Mark B. Spiegel of Stanphyl Capital :

Mark’s Thoughts On Macro

Despite the stock market’s recent rally (we were up a hell of a lot more this month before today!) we continue to carry a large SPY short position, as I believe the major indexes—although not all individual stocks—have considerably more downside to go, the inevitable hangover from the biggest asset bubble in U.S. history.

For far too long, the Fed printed $120 billion a month and held short-term rates at zero while the government concurrently ran a record fiscal deficit. Now, thanks to the massive inflationary hangover from those idiotic policies (November’s “not as bad as feared” data not withstanding), the Fed is reducing its balance sheet and raising interest rates, and although the current rate of high-7% year over-year inflation is unsustainable, the eventual end of China’s “zero-Covid policy” and its November reversal on bailing out its real estate industry combined with the end of Biden’s SPR drawdowns will give commodity prices a brand new tailwind in 2023.

Longer term, the war on fossil fuel, expensive “onshoring,” fewer available workers and perpetual government budget deficits make a new baseline of around 4% inflation (double the Fed’s 2% target) likely.

Even a 2023 Fed interest rate “pause” at 4.75% (and remember, a “pause” is not a “pivot”!) would, combined with $90 billion a month in ongoing QT, make current stock market valuations unsustainable, as stocks are still expensive.

[QTR’s note: This echos Kenny Polcari’s sentiments & my sentiments of recent.]

According to Standard & Poor’s, with 97% of companies having reported, Q3 S&P 500 GAAP earnings came in at around $44.79, which annualizes to $179.16. (And these were the sixth highest quarterly earnings in history; i.e., they were not “trough.”

A 16x multiple on that—generous for a rising rate, recessionary (or even just slow-growth) environment—would bring the S&P 500 down to 2867 vs. November’s close of 4080.11. And remember, just as in bull markets, PE multiples usually overshoot to the upside, in bear markets they often overshoot to the downside. A bottom formed at a considerably lower multiple is not unfathomable.

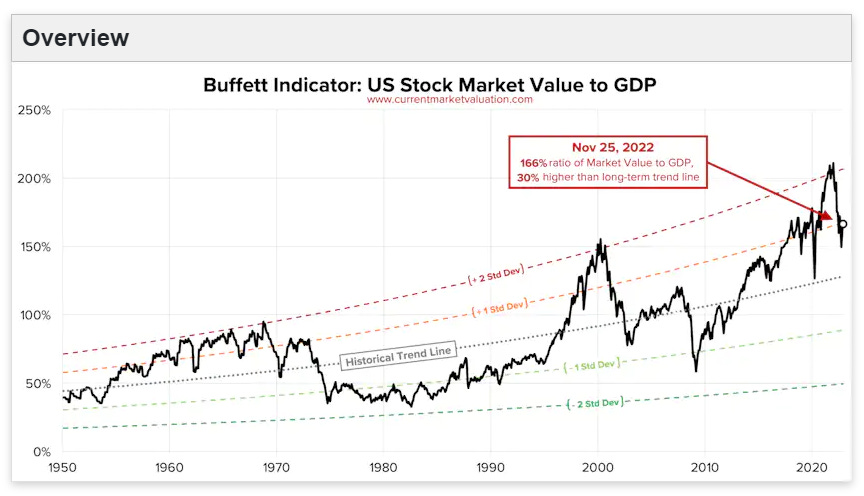

Additionally, we can see from CurrentMarketValuation.com that the U.S. stock market’s valuation as a percentage of GDP (the so-called “Buffett Indicator”is still very high, and thus valuations have a long way to go before reaching “normalcy”:

Regarding sentiment, we can see from Ed Yardeni that in the Investors Intelligence poll the highest the “bear percentage” got so far in the current market was only around 45% (in the most recent poll it was just 31.5%), yet there were multiple times during the 1980s, 1990s and 2008 that it climbed much higher:

Also, we can see from this old academic paper that during the grinding bear market of 1973 to 1975, when the S&P 500’s GAAP PE multiple dropped from 18x to 8x, the bears in the Investors Intelligence poll climbed to around 75% and went over 80% during the bear markets of the 1960s.

So if you think that based on this bear market’s sentiment we’ve “seen the bottom,” I wish you luck!

Mark B. Spiegel of Stanphyl Capital : Mark’s Thoughts On Macro...

-

- There are more pages in this discussion • 6,858 more messages in this thread...

You’re viewing a single post only. To view the entire thread just sign in or Join Now (FREE)