....what Buy and Hold for longer of these large resource behemoths look like

....in 13 years, BHP almost doubled, so using Rule of 72, if you double your money in 13 years, the annual return = 72/13= 5.5% which is rather paltry. And could be worse if bought at the peak. If you read my earlier post on Australia's low grade iron ore up against higher grades from Brazil and Simandou (Guinea), there's also good reason to be nervous.....not to mention too a huge class action lawsuit from UK about to hit BHP like a sledgehammer sometime soon this year.

BHP (ASX: BHP) faces $65 billion damages claim over Brazil mine disaster (smh.com.au)

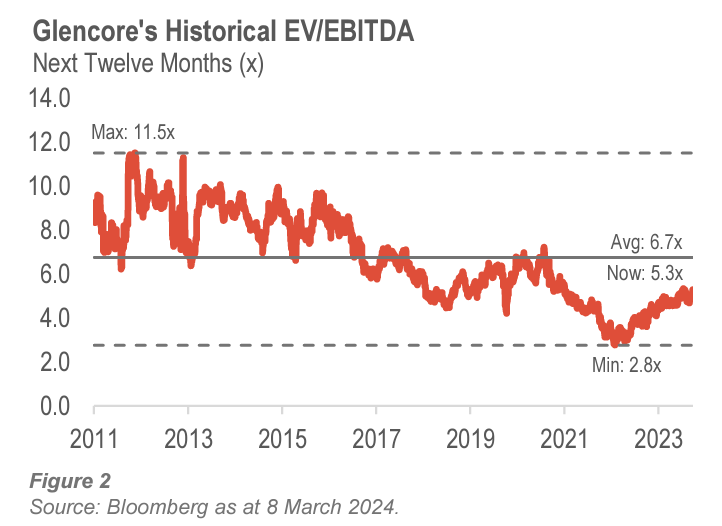

Despite its core asset quality and strong fiscal position, Glencore’s share price has underperformed its peers (see figure 1).

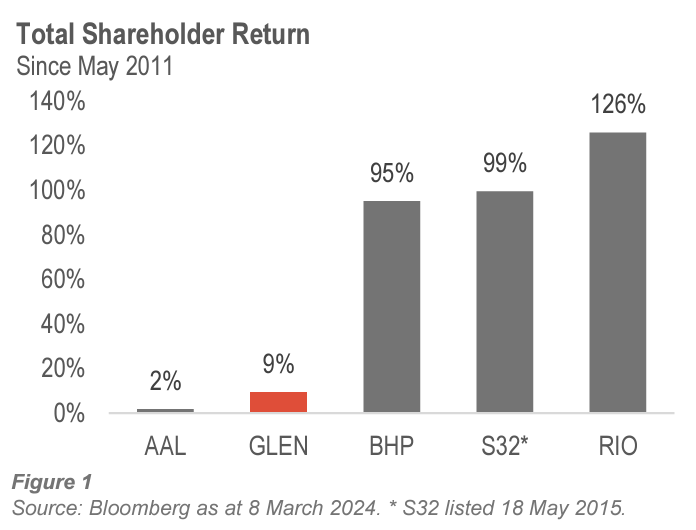

Since listing on the London Stock Exchange (LSE) in May 2011, the total return Glencore has provided to shareholders, including buybacks and dividends, has been 9%. Over the same period, returns delivered by peers such as BHP (+95%), South32 (+99%) and Rio Tinto (+126%) have been multiple times higher. This disparity is a result of continued de-rating (see figure 2) illustrated by the fact that, despite having quadrupled EBITDA, Glencore’s enterprise value has risen by only 15% pursuant to its initial public offering (IPO).

....what Buy and Hold for longer of these large resource...

-

- There are more pages in this discussion • 2,913 more messages in this thread...

You’re viewing a single post only. To view the entire thread just sign in or Join Now (FREE)

Featured News

Featured News

The Watchlist

LPM

LITHIUM PLUS MINERALS LTD.

Simon Kidston, Non--Executive Director

Simon Kidston

Non--Executive Director

SPONSORED BY The Market Online