..I have long cautioned about financials and now it appears that with US 10 year yields looking like peaking, financials are facing strong headwinds in the horizon as the credit cycle begins to turn.

...the XLF has corrected by 18% from its peak but remains 15% above its 2020 calendar year close.

Set to 5 year view

XLF Stock Fund Price and Chart — AMEX:XLF — TradingView

..but CBA has defied gravity.

CBA Stock Price and Chart — ASX:CBA — TradingView

Market participants rather wait for the event rather than undertake pre-emptive action. Psychologically that is easier to do than being ahead with conviction because of fear of doing the wrong thing (i.e selling). Obviously the market does not believe in a recession just yet, we have been told it is just noise and to ignore it...credit markets are still orderly. And of course we have yield seekers who would not trade a gem of a stock for worthless cash earning peanuts right? (and they can ignore capital movement in stock prices because they have a long term view).

Now set to All view on the CBA chart and you can't find any fault with it...too good to be true given the fast slowing world economy we are witnessing today?

Banks Face Trouble As Credit Cycle Turns

WEDNESDAY, MAY 25, 2022 - 09:25 AM

By Simon White, Bloomberg Markets Live Commentator and Analyst

Weak stock markets and worsening growth data - today’s miss in the flash PMI is case in point - did not deter Jamie Dimon from making positive comments on credit and the US economy at the WEF summit in Davos yesterday. Banks jumped on his remarks, but they face an increasingly challenging environment as the credit cycle turns and growth slows.

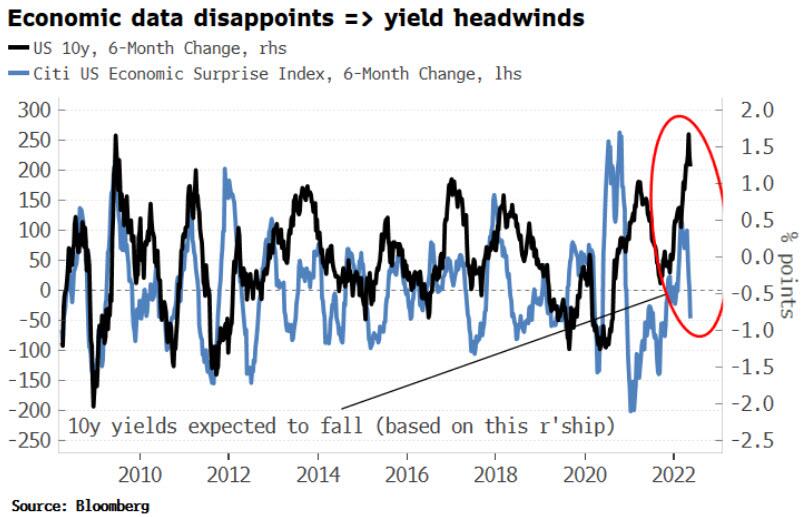

Bank outperformance is more closely linked to longer-term yields than the yield curve, and as a sector it is the most sensitive to changes in yields.

But bonds are already oversold, and as economic data starts to disappoint (today’s disappointing flash PMI is case in point), yields face greater resistance. Moreover, the only seasonally positive months for yields -- January to April -- are now behind us, with yields on average falling in the latter two-thirds of the year.

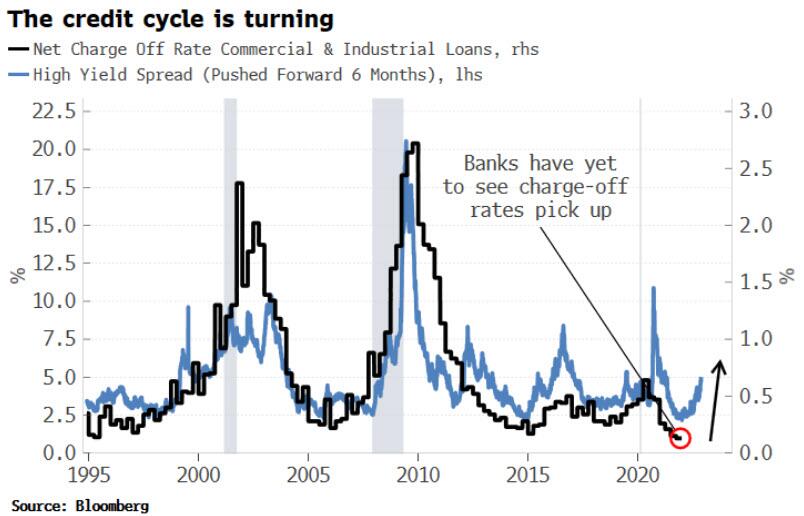

Everything in macro operates with lags of varying lengths, and the rise in yields has fed into credit through a fall in loan demand and tighter lending conditions.

The credit cycle itself operates in a well-defined sequence: first lending conditions tighten, the loan demand falls, followed by a fall in loan supply. Loan delinquencies then rise as more loans go bad, followed by a rise in charge-off rates as losses are realized. Finally, bankruptcies rise as loan losses lead to insolvencies.

The tightening of lending conditions today is captured by the steady widening of credit spreads, signalling the credit cycle is turning.The rise in charge-off rates typically follows wider credit spreads by six months.

Banks can pre-empt losses by increasing their loan-loss provisions. They did this at the beginning of the pandemic, but they turned out to be way more pessimistic than necessary, given the depth and breadth of fiscal and monetary support given to the economy. However, the loan-loss provisions of US banks are now negative, meaning there is currently zero absorbency for approaching loan losses. Banks were over-prepared in 2020, and they are under-prepared now.

It’s possible of course the growth scare is a storm in a teacup, and that credit spreads will soon tighten again. But that is not the way to bet, with a swathe of leading indicators from manufacturing new orders to heavy truck sales all pointing in the direction of an acceleration in growth’s decline in the coming months.

Inflation won’t help banks either. Elevated and persistent inflation typically leads to the real value of bank assets heading to zero faster than the real value of liabilities. Financials were in the bottom third of performers of sectors and asset classes through the four inflationary regimes experienced since the 1970s.

There are times when the macro stars align, pointing to a great trade set-up, but this is not one of them, despite what a bank CEO may say.

..I have long cautioned about financials and now it appears that...

-

- There are more pages in this discussion • 11,519 more messages in this thread...

You’re viewing a single post only. To view the entire thread just sign in or Join Now (FREE)

Featured News

Featured News

The Watchlist

NUZ

NEURIZON THERAPEUTICS LIMITED

Michael Thurn, CEO & MD

Michael Thurn

CEO & MD

Previous Video

Next Video

SPONSORED BY The Market Online