Look, if we know anything right now, it's that inflation is running hot and interest rates are going up. However, as Padowitz explained, historically, when economies are slowing down, investors could cling to the prospect of interest rates heading south too.

"But because of a confluence of events - COVID-19, record levels of fiscal stimulus, and monetary expansion with zero or negative interest rates in some cases, as well as supply chain issues - inflation went from what was thought by some to be transitory to now entrenched and embedded," he said.

"That environment of higher interest rates into a lower economic environment doesn't happen often. It's only happened four times in the last 50 odd years... And all of those times have tended to be pretty poor for equity markets, as you would expect."

The first market impact has been the steep decline in the share prices of long-duration companies, as investors turned to companies that could deliver profits in the short term. The next, according to Padowitz, is a fall in corporate earnings.

"There's always going to be a lag. And when one looks at the historical context of margins, of how much companies earn relative to labour, it's at extreme highs. So there's quite a long way to go where earnings can fall," he said.

How much could earnings fall? Well, Padowitz believes it could be in the 20-30% range, and grimly, even up to 40%.

"We think we're heading into an earnings recession, or even potentially worse than that," he said. How to know when to pivot

According to Talaria analyst Max Welby, there are two signals that investors can use to get a better idea of when the market may have reached its low point.

"Since 1950, if you look at S&P 500, one or both of two things have really signalled the bottom of the market," he explained.

"That has either been a change in central bank policy towards a more supportive approach. And the second thing is a bottoming of the economy, particularly a bottoming of leading economic indicators."

He pointed to the ISM manufacturing index (or the purchasing managers' index PMI) as a key indicator for the Talaria team, one which typically lags interest rates by around 18 months.

"So right now, that is telling us that not only are we a long way off from a change in central bank policy, but we also think we are a long way off from the economy bottoming as well," Welby said.

"Now, what that doesn't mean is that you can't get very sharp recoveries in the market. If you look at bear markets over time, bear market rallies are the norm, not an oddity. What that supplies you with is an opportunity to (rebalance investments)." (see below)

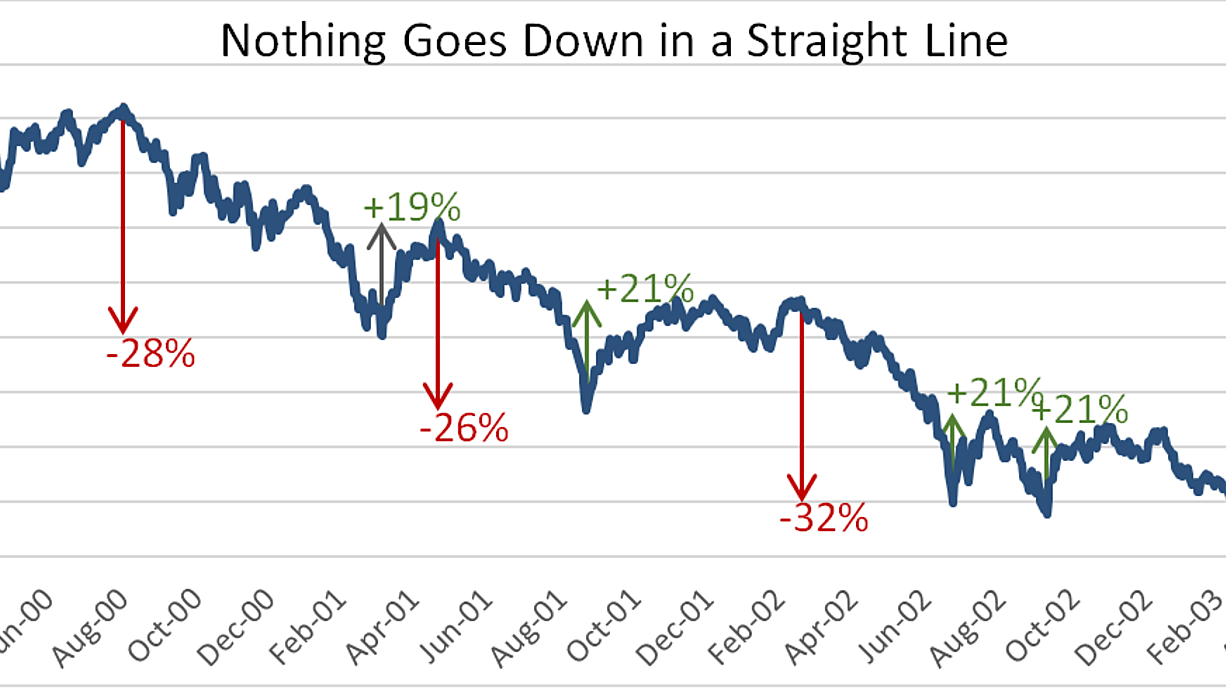

The S&P 500 during the tech bust. (Source: Talaria)

So how should you be positioned? Welby believes investors should be owning assets that are:

Low-beta (so avoid investments that track the market, like exchange-traded funds)

Short-duration (companies reporting profits now)

Low-volatility (companies with share price rises that are boring but beautiful/consistent)

"We want to buy the best company that valuation would afford, not the best company, period," Padowitz added. A final note

While Padowitz agrees that, yes, the market has dropped, and yes, investors may be tempted to dive on in, he is adamant about one thing:

"Price is a liar"

"When you actually look at the individual stocks, there was a lot more value on offer in the February and March period of 2020, during the COVID crash," he said.

"I think the mistake you can make is looking at where prices have dropped and assume that they must be great opportunities... It is very, very difficult to have complete confidence in where share prices are going to go.

So what can you do?

"Do the best you can to make sure that you've got the least amount of big problems if you're wrong," Padowitz said.

"And have the greatest proportion of things that will be on your side - like valuation, business fundamentals, and balance sheets."