...As I said the market is full of trickery and once again we have been blindsided by yesterday's post-Fed rally which you have to say was rather impressive which led me to wrongly and prematurely suggest yesterday that the May threats may be over and that the market crash could be pushed down the road to the last quarter of this year, but I also said that market participants would remain wary, while adding an article to suggest not to get sucked in into the post Fed rally. Not only were US market participants wary, they voted with their feet down to suggest that Powell is wrong and has been Behind the Curve and Behind the Curve he has been as contrary to his FOMC statement that labour costs would not be an issue, unit labour cost turned out to be +11.6% q-o-q against consensus of +9.9% and previous +1% and non farm productivity substantial lower -7.5% vs -5.4% estimate.

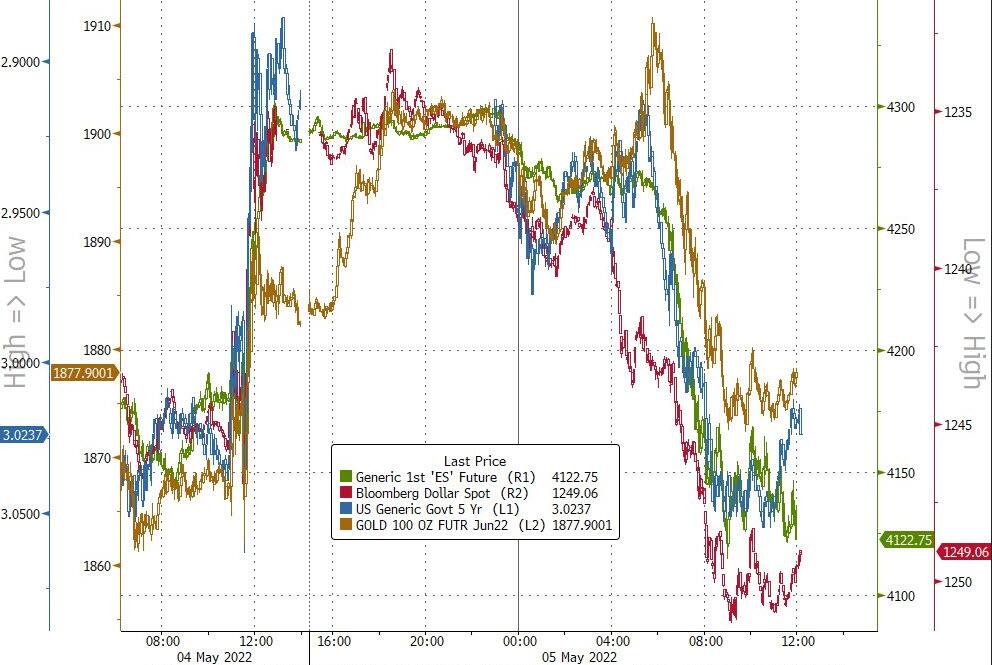

And we saw 10 year yields rising sharply to 3.1% before settling at 3.035% causing markets to plunge in its sharpest fall since March 2020. Dow was lower by 1063 pts or -3.12%m S&P500 153pts down or -3.55% to 4147 and Nasdaq plunged 4.99% to 12317.

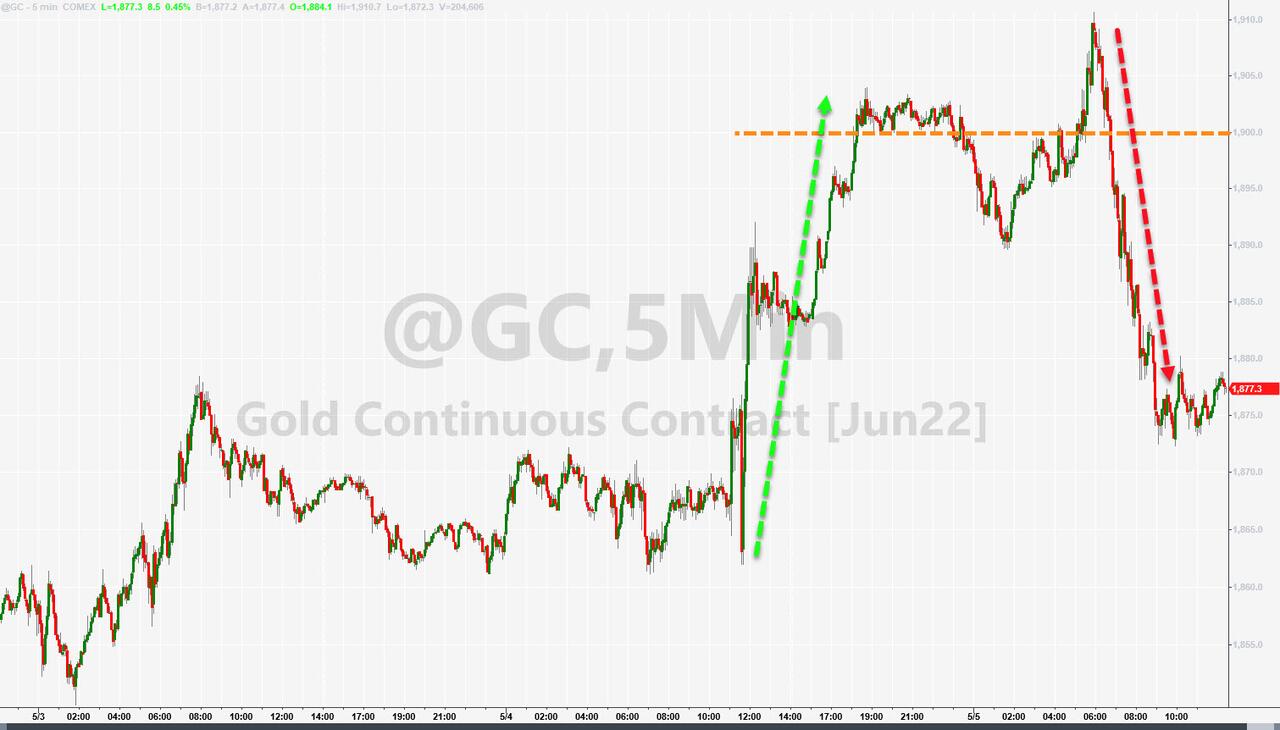

Basically, all the gains and more from the day before were wiped out, monsters of tech stocks hammered, Tesla -8.3%, Amazon -7.5%, Apple -5.57%, Microsoft -4.36%, Meta -6.77%, Alphabet -4.75%, the XLF -2.91% and banks broadly lower by 2.5-3.5%. Gold retraced from its 1900 level to 1877 but gold equities bore the brunt of the pullback with GDX lower by 3.2% and GDXJ -4.19% and silver stocks smashed too by 4.7-5.5%. BTC crashed 8% to $36.5k and poised to test $35k. And AUD the clear barometer of Risk On/Off fell from a height of 72.6c to a low of 70.6c before settling now at 71.1c.

In my earlier post, I suggested a test of 4000 on the S&P500 on the cards with probable falls to 3800 if 4000 does not hold. Looking at the instability of this market, it would not surprise me if the Fed would allow a bear market to be registered on the S&P500 circa 3850 and lower to kill off remaining exuberance , so that it can engineer a softer landing on the equity markets while proceeding with its rate hikes into the months ahead. Another 5-10% fall on the S&P500 is tolerable if the prize is to kill exuberance so that the market do not get wildly high again to threaten a super market crash thereafter that could prove systemic and which the Fed would want to avoid at any cost.

Well, I warned on this thread since last quarter last year with my train wreck rhetoric, and why it would pay staying on the sidelines. Our ASX has a lot of catch up to do and 7000 test was my earlier prediction, so again it would not surprise me market participants would want to wait to see lower prices before starting to act, as I had mentioned best to act ahead and now stay glued to prices especially what the indices indicate.

Sinko De Mayo: Post-Powell Panic-Bid Hangover Prompts Panoramic Pukefest

BY Zero Hedge

FRIDAY, MAY 06, 2022 - 06:00 AM

Tl;dr: The bond market just told Powell (and the stock market), "you're wrong!"

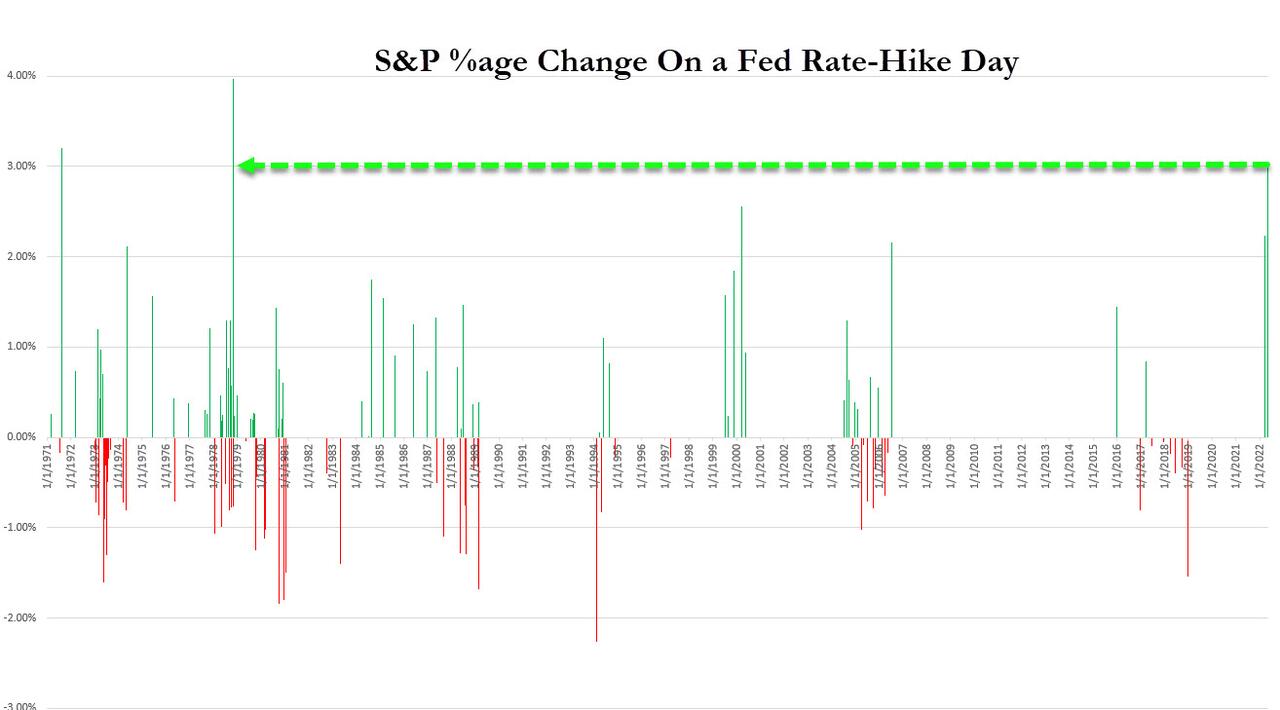

Remember yesterday was the best performance for a Fed rate-hike day since 1978!

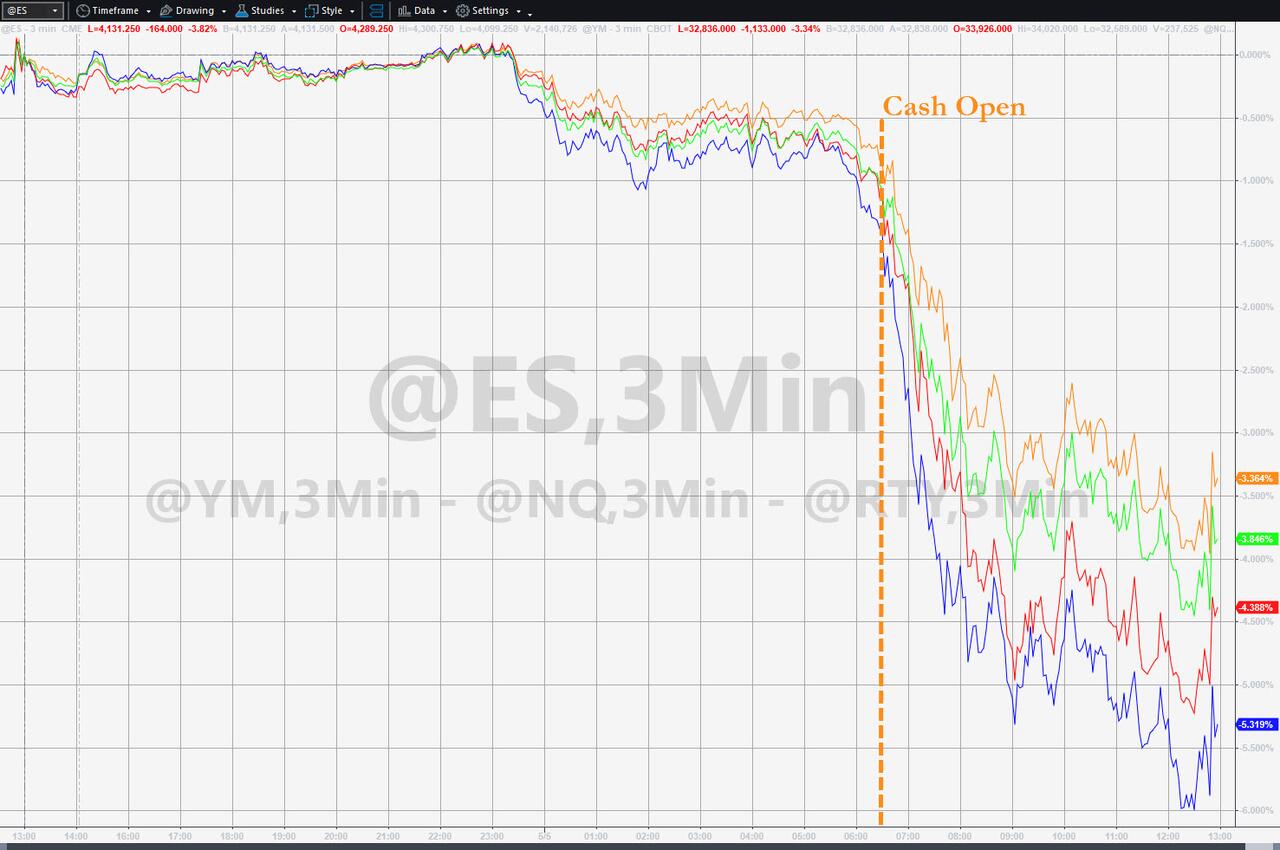

And today, the Nasdaq 100 Index fell 6% at its lows, the most since March 2020...

...fully reversing yesterday's post-FOMC gains.

Notably this 2% or so drop in the S&P 500 in the two days of a Fed hike and the next is on par with the drop that happened in Dec 2018 and prompted Powell to reverse his hawkish stance.

We note that the S&P stopped at 4099.25 - which is max negative gamma - just one giant ping-pong game.

Within a week we’ve now seen two of the biggest 24-hour turn-arounds for the index since 1985.

In the past week we have had:

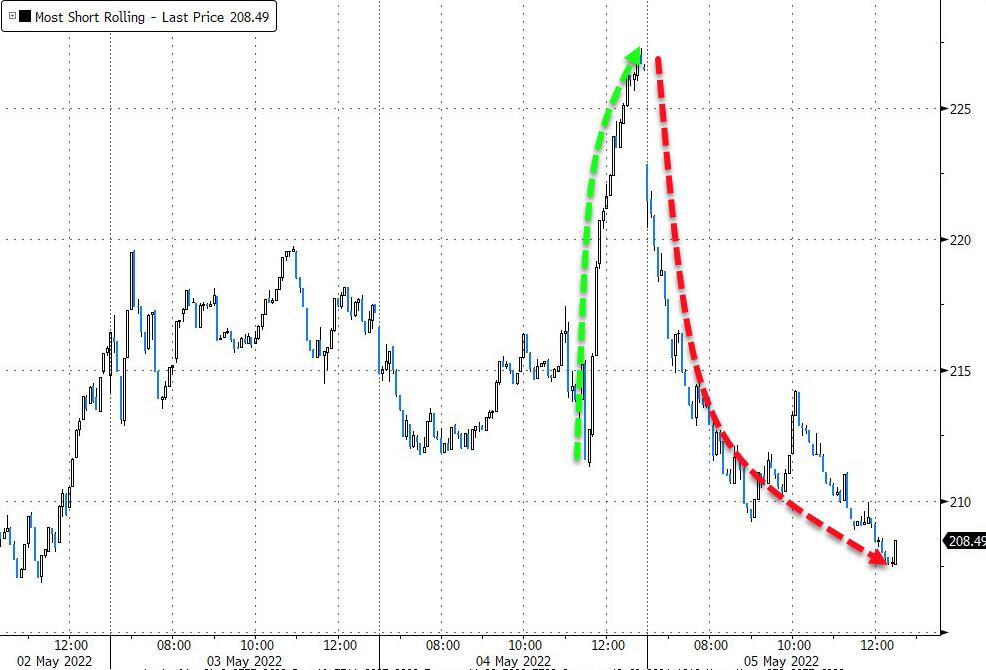

As yesterday's massive short-squeeze is unwound instantly Today was the biggest drop in 'most-shorted' stocks since Feb 2021's peak after the record meltup...

- Friday: biggest drop since June 2020

- Wednesday: biggest surge since May 2020

- Thursday: biggest drop since June 2020

Source: Bloomberg

As Jason Goepfert notes, there have been 2 days in the past 25 years when S&P 500 futures were down 3% and 10-year Treasury futures down 1%:

Someone is blowing up, and this is forced liquidation.

- October 9, 2008

- March 18, 2020

Source: Bloomberg

Paging...

It seems the market is 'stuffed' full of The Fed's bullshit...

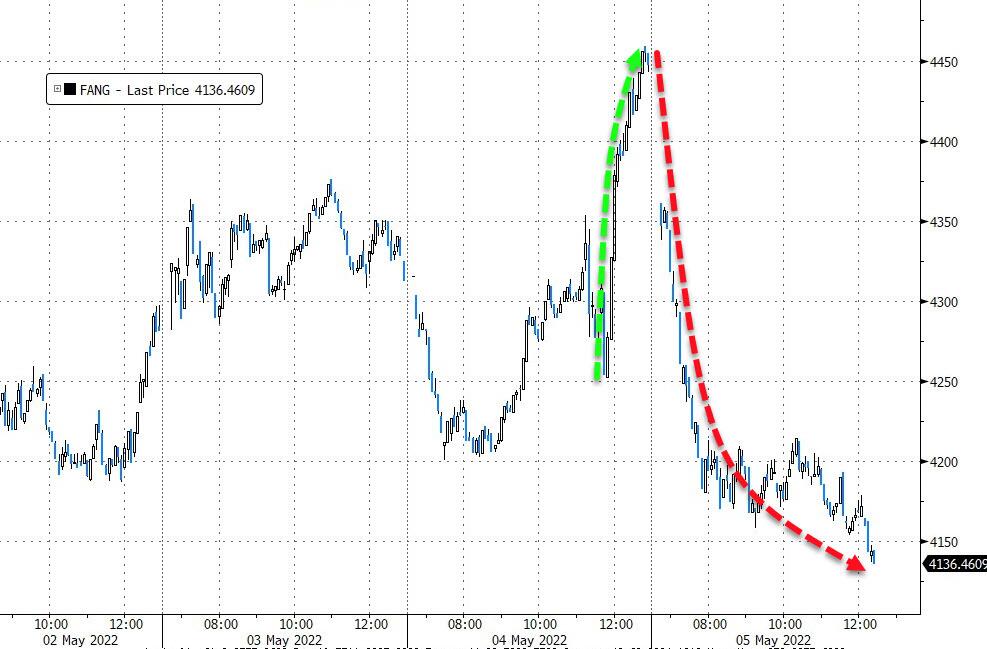

Energy is holding gains while tech and discretionary has been hammered over the past two days...

FANG stocks puked hardest...

Source: Bloomberg

VIX exploded back above 32 today...

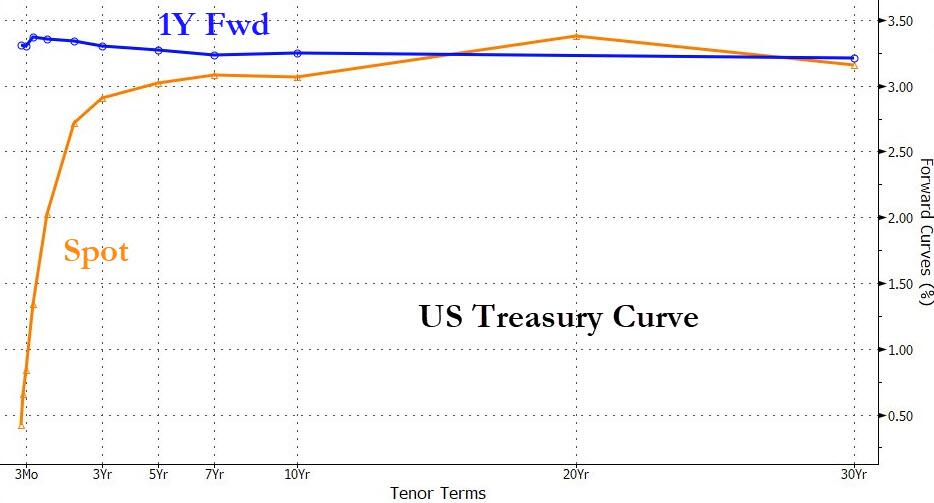

Treasuries were clubbed like a baby seal today with the long-end underperforming (30Y +13bps, 2Y +6bps), massively unwinding yesterday's moves...

Source: Bloomberg

The entire curve from 4Y out is above 3% (and 1Y fwd, the entire curve is inverted)...

Source: Bloomberg

Like everything else, the dollar round-tripped from yesterday's losses...

Source: Bloomberg

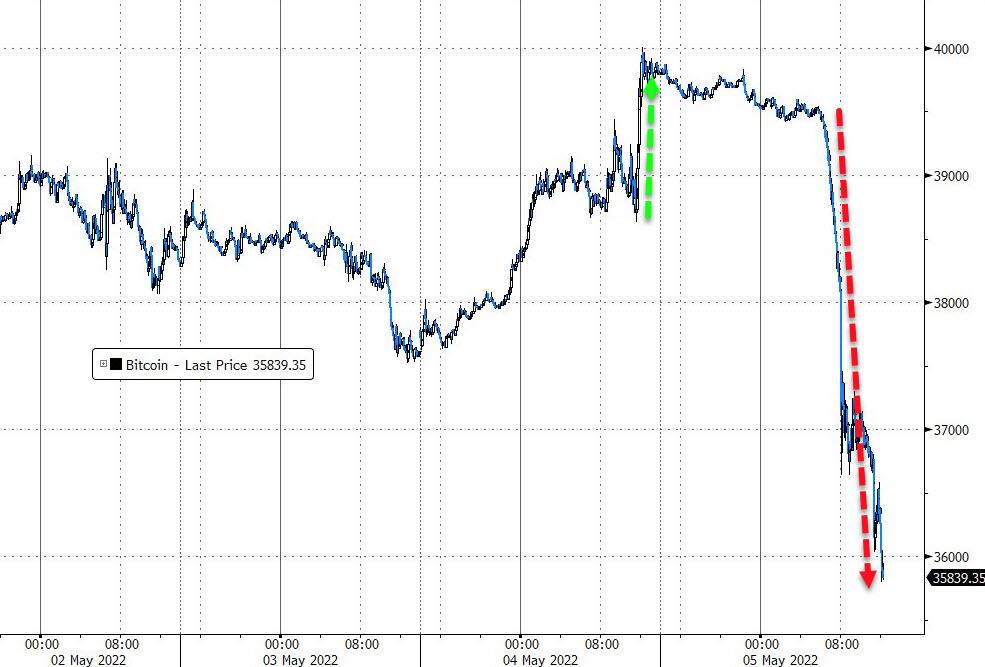

Bitcoin was a bloodbath, smashed back below $36k for the first time since Feb 22...

Source: Bloomberg

Gold topped $1900 overnight but as the selling pressure escalated during the day, gold plunged back below, erasing all post-Fed gains...

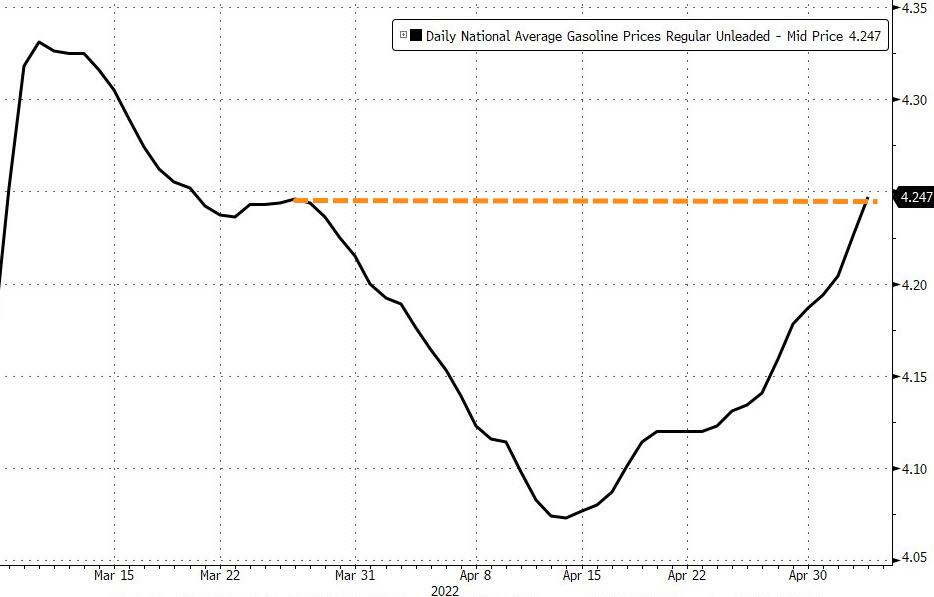

Oil ended higher on the day after the Biden SPR news...

The Biden admin decided it was time to start refilling the SPR that they planned to empty to bring down oil (and thus gasoline) prices... Sadly for them, pump prices are now back above their cunning SPR plan levels...

...and are due to make new highs very soon...

Source: Bloomberg

Who will Biden blame this time?

Finally, what happens next?

Yesterday: All puts monetized

Today: everyone rushes to buy new puts

Tomorrow: all puts cashed out again after Williams sounds a bit dovish

— zerohedge (@zerohedge) May 5, 2022

Why Did The Market Just Break? Nomura Explains

BY TYLER DURDEN

FRIDAY, MAY 06, 2022 - 02:04 AM

Yesterday, while stocks were surging in the aftermath of the Powell presser during which the Fed chair took away the possibility of a 75bps rate hike, we joked that the bullish market reaction is precisely the opposite of what bulls - or Powell - want...

... as the easing in financial conditions (i.e., higher stocks) would undo almost all of the tightening from the incremental 50bps rate hike (first of many... or not many, now that the BOE confirmed that all developed central banks are hiking right into a recession). And just to make sure the market understood what was going on, we repeated it again this morning.

Which brings us to today's remarkable U-turn in stocks, and the complete reversal in stocks observed yesterday.

But first, a quick recap of what sparked the post-Fed rally, which as we explained yesterday was nothing more than the latest giant gamma squeeze, an observation confirmed this morning by Nomura's Charlie McElligott who writes the following:

I believe the scenario which might have scared [Powell] the most would have been going so hard with the potential “50bps May / 75bps June / 75bps July” which would have gotten them to “Neutral-ish” by end of Summer and stuck sitting on their hands…but then, risk being caught in a situation where the MoM inflation data stays persistently higher while unemployment data makes new lows—which would then see the market “expect even more” again, off what was already a “75bps hikes prior” and risking an enormous “policy / communications error” hawkish-escalation “hard landing” accident

As this was clearly then perceived by a VERY front-footed “hawkish” market as “UNDER-delivering” on said expectations for a “hawkish messaging,” we then saw Stocks blow higher thereafter, thanks to a massive “Short Gamma” squeeze and the corroborated “Vanna sling-shot” feedback loop we have been discussing, as implied Vols were just clobbered with the “hawkish left-tail” then viewed as almost essentially “removed” from the scenario distribution going-forward.

Precisely what we said yesterday, but recall we also said the following: "while it is easy to turn optimistic here, a warning: the last thing the Fed wants is for its 50bps rate hike - the biggest in 22 years - to be viewed as a green light to more risk on. In fact, if we indeed see stocks surging in the next few days, we fully expect the next crew of Fed talking heads which will hit the mic as soon as Friday to warn that not only is a 75bps - and even as 100bps - rate hike on the table, but that an emergency, inter-meeting announcement is distinctly positive if algos ignore the Fed call at their own peril."

Which brings us to the even more important question of "where to from here" which prompted a witty rejoinder Charlie McElligott who writes today that "a client said something which struck me two days ago: “Bulls and Bears both want a rally.”

That, of course, corroborates with what we said yesterday and Nomura's feedback from many in the “impulse FCI tightening” bear-camp, who have been saying they wanted to fade a large post-Fed relief / mechanical rally.

To the Nomura strategist, this then means the best way to continue trading this environment is “Short Vol, Short Delta.”

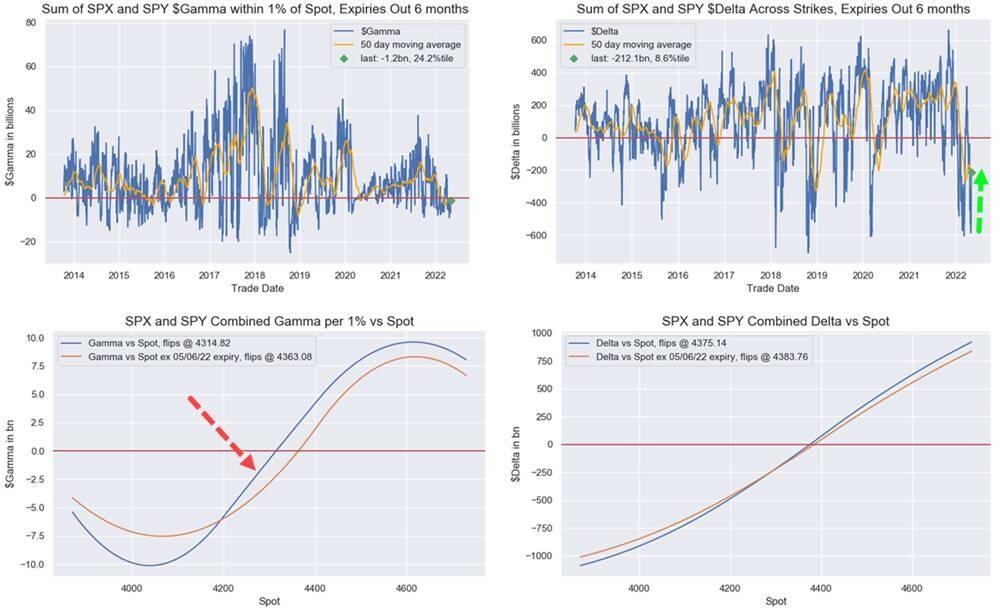

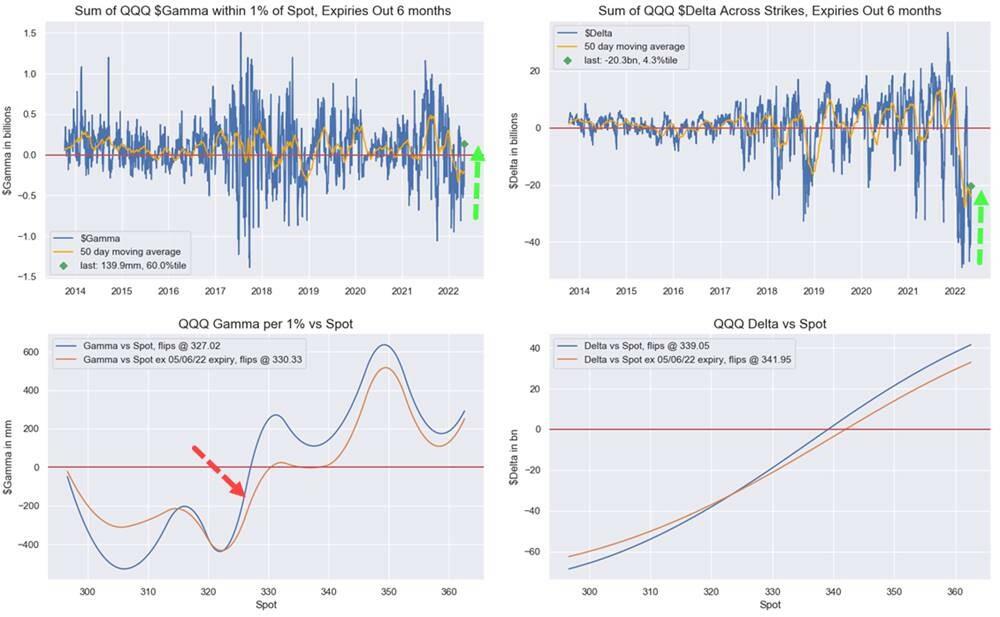

Practically, key levels for Bulls to reclaim from here are the “Zero Gamma” lines—where it truly feels that “THE” force which continues to drive the market are these “short Gamma” hedging pinch-points, where particularly SPX and QQQ are within reach—but still below—reclaiming this as a “stabilizing” force moving-forward:

- SPX / SPY $Gamma -$1.2B (jumping up to 24.2%ile now), “Zero Gamma” neutral line up at 4314 (currently nearing “Neutral Gamma vs Spot” but still “Short”

- QQQ $Gamma +$139.9mm (jumping up to 60.0%ile now), “Zero Gamma” neutral line up $327.02 (currently nearing “Neutral Gamma vs Spot” but still “Short”

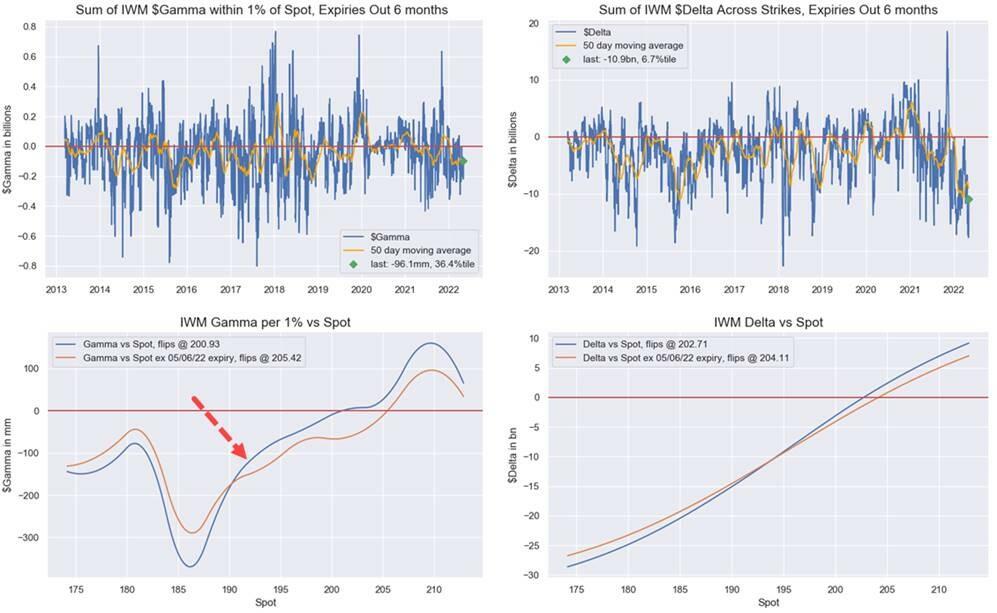

- IWM $Gamma -$96.1mm (jumping up to 36.4%ile now), “Zero Gamma” neutral line up at $200.93 (currently still VERY “Short Gamma vs Spot”

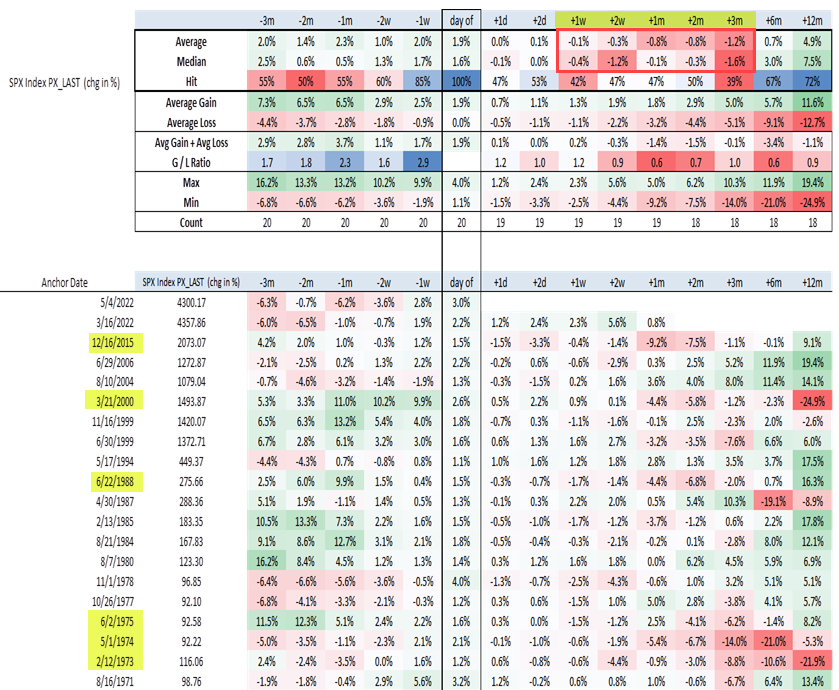

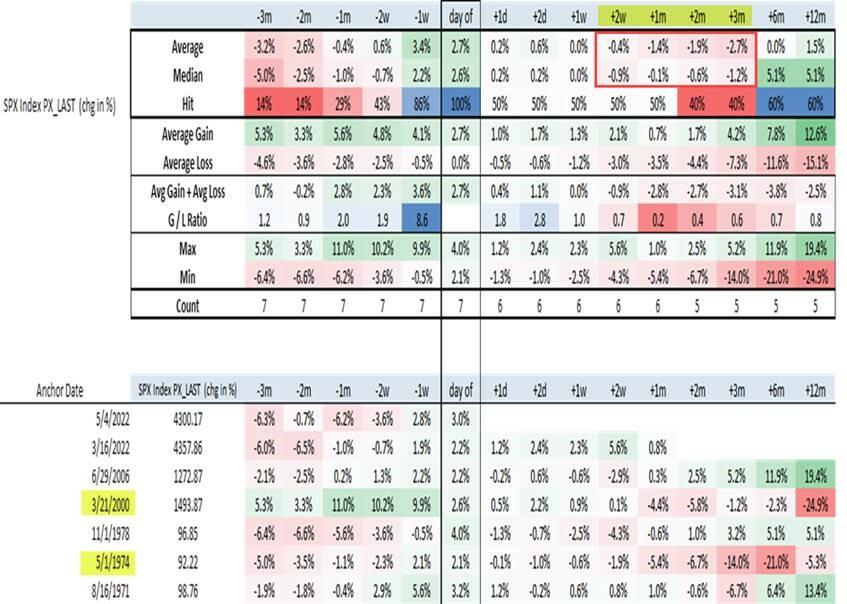

Charlie then looks at history to make an “analog” observation; specifically he took a look at days when the Fed hiked Rates and the SPX was up by more than either +1% or more than +2%. The read? Both show forward returns are locally “mixed at best” with a median SPX trade that is LOWER out 3m thereafter for both “triggers” (which is very rare for 3m windows in SPX tbh)…while revealing some especially “cringe” dates on the backtest:

1% moves on Fed hikes:

2% moves on Fed hikes:

McElligott concludes by noting that the Fed's “reset” of expectations to “buy time” for data to fit their view "feels risky to me — I mean, we are talking an attempt at threading the needle, but with a MOAB — as it risks both another “hawkish escalation” down the road which would almost certainly then see the market price “policy error / hard landing” bets even more aggressively, as the Fed would then be pushing into outright “restrictive” territory."

Of course, by extension if a market rally is the opposite of what bulls wanted yesterday, pushing into "outright restrictive" territory - i.e., accelerating the next recession - is just what the bulls need, as it means rate cuts and a fresh QE can't be far behind. In fact, today's crash is precisely what the bulls want...

...As I said the market is full of trickery and once again we...

Featured News

Featured News

The Watchlist

VMM

VIRIDIS MINING AND MINERALS LIMITED

Rafael Moreno, CEO

Rafael Moreno

CEO

SPONSORED BY The Market Online