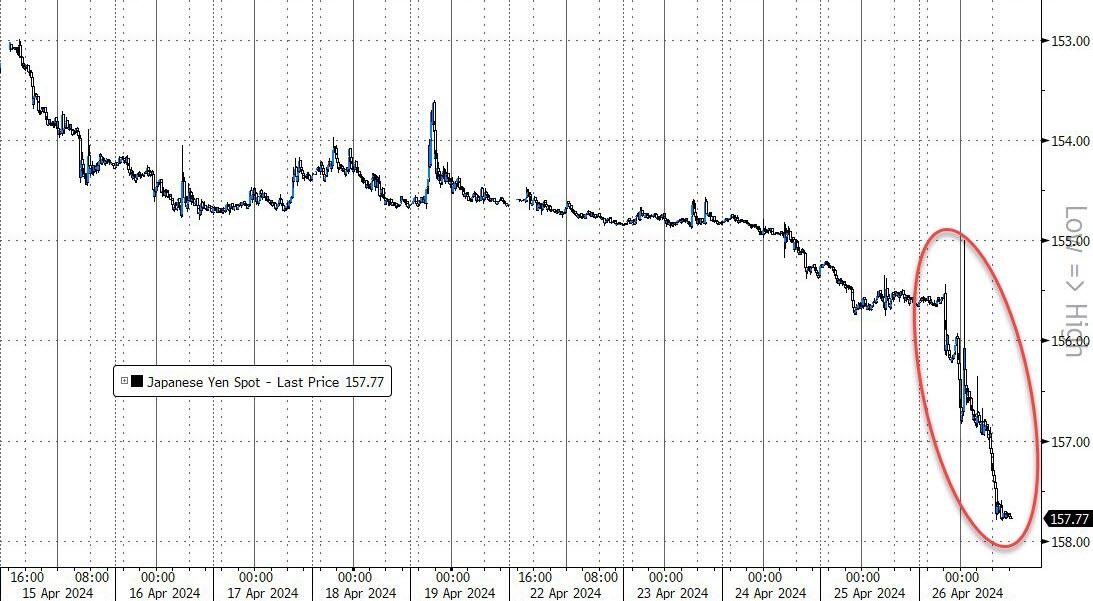

...the Yen collapse last night to 158.35 was the biggest overnight development.

...BoJ's biggest fear is unfolding

...despite the seventh straight week of declines in the yen vs the dollar as it appears the BoJ and MoF have given up... Source: Bloomberg

by Kurts Altrichter

Why You Should Care About the Yen Carry Trade

The crash in $JPY has been going on for well over a year. The cause? The massive interest rate gap: Japanese bonds at ~1% vs. U.S. Treasuries at ~4.25%. This disparity has been pulling investors away from the yen in search of higher yields

While the Fed, ECB, and Bank of England have hiked rates to levels unseen in decades, the Bank of Japan has held rates close to 0% for the last 17 years. This difference has forced global investors to sell the yen and buy the higher-yielding dollar, pound, and euro.

Enter the "yen carry trade": A strategy for low-risk returns: investors borrow cheap yen to invest in higher-yielding fixed income around the globe. This dynamic is lucrative until the yen strengthens, making it a critical point for investors to watch.

Here's how it works: Hedge Funds, family offices, and some HNW investors will borrow the yen at around 1% (they do this by selling Jap gov bonds short) and buy Treasury bonds (or other fixed income like EM debt or junk bonds) and between 4%-10%ish yields, thereby making a leveraged interest rate spread. Again, this works very well until the yen strengthens, and that's why this matters

In response to the yen reaching a 34-year low, Japanese authorities have recently warned against this type of speculative trading, which is code for saying they are willing to purchase trillions of yen to prop up the currency if the sell-off continues. A rapid rise in the yen will unravel carry trades, causing widespread market volatility and that could be catastrophic.

This could be a huge problem. The short positions on JGBs are extremely high. If investors panic in response to the possibility of government intervention, they will unwind their carry trades and race to exit their positions, in turn causing massive volatility in uncorrelated markets: U.S. Treasuries, junk debt, emerging market debt, and equities.

While the US economy is chugging along with rates 500 bps above Japan's, there is not a lot of motivation for investors to allocate capital to Japanese risk assets. These traders have made a lot of money so far, and they will likely continue to bleed the currency dry for much longer than markets expect.

The BOJ is in a tough spot. The easiest way to save the yen would be to start closing the gap in interest rates, which means hiking rates even further. However, the Japanese economy has delivered negative economic growth in 4/10 quarters so they would be essentially hiking themselves into a recession or worse.

The question that the Bank of Japan has to answer is whether it wants to save its currency or save its economy. If the BOJ is forced to make this decision, then we have a currency crisis either way.