John P. Hussman, Ph.D.

President, Hussman Investment Trust January 2025

That the free-enterprise economy is given to recurrent episodes of speculation will be agreed. There is protection only in a clear perception of the characteristics common to these flights… There are, however, few matters on which such a warning is less welcomed. Those involved with the speculation are experiencing an increase in wealth – getting rich or being further enriched. No one wishes to believe that this is fortuitous or undeserved; all wish to think that it is the result of their own superior insight or intuition. Speculation buys up, in a very practical way, the intelligence of those involved. As long as they are in, they have a strong pecuniary commitment to belief in the unique personal intelligence that tells them that there will be yet more.” – John Kenneth Galbraith, A Short History of Financial Euphoria

On December 6, the S&P 500 set the most extreme level of valuations on record, exceeding both the 1929 and 2000 market peaks on measures that we find best-correlated with actual, subsequent 10-12 year S&P 500 total returns across a century of market cycles.

Reliable valuation measures are enormously informative about both long-term investment returns and the potential depth of market losses over the completion of any given market cycle. At the same time, valuations are of strikingly little use in projecting market outcomes over shorter segments of the market cycle. Investor psychology – the desire to speculate, or the aversion to risk – has a much stronger impact, which is why we also have to attend to factors including market internals, sentiment, short-term overextension / compression, and monetary policy (while unfavorable market internals dominate monetary easing, favorable internals amplify it).

Amid the untethered enthusiasm about artificial intelligence, and prospects for deregulation and lower corporate taxes, it’s worth repeating that despite all the society-changing innovations of the past 20-30 years, both GDP and S&P 500 Index revenues (which include the impact of stock buybacks) have grown at an average rate of only about 4.5% annually. That’s slower, not faster, than the growth rate during the preceding half-century.

Yes, the largest companies are very profitable, but that’s nearly always true at speculative extremes. That cohort of mega-cap companies is constantly changing, and except on their approach to extremes like 1929, 1972, 2000, and today, the companies with the largest market capitalizations have historically gone on to lag the S&P 500 over time.

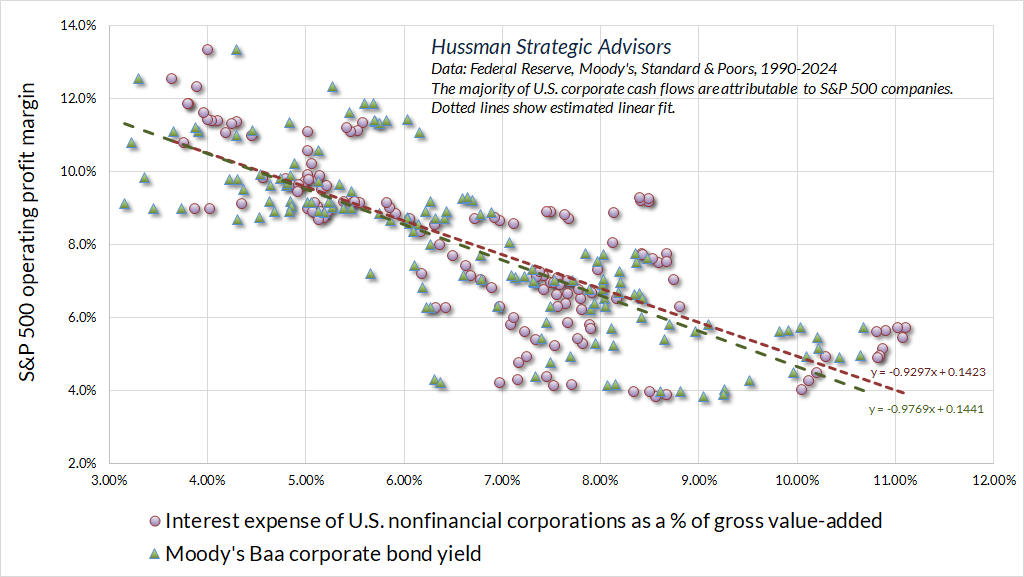

Investors regularly forget that the central feature of free-enterprise is the continual emergence of innovation-driven “new eras” in which both profit margins and growth rates are trajectories rather than durable numbers. As I reviewed in last month’s comment, Ring Out Wild Bells, the primary driver of rising profit margins since 1990 has not been rapid productivity growth or higher EBIT margins (earnings before interest and taxes). The simple reality is that most of the expansion in profit margins since 1990 is explained by falling interest expense, thanks to persistently declining interest rates that companies temporarily locked in at the 2020-2021 lows.

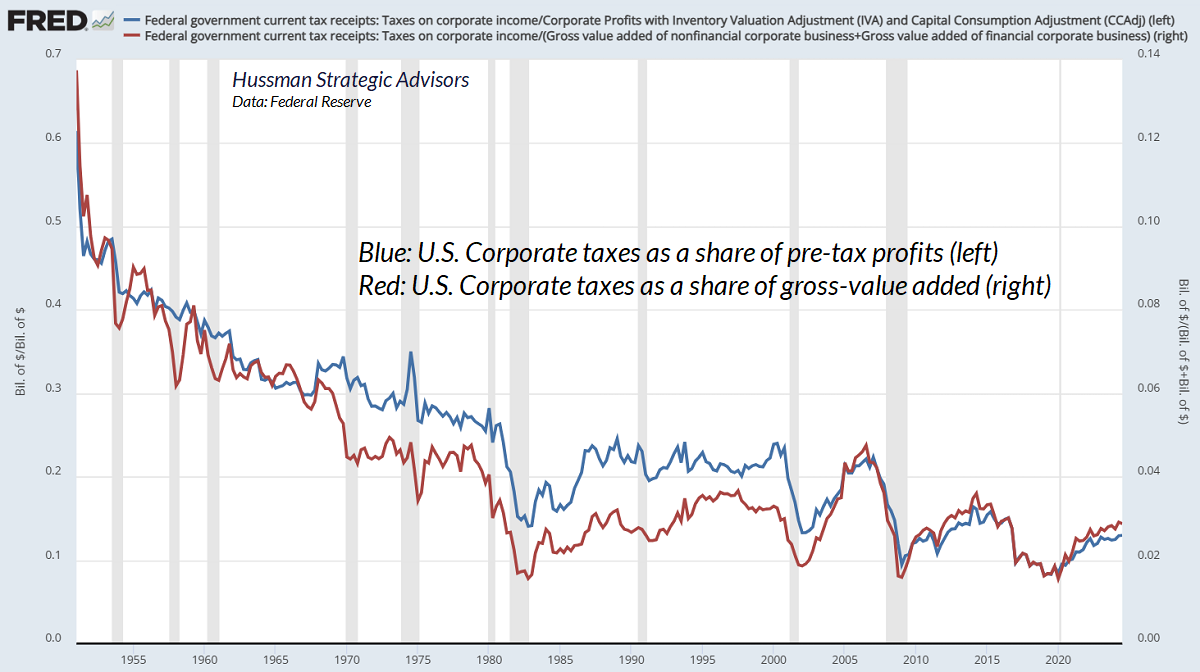

Meanwhile, most of the historical impact of corporate tax reductions was reflected in profit margins by the early 1980’s. Even if corporate taxes were reduced by one-third from here, and assuming those tax cuts were sustained permanently, the value of that tax reduction would amount to just 4% of market capitalization, and after-tax profit margins would increase by less than 1%.

Having priced the stock market at elevated multiples of record earnings, investors now require profit margins to sustain record highs permanently – simply for growth in earnings and payouts to match the 4.5% revenue growth rate of recent decades, and they require the S&P 500 price/revenue ratio to remain at a permanently high plateau, three times its historical norm.

Given our own 4-year baseline expectation for real GDP growth of just 1.5% (see The Turtle and the Pendulum), even 4.5% nominal growth would require either a 3% inflation rate in the coming years, or a 2% inflation rate coupled with a jump in productivity that fully restores the 1948-2000 average.

One might hope for higher inflation, imagining that it might produce higher nominal growth and accompanying market returns, but that would require valuations to remain at record extremes. Unfortunately, valuations are the first casualty of persistent inflation. In fact, except when valuations have been at least 25% below historical norms, the S&P 500 has lagged Treasury bills, on average, when consumer price inflation has been anything over 4%.

There’s no question that investors are eager to justify record valuation multiples by appealing to the growing share of technology companies in the S&P 500. Yet the technology sector itself is trading at the highest multiple to revenues on record. Meanwhile, the growth rate of overall S&P 500 revenues, which include the technology sector, is below historical norms while the S&P 500 price/revenue multiple is three times its historical norm, easily eclipsing the 1929 and 2000 peaks.

Still, for the moment, neither valuations nor arithmetic matter to investors. As Galbraith observed, “As long as they are in, they have a strong pecuniary commitment to belief in the unique personal intelligence that tells them that there will be yet more.”