...healthcare, defensive no more, plagued by high debts under soaring rates and escalating operating costs. Brookfield’s Healthscope debt trap is a mess for everyone involved

The investment giant is bringing its punchy approach to restructuring – and tactics more often found in the US – to Australia as it works on the hospital group. Jemima WhyteSenior reporter

May 12, 2024 – 5.38pm

The owners of Healthscope, the country’s second largest privately owned hospital group, don’t want to talk about negotiations with its lenders. Everyone else does.

It’s partly because Canadian giant Brookfield, which owns Victorian energy transmission group AusNet and building contractor Multiplex, is again ruffling stakeholders, just months after an aggressive but failed attempt to buy Origin Energy.

This time, it is their punchy approach to restructuring debt, bringing tactics that are more often found in the United States to Australia. Brookfield’s US managing director, Michael Rudnick, who specialises in “liability management” and restructuring, flew into Australia six weeks ago and the hospital operator’s lenders have been offside ever since.

Healthscope has a contract with the NSW government to run the public wing of Northern Beaches Hospital until 2038. Nick Moir

Detractors are quick to point out that how Brookfield handles the Healthscope restructure may spill into their ability to get financing for other deals in the local market.

Whether Brookfield is successful in convincing its group of 20-plus lenders – including the big four local banks, debt funds Challenger, Revolution and Metrics Credit Partners alongside international names – that they must cut a deal for its $1.6 billion debt isn’t clear. There are no signs that the banks are rolling over yet.

In fact, late last week the market chatter was the negotiations were at a stalemate.

The lenders were still baulking at Brookfield’s proposal to split Healthscope into two, and force the lenders to recut their terms. One option canvassed included rolling lenders into a BadCo, and only allowing those that agreed to participate in GoodCo and subsequent (and likely) debt issues.

Observers noted the ongoing stalemate signalled that maybe Brookfield, which declined to comment, was starting to consider other options.

Either way, the approach is reshaping the market. Lenders are telling issuers that these kinds of loopholes can’t be left open on new deals.

Brookfield’s move to restructure the assets security pool and potentially subordinate existing lenders – as they ask for more favourable terms – is more commonly used in Chapter 11 situations, which don’t occur here.

The proposed restructure had elements of controversial restructures including Chewy, J.Crew and Serta, and even GenesisCare, which did affect local lenders cut out quickly unless they agreed to help refinance the company as part of the Chapter 11 terms.

But however significant the issues are for Brookfield’s own reputation and lending syndicates in the local market, there are much bigger issues at play.

Restructuring Healthscope, which flagged in its own accounts that it may breach quarterly covenants if operating conditions deteriorate, will draw in private health insurers, the state and federal governments, and landlords North West and ASX-listed HMC Capital, which own the real estate for Healthscope’s 38 hospitals.

Brookfield is doing its best to create a “burning platform”, and a sense of urgency around the whole private hospital sector. Its attempt to restructure the debt is before any covenant breaches, although it flagged they may be coming in their filings with the Australian Securities and Investments Commission.

In regulatory filings, the company said while it would meet its March 31 quarterly covenants, “based on the group’s cash flow forecasts and earnings projections, and absent a recapitalisation or a modification of the terms of the facilities, the group is forecasting very limited covenant headroom with the possibility of a covenant breach during the financial forecast period”.

Moving early on the lenders may help ratchet up pressure on governments and health insurers, which are already in discussions about how to better share funding support.

The starting point is how to square out the private health insurers’ super profits during the pandemic when elective surgery collapsed and fewer claims were made, but private hospitals are hoping for more than that. And, of course, more funding from the private health insurers would help the private hospital system’s margins.

Brookfield doesn’t have to do a lot to remind everyone of the challenges facing the private hospital sector. Inflationary wage costs, a labour squeeze and doctors reducing hours following the pandemic are just some of the factors hurting the sector, which helps to keep pressure off the public hospital system.

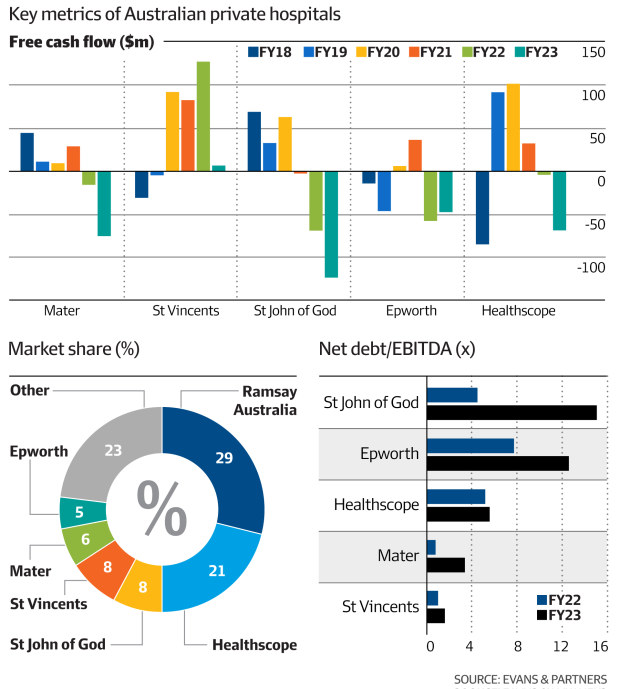

Evans & Partners analysts described the private hospital sectors as in “critical condition” and estimate all players – except Ramsay Health Care – are unprofitable at profit before tax.

It called out Healthscope, Mater and St John of God as under the most financial stress because of their high debt levels. Healthscope’s interest cost rose 18 per cent during the 2023 financial year. Of course, some of the pressures could reduce in time – labour shortages may ease, and wage pressure as well.

But strip it all back, and consider this as a private equity investment. Then the big – if longer term – question is: would Brookfield tip in more equity for one underperforming asset or choose to walk away? And if it walks, what does that mean for its reputation?

Immediately after the deal closed, Brookfield sold 22 properties in the Healthscope portfolio. North American investors NorthWest and Medical Properties Trust bought the properties for $2.5 billion, and Healthscope struck leases that have a weighted average expiry of 20 years and will incur fixed annual rent increases of 2.5 per cent per annum.

It was a textbook OpCo, PropCo move. ‘Cashflow lend’

Later, when the COVID-19 pandemic hit, and Healthscope’s revenue from elective surgeries was wiped out, Brookfield changed CEOs and restructured.

The lenders took what is often known as a “cashflow lend”. That is, they didn’t have security over the properties, which were owned by others. Instead, they were to be paid back from hospitals’ cash flows, which were considered largely predictable. Under the terms, debt can’t be traded while the borrower is in compliance with them.

So where does that leave everyone now? Simply, waiting.

One milestone for Healthscope – and the sector – will be the outcome of negotiations with the private health insurers and the government, which are now tipped to go to some form of government review into the sector. Another catalyst that could break the stalemate would be any covenant breaches, which would allow lenders to trade debt.

Until then, it’s about brinkmanship and who blinks first. Already, names for alternative operators for the private hospital group are being thrown up, including Wesfarmers, which is speculated to have cast an eye at Ramsay, and other private equity firms.