...unless and until the Fed pivots, the US Dollar would continue strengthening and that does not bode well for commodities, tech (major MNC techs have large foreign earnings which translates into lower dollar proceeds)...which means the markets (both US and Aust) are unlikely to go anywhere higher in the short term. Leaving them susceptible to downside risks attributable to risk factors that have been well articulated across several posts in this thread.

This Could Be the Start of a Dollar ‘Doom Loop’ Like No Other

A reverse currency war beckons

By

Tracy Alloway and

Joe Weisenthal

July 18, 2022 at 6:00 AM GMT+10

The dollar’s gain is the world’s pain — and based on its current trajectory, the world may be in for a whole lot more discomfort.

Concerns over global growth have recently sent the Bloomberg Dollar Index to the strongest level on record, with the greenback hitting multi-decade highs against currencies like the euro and the yen.

But the move risks becoming a self-reinforcing feedback loop given that the vast majority of cross-border trade is still denominated in dollars, and a stronger US currency has historically translated into a broad hit to the world economy.

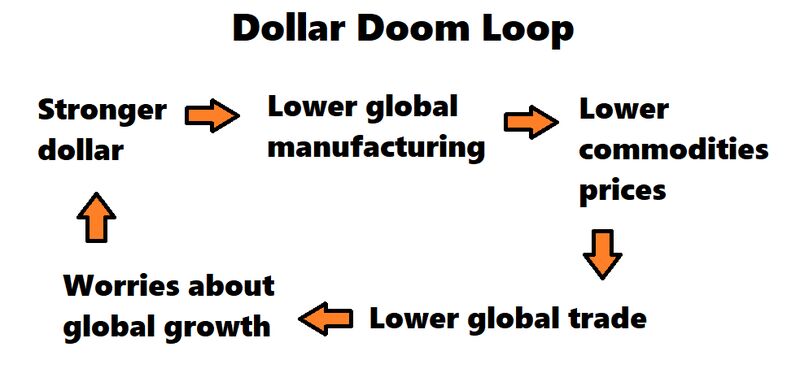

Against the backdrop of higher-than-expected inflation and still-elevated commodities prices, the concern is that we’re in for a dollar ‘doom loop’ like never before, according to Jon Turek, the founder of JST Advisors and author of the Cheap Convexity blog.

With the Federal Reserve hiking interest rates at the fastest pace in decades, he says, it’s much less clear what could break the feedback loop in the next few months.

“What makes this version of the doom loop really scary is it’s kind of hard to see how those circuit breakers play out over the near term,” Turek says in a new episode of the Odd Lots podcast. “We have a European problem, which creates pressure on the euro, which sends the dollar higher, which worsens the manufacturing cycle, which does this whole thing again. But is the Fed going to pivot with spot inflation at an eight handle?”

Of course, there have been periods of notable dollar strength before — such as in 2016 or 2018. Back then, the currency gained as the Fed sought to tighten policy and stopped once the central bank stayed its hand. With data released last week showing US CPI surging 9.1% year-on-year in June, the Fed has much less wiggle room to reverse course.

So the key question is to what extent the stronger dollar reduces the Fed’s inclination to go even bigger on interest-rate hikes in the coming months — in turn potentially providing some relief to exporters and leveraged borrowers around the world?

“It’s a little hard to see what kind of stops this. And I guess the best answer is that it could stop itself,” Turek says. “Something to start to think about — especially past September FOMC and really into the end of the year — depending on how bad the growth conditions are, especially in Europe, is: Will the Fed sort of be able to do this implicit handoff from interest rates to global economic conditions?”

When it comes to the dollar loop, there are many transmission channels. Researchers such as the International Monetary Fund’s Gita Gopinath and the Bank for International Settlements’ Hyun Song Shin, for instance, have shown that the dollar’s role in global trade means that a stronger US currency can lead to a tightening of global financial conditions and a hit to real investment.

The US currency also has a special position in world markets. When investors are worried, they tend to rush to the safety of dollar-denominated assets, sending the currency even higher. That’s one reason why the dollar surged when markets crashed in March of 2020, and why it’s been strengthening now.

Complicating the current situation is the fact that major central banks around the world are now in tightening mode, or about to be. The European Central Bank is expected to begin hiking rates this month for the first time since 2011. Germany, in particular, faces a double economic whammy as soaring natural gas prices also cut into its manufacturing sector.

“We’re in a world now where central banks who are all dealing with above target inflation have very little tolerance for massive currency weakness because it’s thought to only amplify the pressures that they’re dealing with by hiking rates,” Turek says. “We are in this sort of reverse currency war, but I think that central banks are clearly making an emphasis on the role of currencies, some more explicit than others, of course … Given the nature of the shock, it does make sense for central banks to have a very big, you know, overarching currency focus.”

That may be one reason why Switzerland’s central bank surprised the market with a 50 basis point rate rise in June, its first hike in 15 years. Even though the Swiss franc has been relatively strong, Turek argues, “it hasn’t been strong enough in real terms to kind of offset some of the above target inflation that even they’re seeing.” Meanwhile, at the Bank of England, Catherine Mann noted in a speech earlier this month that “tighter US monetary policy tends to boost UK inflation because of the weaker pound.”The wild card could be China, Turek says. Credit in the country jumped in June after the government unleashed stimulus aimed at offsetting the effects of rolling Covid-19 lockdowns. But even with the stimulus, it’s tough for new loans and other types of monetary easing to transmit to the real economy given ongoing pandemic restrictions.

Source: Turek/Bloomberg

Recent dollar strength is at odds with predictions made earlier this year that the invasion of Ukraine and subsequent sanctions could mark a turning point for the US dollar. On the other hand, the timeframe for reducing the dollar’s role as the world’s reserve currency was never expected to be a quick one, and a painfully soaring greenback could ultimately still encourage countries to seek alternatives.

And in the US, the dollar doom loop could end up doing some of the Fed’s work for it when it comes to fighting inflation.

“What makes this version of the doom loop so challenging is that it is a condition or an externality that the Fed, in its efforts to lower inflation and lower inflation quickly, is actually accentuating what I think is almost, in their view, positive,” Turek says. “The question that market participants should begin to ask is if the dollar is doing all this work, you know, does the Fed have to go to 4.5% or something like that? I think that is an interesting question on its own, but in terms of what arrests this current dynamic, it’s really tricky.”

Its Over, page-13715

Featured News

Featured News

The Watchlist

ACW

ACTINOGEN MEDICAL LIMITED

Dr. Steven Gourlay, CEO

Dr. Steven Gourlay

CEO

Previous Video

Next Video

SPONSORED BY The Market Online