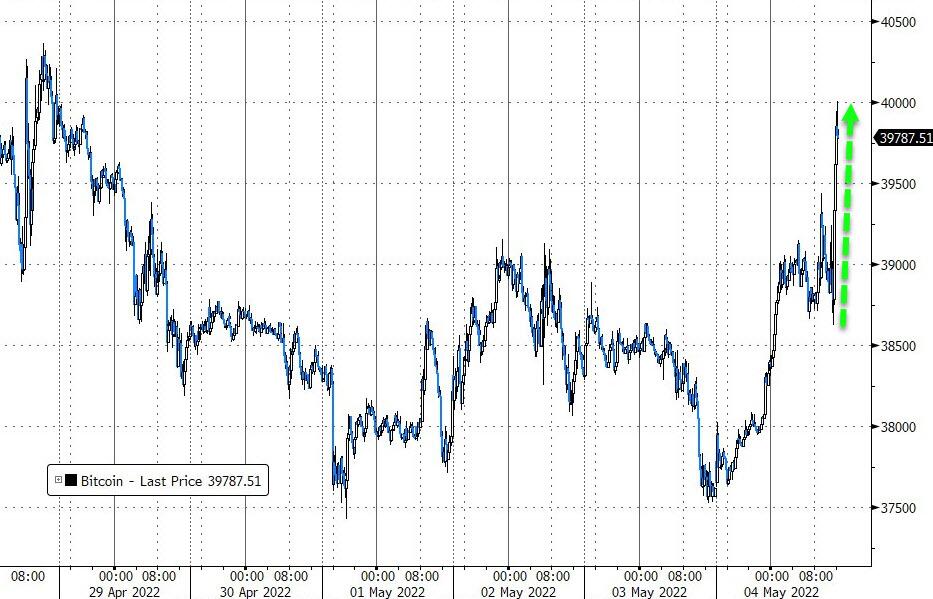

"Our tools don’t really work on supply shocks, our tools work on demand."

Which could be why Bitcoin quickly ripped up to $40k...

Source: Bloomberg

Gold was also bid on his comments...

As hard as Powell tried to rescue his credibility, crypto and gold exposed the lie.

*POWELL SAYS `NO, I DON'T' THINK FED HAS CREDIBILITY PROBLEM

Narrator: what credibility

— zerohedge (@zerohedge) May 4, 2022

As one veteran trader noted: "it seemed like Powell reverted back to his 'inflation is transitory' perspective... good f*ing luck with that!"

Parsing the Fed’s decision and Powell’s comments

Timothy Moore

The Fed’s policy committee voted for a 50 basis point rate increase, and chairman Jerome Powell signalled two more 50bp increases would follow in June and July, then the central bank would shift to 25bp increments.

Here are some views of the overnight news:

NAB’s Ray Attrill, head of FX strategy, markets: “You might be forgiven though for thinking the Fed had just signalled that it might soon be done tightening (!) though in the context of how much equity markets had fallen in April and the reasons behind it, arguable it is more a case of a market that heavily ‘sold the rumour’ now buying the fact of the Fed’s may actions.”

Ian Shepherdson, Pantheon Macroeconomics: “We think a 50bp hike is very likely in June—but it’s not a done deal— but after that we think all bets are off, precisely because we do expect a steep, sustained drop in inflation, starting with next week’s April report.

“At the same time, we also expect a clear softening in manufacturing, and a meltdown in housing market activity, all of which suggest that a third straight 50bp hike, in July, is less likely than markets thought before the meeting. Judging by the drop in two-year yields during the press conference, markets are beginning to have a re-think about the idea of a long string of 50bp increases.”

Bank of America: “At this stage, we believe the Fed has pivoted to an appropriately hawkish stance and is likely done surprising markets for a while. We recommend focusing more on the data flow going forward, especially around labour and inflation.”

BofA also said: Powell “noted that 50bp rate hikes would be on the table for the next two meetings, while dismissing the idea of an even bigger 75bp increase. Moreover the Fed would not hesitate to raise rates above neutral -between 2-3 per cent-into restrictive levels if warranted. This would be in line with our current base case of additional 50bp hikes in June and July and then 25bp rate hikes at every meeting thereafter; we think ultimately raising the fed funds rate to 3.25-3.50 per cent by May 2023. At the end of the day the Fed is committed to restoring price stability.”

Oanda’s Edward Moya: “US stocks surged after Fed chairman Powell signalled he can slow inflation without triggering a recession. It seems risky assets can rally now that Wall Street has fully priced in the rest of the year’s rate hikes by the Fed.”

Jeffrey Roach, chief economist at LPL Financial: “Recent actions by the [Fed’s policy committee] confirms the base case scenario that the markets incorrectly priced in huge aggressive Fed action this year.”

Roach also said it was important to note that the decision was unanimous, as in James Bullard did not dissent with a vote for a higher increase like he had intimated. “Reading between the lines, I see this as net positive for markets.”

Jamie Cox, managing partner at Harris Financial Group: ”Powell had a third mandate today--and that was to dispel the notion of a 75bps rate increase.

“This is not the Federal Reserve of the 1970s, where every excuse was given about why inflation was high,” Cox also said. “This Fed, under the direction of Powell, is owning inflation as a problem and is intent upon fixing it. The first and most important tool of inflation fighting is credibility--and Powell established that today.

“Powell went a long way toward quelling market worries about a policy error by the Federal Reserve which slams the brakes not the economy and precipitates a sharp recession, which is anything but a ‘softish’ landing.”

Kathy Bostjancic, chief US economist at Oxford Economics: “While we didn’t believe the Fed would raise rates by 75bps rate increments, if the Fed wants to ‘expeditiously’ tighten policy and financial conditions, we question whether Powell should have removed the speculation of 75bps rate increases at upcoming meetings. Maybe he’s trying to thread the needle to achieve a ‘soft landing’ by avoiding an overly rapid tightening in financial conditions.”

Sonders sees recession risk, reason for caution

Timothy Moore

In her review of the Fed developments, Charles Schwab chief investment strategist Liz Ann Sonders indicated she’s hesitant to embrace the Fed’s optimism as well as the initial market enthusiasm.

“Although the Fed addressed the contraction in the economy in the first quarter, it focused more on the strong gains in final sales to households and businesses. For what it’s worth, we believe the risk of recession is elevated and should not be dismissed. Expectations are that the Fed will hike rates by a similar amount at the next couple of FOMC meetings.

“Stocks were choppy-to-weak following the announcement, but began to rally as the press conference unfolded. We expect continued bouts of volatility associated with both monetary policy and the trajectory of inflation and economic growth. Courtesy of still-strong earnings growth, and a weak four-month start to the year, valuations have come down notably. However, expectations looking ahead are for another deceleration in growth in the second quarter, as well as a likely long-awaited hit to profit margins.

“We continue to recommend investors keep portfolio risk to levels no higher than strategic asset allocations, remain diversified (across and within asset classes), focus on high-quality fundamentals, and utilise periodic rebalancing to take advantage of volatility by ‘adding low and trimming high’.”

US equities rally ‘too exuberant’: El-Erian

Timothy Moore

In a series of three tweets, Mohamed El-Erian offers his view of the reaction to the Fed’s policy meeting and Jerome Powell’s comments.

“This afternoon’s sharp downward move in yields for the shorter maturity US government securities is consistent with what I had cautioned in recent weeks was an excessive market pricing of #Fed rate hikes. Importantly, however

“… this is not because such hikes are not needed to tame #inflation quickly consistent with the Fed’s 2 per cent target. They would be if the starting point was not so problematic. One big issue is that the #FederalReserve is already very late in responding. As such, the Fed’s …

… potential non-validation of the prior forward curve would be linked more to the potential adverse impact on growth … making today’s equity market reaction too exuberant if this analysis is indeed correct, and also making the #growth and #inflation outlook far from linear. 3/”

...the trauma that Powell went through in Christmas 18 when he...

Featured News

Featured News

The Watchlist

NUZ

NEURIZON THERAPEUTICS LIMITED

Dr Michael Thurn, CEO & MD

Dr Michael Thurn

CEO & MD

SPONSORED BY The Market Online