...few expected the GyG IPO to do as well as it did.

...difficult to find an explanation for the vibrant premium achieved over the premium IPO price, other than some say FOMO

....but any buyer could well do a little research to find that fast food companies are not doing well at all, DMP (Domino Pizza) already has a global footprint and languishing under a giant X-mas tree chart, while CKF (Collins Food which owns KFC) has gone nowhere the past 5 years on a PE of 34x.

....and with a chequered history of meeting targets/projections, GyG could struggle to operate under a listed environment where you can only expect a brutal selloff if those prospectus projections that have been juiced up is not met in the quarters ahead. Blaming on the economic environment won't work, it has been priced for perfection. Even Maccas had to resort to a $5 meal to address the cost of living issue its patrons face. I don't even think GyG has a loyal following just yet, unlike Maccas and Maccas already having it tough.

5 year view

DMP Stock Price and Chart — ASXMP — TradingView

CKF Stock Price and Chart — ASX:CKF — TradingView

Guzman y Gomez has a history of missing forecasts, documents show

Sarah Thompson, Kanika Sood and Emma Rapaport

Jun 20, 2024 – 5.55pm

It’s tiempo de fiesta for Guzman y Gomez’s investors after shares in the Mexican-themed restaurant chain shot up 36 per cent on Thursday. But can they trust its co-CEOs Steven Marks and Hilton Brett to deliver on the blockbuster IPO’s growth forecasts?

Documents presented by Guzman y Gomez’s largest shareholder, TDM Growth Partners, to its backers in 2018, and now obtained by Street Talk, show the restaurant chain missed every projection on key financial metrics for both FY22 and FY23.

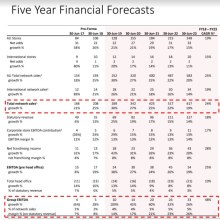

For starters, those documents suggest the company would have 248 stores in Australia – and another 20 overseas – by the end of June last year. In reality, it was 38 stores short of the target come IPO time – not a good look when you consider its lofty ambitions of serving burritos from 1000 locations in Australia within two decades.

More importantly, TDM and Guzman y Gomez forecast a base case EBIT of $31 million for FY23. That’s nearly eight-times – yes, that’s not a typo – higher than the actual pro forma EBIT of $3.7 million that earns a mention in the IPO prospectus.

In 2018, Guzman y Gomez forecast EBITDA of $26 million for FY22 and $33 million in FY23. The actual numbers were less appetising at $21.7 million and $29.3 million respectively. Guzman y Gomez expects to make $59.9 million in earnings in FY25.

Of course, IPO documents typically do not include management’s track record of forecasting for the business. Thankfully, the confidential investor presentation from 2018 should help fill in some of the gaps for over-zealous investors in the company.

The bottom line is this – Guzman y Gomez hasn’t been growing as fast, or is as profitable, as management had previously predicted.

We’ll sign off by bringing your attention back to valuation multiples. Back in 2018, when Guzman y Gomez was raising at a $125 million pre-money valuation, TDM reckoned it was hot to trot at a 13.2-times EV/EBITDA multiple. Fast-forward to 2024, and it’s defending a valuation of 32.6-times.

...few expected the GyG IPO to do as well as it did....

-

- There are more pages in this discussion • 1,287 more messages in this thread...

You’re viewing a single post only. To view the entire thread just sign in or Join Now (FREE)

Featured News

Featured News

The Watchlist

LPM

LITHIUM PLUS MINERALS LTD.

Simon Kidston, Non--Executive Director

Simon Kidston

Non--Executive Director

SPONSORED BY The Market Online