..retail CBDC is off the radar, for now. RBA warms to its own digital currency – but only for other banks James EyersSenior Reporter

Sep 18, 2024 – 11.13am

The Reserve Bank is growing more confident that it can create a new digital version of the Australian dollar to save banks and other participants in financial markets billions each year by streamlining the settlement of transactions.

However, it remains sceptical about digital cash for consumers. It is concerned that savings would be withdrawn from banks if they could be deposited into a digital wallet overseen by the central bank.

The RBA is looking to create new forms of digital money to help streamline the settlement of transactions.

The RBA and Treasury are working together to evaluate the opportunities and risks of creating new forms of digital money in Australia.

The move was prompted by the advent of cryptocurrencies and investment banks developing blockchain infrastructure to make trading easier and cheaper.

Blockchains are digital ledgers that allow trades and payments to settle instantly. They remove the need for clearing houses and reduce processing costs.

The RBA is considering whether a state-backed digital form of the Australian dollar – the eAUD – could help banks improve back-end processes.

Project Acacia – the RBA’s codename for the work – will focus on “opportunities to uplift the efficiency, transparency and resilience of wholesale markets,” RBA assistant governor Brad Jones said in a speech in Melbourne on Wednesday.

The RBA said it would launch a new project experimenting with “tokenised” commercial bank deposits, referring to digital tokens that represent money. These tokens can be used on blockchains to settle purchases of property or commodities.

“With the strong endorsement of the [RBA] Payments System Board, I can confirm that the RBA is making a strategic commitment to prioritise its work agenda on wholesale digital money and infrastructure,” Mr Jones said. “Unlike a retail [central bank digital currency] that would be issued for use among the public, a wholesale [currency] would represent more an evolution than revolution in our monetary arrangements.”

The focus puts Australia ahead of other global central banks considering the technology. “We are among the leaders with our work evaluating different ways that digital central bank money can be implemented to facilitate efficient ‘atomic’ settlements of digital asset trades,” said Talis Putnins, chief scientist at the Digital Finance CRC, which has been working with the RBA on the project.

The RBA’s support for new forms of wholesale money contrasts with its concerns about the development of a digital currency for consumers, such as those launched in China and being considered by the European Central Bank. It is worried a central bank-issued digital form of cash could accelerate bank runs in a financial crisis.

“The potential benefits of a retail [currency] generally appear modest or uncertain at the present time, relative to the challenges it would introduce,” Mr Jones said.

At that Summit last year, Mr Jones said there would be benefits of some $17 billion from using digital currencies in markets. This includes cost savings from shorter settlement times, which would reduce the amount of capital held to protect against failed transactions.

Central banks have been forced to consider their versions of digital currencies since the creation of bitcoin 15 years ago challenged fiat currency systems by creating a borderless, native currency for the internet.

Bitcoin has a market capitalisation of $US1.2 trillion ($1.8 trillion) and is trading at almost $90,000 a coin after it more than doubled over the past 12 months.

Facebook’s 2019 announcement that it would create a cryptocurrency called Libra also rattled central banks and governments. Regulators shut down the project, but it accelerated the development of official digital currencies as central banks sought to maintain control of their monetary systems. Digital cash alarm

Mr Jones’ speech on Wednesday set out a range of concerns about issuing a central bank digital currency into the Australian retail market.

The most significant concern is that a digital currency for the public could increase the risk, or amplify the effects, of bank runs.

“In times of stress, access to a risk-free [digital currency] would increase the ability of panicked households to switch out of bank deposits en masse,” Mr Jones said.

“The events at Silicon Valley Bank last year offered a cautionary tale over the risk of rapid-fire bank runs in the digital age – one that could be magnified if bank deposits were convertible into [central bank digital currencies] at the touch of a smartphone.”

He said RBA staff had examined the effects on bank liquidity if Australian households simultaneously transferred $5000 from their deposit account into a central bank digital currency for consumers and had found this would reduce banks’ liquidity buffers by between 40 and 60 per cent.

Still, the RBA has not ruled out creating a form of digital cash in the future. It will host a series of workshops on the topic next year.

At a wholesale level, the potential benefits of a central bank digital currency are clearer.

Professor Putnins said potential gains from a wholesale CBDC in Australia are more than $5 billion a year, mostly efficiency gains tokenising assets in existing markets. “For banks, a wholesale CBDC could be an efficient interbank settlement layer that enables more innovation like tokenised bank deposits and giving customers access to digital assets,” he said.

Wall Street investment banking giants including Goldman Sachs and JP Morgan have built blockchains to manage commodity trading and the trading of debt instruments, including money market funds.

Many of the benefits were explored during 14 pilot projects the RBA conducted last year.

Mr Jones pointed to research by global regulators examining how a central bank digital currency, combined with blockchains, could reduce counterparty and operational risks, improve capital efficiency and lift transparency, especially in greenfield markets where digital representations of assets could be updated and verifiable in real-time.

He said price discovery and placement in the $780 billion market for bank term deposits – around 25 per cent of bank funding in Australia – still occurred in branches and over emailed spreadsheets and phone calls, “in an opaque, labour-intensive manner that is little changed from 25 years ago. This begs the question – is this the best we can do?”

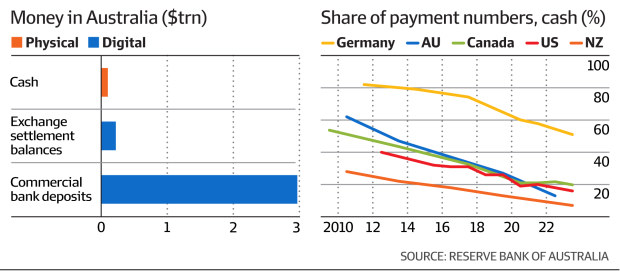

The RBA already provides banks with a digital form of money known as “exchange settlement” balances. Similarly, a wholesale central bank digital currency could be issued to eligible financial institutions and serve as the ultimate safe asset in the settlement of wholesale market transactions.

What would be new is that this could sit on different types of ledgers, both centralised or decentralised, possibly alongside “tokenised” assets to offer greater functionality.

“This could support asset settlement and other wholesale payments in new ways,” Mr Jones said.