...today Donald Trump said he will bring inflation down except he did not say how.

...the only cue I got was that he would bring the price of gasoline down by 'drill, baby, drill' - that he can do by increasing supply of the black gold that the US has under its ground.

But his tariffs on China and EU would increase cost to US consumers, his tax cuts would fuel demand-led inflation, his onshoring of manufacturing would increase the cost of goods that American citizens buy...his America First policy would make businessmen wealthier but consumers poorer, increasing inequality (what do we boomers care, right?).

He can't change the hell-hole predicament that America is already in.

Are we naive enough to believe that a tariff imposition on China and EU won't see a corresponding repercussion on US trade?

It has been the premise that US exerts its superpower interventionist approach to defend the democratic world in order for its US dollar to be the international reserve currency that the world accepts. This is why US defends countries without asking them to pay as Trump does. Because it incentivises its allies and friends to lend to the US at affordable rates by buying their US Treasuries, so Americans can continue to spend with impunity. Biden has erred and allowed former US backers amongst emerging market countries to embrace the other side (Russia/China) and Trump's America First policy would only serve to further water down its hegemonic power, and eventually compromise its reserve currency status within 10 years.

Second subprime crisis more likely with Trump in the White House

Investors need to start preparing for how a re-elected Donald Trump will shape inflation, interest rates, and hence asset prices.

Christopher JoyeColumnist

Jul 19, 2024 – 3.42pm

With the US Federal Reserve desperately seeking to lower interest rates in September to bolster Joe Biden’s electoral prospects, one topic that has not commanded enough attention has been what a Trump presidency will mean for markets.

Helpfully, The Wall Street Journal has just released a survey of economists that reveals inflation and interest rates are likely to be higher for longer under a Trump regime.

This column has long posited that Trump’s core electoral platform of slashing immigration, imposing tariffs on Chinese imports and reducing taxes would boost wages, consumer prices and the size of the already gigantic US budget deficit.

The risk is that if Trump wins comprehensively in November, he may receive a mandate to implement even stronger iterations of these policies, which would, at the margin, further amplify inflation.

It beggars belief that the Fed would be falling over itself to hastily cut rates in September in the face of what could be a fairly dramatic regime change.

Why not exercise the option to wait, given it will garner profoundly new information in November apropos the expected trajectory of the economy?

Trump also has a radically different and more self-deterministic approach to geopolitics, which could materially lift the probability of China seeking to unify with Taiwan.

Precisely what this means for markets is an open question.

If Trump is keen to try to appropriate Taiwan’s competitive advantage in semiconductors, and allow the island state to be absorbed back into the mainland with minimal fuss, it might resemble a fairly stealthy event similar to what we saw play out with Hong Kong.

If, on the other hand, a bombastic Trump wants to engage in an existential battle with the Middle Kingdom on ideological lines, and zealously defend the Western liberal-democratic project from autocratic interference, we could be on the precipice of major power conflict.

Trump’s preternatural sensitivity to financial market movements, and his perverse fixation with the power wielded by despotic dictatorships, might argue in favour of the more benign contingency.

But in the end, nobody knows. What we do know is that the tails of the distribution of potential outcomes are going to get a lot fatter under an emboldened Trump administration.

Inflation more persistent

There are consequential corollaries from all of this. A key observation is that multi-asset-class portfolios and the financial system at large remain heavily influenced by the ultra-cheap money paradigm and the rampant search for yield that resulted from near-zero cash rates.

Since unemployment rates have generally risen only modestly, most economies have yet to experience the reckoning that would compel a painful reallocation of people and money from “bad” zombie businesses that predicated their future on the low-rates-for-long paradigm back towards “good” firms that can thrive in a climate of much higher cost of capital.

A Trumpian world characterised by even more persistent inflation pressures is likely to apply a harsher blow-torch to the fragile perimeter of the economy. As this column has explained previously, we are already seeing many signs of these problems emerging for cyclically sensitive borrowers, with the highest business insolvencies in Australia in more than 25 years and the second-worst default cycle in risky high-yield, or sub-investment grade, bonds since the 2008 crisis.

Only last week, PIMCO warned that 40 per cent of all private credit borrowers cannot repay their loans based on current interest rates.

The search-for-yield crowd was banking on steep rate cuts this year to bail themselves out of exposures to cyclically vulnerable sectors, but they have failed to materialise.

Trump will further tilt these probabilities against zombie companies, low-yielding commercial property, marginal residential borrowers and the non-banks that finance them.

RBA likely to keep rates high

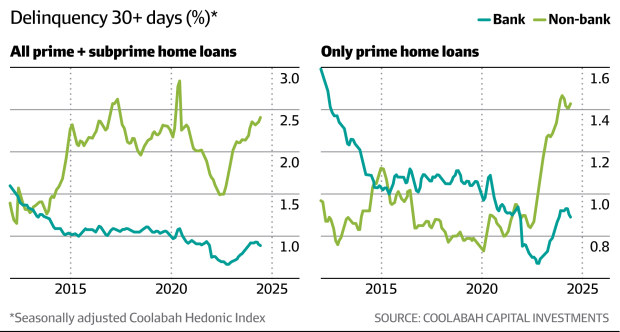

One system Coolabah has developed in-house is a proprietary compositional-adjustment methodology for measuring the arrears (or default) rates on Aussie bank and non-bank home loans that have been sold to investors (or securitised) via bonds, which we published in 2019. The Reserve Bank of Australia has copied this method for its own analytical purposes.

This system takes portfolios of home loans and controls for factors that might artificially influence the headline or official arrears rates in a spurious manner, including the life of the loan, the type of borrower, the amount by which they have leveraged their home, the date the bond was issued, and so on. We also seasonally adjust the data.

It is important to control for artificial influences on default rates because they can drive incorrect conclusions. A surge in bond issuance can, for example, suppress the headline home loan default rate as reported by Standard & Poor’s, while the real, or underlying, default rate is actually rising rapidly. This is because new bond issues are structured to comprise portfolios of loans that are default free.

Our system continues to show a striking bifurcation in the default experience of regulated banks and unregulated non-banks. Whereas non-bank lenders are suffering a dramatic increase in their arrears, which the RBA has also confirmed, the much larger and more significant banking system has only experienced a normalisation in the share of borrowers falling behind on their repayments.

This is partly a function of the fact that since the first 2008 subprime crisis, regulators forced banks to stop lending to borrowers who have a very high probability of defaulting on loans, which has pushed these households and businesses into the arms of private credit funds and non-bank institutions.

With the RBA likely to keep rates high, and possibly lift them again next month (even though Martin Place is desperate to avoid such an outcome), this situation is only likely to get worse.

A similar state of affairs is playing out in the US with respect to commercial real estate loans. The Wall Street Journal recently reported that defaults in “the commercial real-estate debt market are surging, triggering losses”.

More specifically, defaults on single-asset and single-borrower loans to commercial property owners have tripled to almost one-in-10 this year at the same time as more than half of all these loans are due for repayment by 2028.

“The losses are particularly jarring for investors because credit-rating firms initially gave many of the bonds triple-A ratings … Bonds are getting hit now because debt is coming due on properties that were able to limp along for years,” the article said.

“This is a cautionary tale for Aussie private credit investors given their portfolios are mostly focused on financing riskier commercial property borrowers that cannot get money from more conservative banks.”

It would not surprise this columnist if we see the emergence of a second subprime crisis, which this time would affect non-banks rather than banks. That is good news for the wider economy because non-banks represent only a small minority of it, which is why regulators are relatively relaxed about these marginal lenders blowing up. Of course, the risk of a second subprime crisis is undoubtedly heightened if Trump comes to power.

The arguably more meaningful shift in a Trumpian world would be any material change in the long-term cost of capital, or discount rate, that determines the valuation of all assets. Simply put, interest rates are likely to remain higher than the counter-factual, which in turn implies lower asset prices

...today Donald Trump said he will bring inflation down except...

Featured News

Featured News

The Watchlist

VMM

VIRIDIS MINING AND MINERALS LIMITED

Rafael Moreno, CEO

Rafael Moreno

CEO

SPONSORED BY The Market Online