....I've said before about dividends, if not careful it is like taking from one pocket to another. Telstra long term shareholders can tell you but still contend getting their dividends despite long term erosion in their capital.

....now this must sink into BHP holders.

...in fact dividend focused holders probably never cared about being spooked to exit at the heights. Because time and time again, it has proven that prices will return. Except that if they knew how to take advantage of the cyclicality, they would be immensely much better off. If you must know, BHP price at $40 is now at the same level it traded in May 2008 peak , 14 years ago! Of course, they had their dividends and other special payouts. But if this is the cyclical peak that I am calling, it is down from here and will likely take multiple years before reaching this level again. And so holders likely have to choose Capital or Dividends. In all likelihood, they do nothing and that means Dividends. Dividend cuts are coming for the ASX’s richest miners Emma RapaportMarkets Reporter

Jul 1, 2022 – 4.13pm

Investors are “sleepwalking into dividend cuts” unless they strategically pivot away from iron ore dividends, which could fall by up to 40 per cent, and into the safety of industrials, an investment manager has warned.

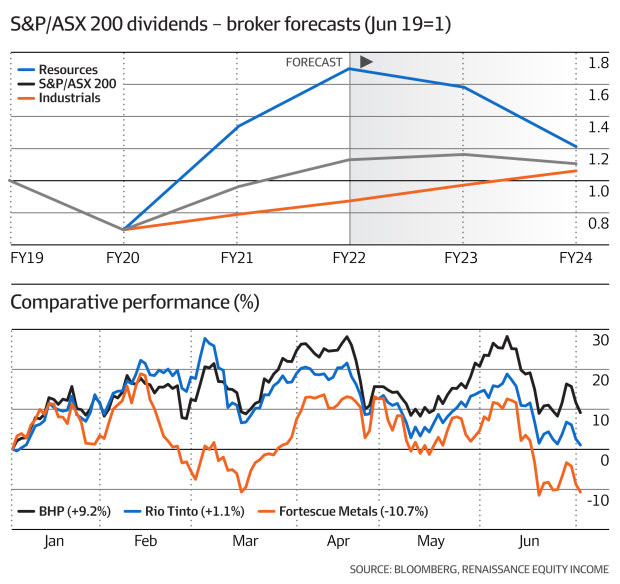

Tom Young, portfolio manager at Renaissance Equity Income, sounded the alarm, pointing to sell-side analyst forecasts that put dividends from large-cap favourites BHP Group, Rio Tinto and Fortescue Metals on a downward trajectory over the next two years.

“Mining dividends have basically been the only thing going up from an income perspective for retirees for the last five years,” he said, citing profit margins that "would make Louis Vuitton blush".

“[But they’ve] grown so far and so fast that they now represent a material risk to market dividends."

“It’s easy to forget just how volatile mining dividends can be,” Tom Young says.

Mr Young estimates dividends from the big three miners now make up 34 per cent of ASX 200 payouts.

Iron ore miners face a combination of unique risks that mean dividend cuts are likely, Mr Young said. First, the Chinese property market, which is a key demand driver on account of its steel usage, has slumped amid a developer debt crisis and weak buyer sentiment.

Second, he argued that fiscal stimulus is not making its way into the Chinese economy, risking gross domestic product targets and putting Australian iron ore exports under “increasing risk”.

“China is the bulk of the seaborne iron ore market and no one can step in and take the volume they’re taking,” he said.

But rather than a forecasting major downturn, Mr Young describes current events as a “normalisation of iron ore prices” which peaked at $US237 a tonne in May 2021 and have fallen back to $US120.90 a tonne.

“Now is a good time to reassess dividends from this sector to avoid being caught behind the curve.”

“Retirees who have come to rely on dividends from mining and energy stocks over the last six years may be sleepwalking into dividend cuts unless they reconsider their reliance on iron ore dividends,” he said.

Mr Young’s warning comes after a multi-year boom in iron ore dividends. Rio Tinto delivered dividends worth $US16.8 billion to shareholders, including two special dividends, over the past 12 months. BHP returned $US17.7 billion while Fortescue Metals paid out $6.6 billion. Meanwhile, bank dividends were slashed during the early stages of the pandemic to preserve capital.

But share prices have come under pressure this year alongside the pullback in the iron ore price. BHP fell 7.5 per cent in June, Rio Tinto 10.3 per cent while Fortescue gave back 12.8 per cent.

Mr Young suggested income-hungry investors seek a diversified bucket of dividend payers, describing bank, healthcare and supermarket dividends as “the inflation hedge retirees need” with consumer prices set to hit 7 per cent by the end of the year.

He expects the big four banks to be beneficiaries of the higher interest rate environment, sanctioned to earn more interest from borrowers than the cost of funding deposits. He downplayed credit risk fears, arguing expanding margins will offset bad debts in “all but the most extreme house price scenarios”.

“I think we’re headed into a discretionary income squeeze rather than a credit crisis.”

The fund manager estimates that just 12 per cent of non-resource dividends come from sectors exposed to inflation, namely consumer discretionary and building material stocks.

“Everyone is worried about industrial dividends if we enter a recession, but I think everyone is looking in the wrong spot,” he said.

“I think industrial dividends actually look alright. They were rebased during COVID and never fully recovered, balance sheets have been fixed, cash flows are strong, payout ratios are lower than they used to be and in aggregate industrial dividends are lower than they were five years ago, so there’s a lot of buffer built into these dividends to handle inflation.”

Indexing woes

For investors hoping a passive strategy will see them through the market volatility, Mr Young warned this approach contains “unnecessary concentration risk”.

Similarly, exchange-traded funds promising to seek out high dividends present risks because stocks historically have the highest dividend yields right before they cut dividends, he said.

“Dividends reflect what’s happened in the last 12 months, whereas the market looks forward 12 months,” Mr Young said.

“So if you’re buying stocks purely on the dividend yield, and the highest dividend possible, you’re buying every single stock that’s going to cut its dividend, and then you end up burning a lot of performance.”