Jamie Dimon’s S&P 500 Bear Market: Brutal, Far From Unimaginable

By

- A clash with JPMorgan forecasters highlights a chaotic 2022

- Market unwind has further to go given decades of easy money

Lu Wang and

Peyton Forte

October 12, 2022 at 1:26 AM GMT+11

Jamie Dimon says don’t be surprised if the S&P 500 loses another one-fifth of its value. While such a plunge would fray trader nerves and stress retirement accounts, history shows it wouldn’t require any major departures from past precedents to occur.

Judged by valuation and its impact on long-term returns, the JPMorgan Chase chief executive officer’s “easy 20%” tumble, mentioned in a CNBC interview yesterday, would result in a bear market that is in many regards normal. A decline roughly to 2,900 on the S&P 500 would leave the gauge 39% below its January high, a notable collapse but one that pales next to both the dot-com crash and global financial crisis.

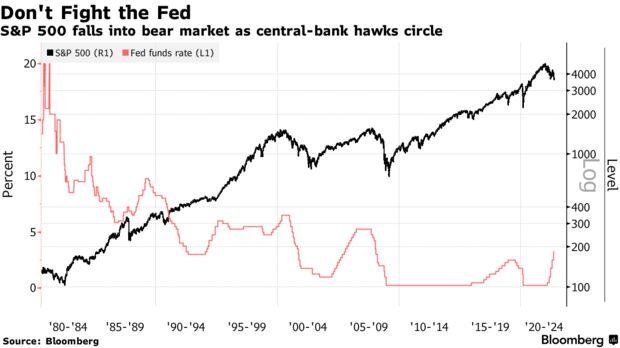

The price implied in Dimon’s scenario is roughly the index’s peak from 2018, the year when President Donald Trump’s corporate tax cuts took effect and an equity selloff forced the Federal Reserve to end rate hikes. Rolling back the gains since then would leave investors with nothing over four years, a relatively long fallow period. But, given the force of the bull market that raged before then, it would cut annualized gains over the past decade only to about 7%, in line with the long-term average.

Nobody knows where the market is going, Dimon included, and much will depend on the evolution of Federal Reserve policy and whether earnings stand up to its anti-inflationary measures. As an exercise, though, it’s worth noticing that a drawdown of the scope he described isn’t unheard-of, and would strike many Wall Street veterans as a justifiable reckoning in a market that had been carried aloft by the Fed’s generosity.

Falling interest rates had “been great for valuation multiples and we’re unwinding all of those,” Michael Kelly, global head of multi-asset at Pinebridge Investments LLC, said on Bloomberg TV. “We’ve had easy money for a long time and we can’t fix all of that very quickly.”

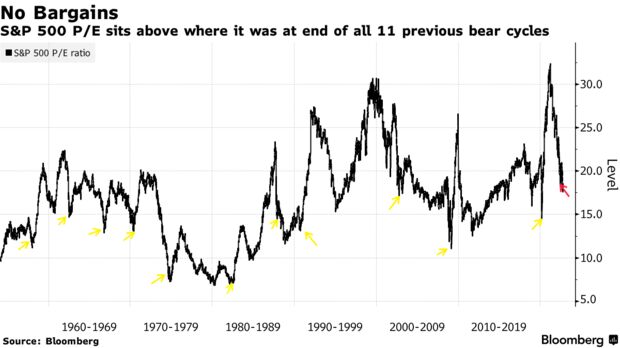

At 34%, the average bear market since World War II has been a bit shallower, but the drops vary enough that a 40% plunge fits within the bounds of plausibility. One reason the current drawdown may have legs is valuation. In short, even after losing $15 trillion of their value, stocks are far from being obvious bargains.

At the low last month, the S&P 500 was trading at 18 times earnings, a multiple that is above trough valuations seen in all previous 11 bear cycles, data compiled by Bloomberg show. In other words, should equities recover from here, this bear market bottom will have been the most expensive since the 1950s. On the other hand, matching that median would require another 25% drop in the index.

“We had a period of a lot of liquidity. That’s different now,” said Willie Delwiche, an investment strategist at All Star Charts. “Given what bond yields are doing, I don’t think you can say a 40% peak-to-trough decline is out of the question.”

Would the S&P 500 become a bargain if a 20% drop played out? It’s debatable. While 2,900 is quite cheap relative to existing estimates for 2023 earnings -- about $238 a share, implying a P/E ratio of 12.2 -- those estimates would be in serious trouble should a recession occur, as Dimon predicted. Adjusting forecasts for a 10% fall in profits yields an earnings multiple of 14.3 -- not expensive, but not a screaming bargain, either.

Underlining Dimon’s gloomy outlook is the threat of an economic contraction. From surging inflation to the Fed’s ending quantitative easing and Russia’s war in Ukraine, a number of “serious” headwinds are likely to push the US economy into a recession in six to nine months, the JPMorgan CEO told CNBC.

Dimon’s assessment on the economy and market appears more ominous than his own in-house forecasters. Michael Feroli, JPMorgan’s chief US economist, expects real gross domestic product to expand every quarter through the end of 2023.

While market strategists led by Marko Kolanovic admitted their year-end targets for financial assets may not be reached until next year, the team kept their upbeat tone on corporate earnings. It had expected the S&P 500 to rally to 4,800 by December.

“Equities are proving to be an effective real asset class as their earnings are linked to inflation,” the team wrote in a note last week. “Unless nominal GDP growth downshifts drastically, earnings growth should remain resilient and defy expectations of a decline even in an environment of low real GDP growth.”

Its Over, page-14876

-

- There are more pages in this discussion • 7,782 more messages in this thread...

You’re viewing a single post only. To view the entire thread just sign in or Join Now (FREE)