...price performance of a stock or an asset class is more a function of fund flows than actual fundamentals.

...when you have net fund inflows, price rises, and conversely when you have net fund outflows on a consistent basis, price falls.

...fund flows are determined by a variety of factors and foremost on perception and anticipation of the future.

...when Gold had to compete for funds with soaring tech stocks and speculative money going into BTC, it did not get the fund flows to drive its price higher as much as now that the tech and BTC bubble appears to have lost its mojo.

....hence the Capital Rotation Event (CRE) out of tech/equities into Gold.

....one asset class loss is another asset class gain. Be on the right side of where the fund flows move to.

Gold Soars as Goldman Sees $4,500 Tail Risk in 2025

Intro:

Since the reports discussed here-in were published, Gold has rallied over 1% percent touching $3,059 and Silver over 2% touching $30.40 before settling in at $3052 and $34.30 respectively as of this writing.

Goldman, BOA Unshackle Gold

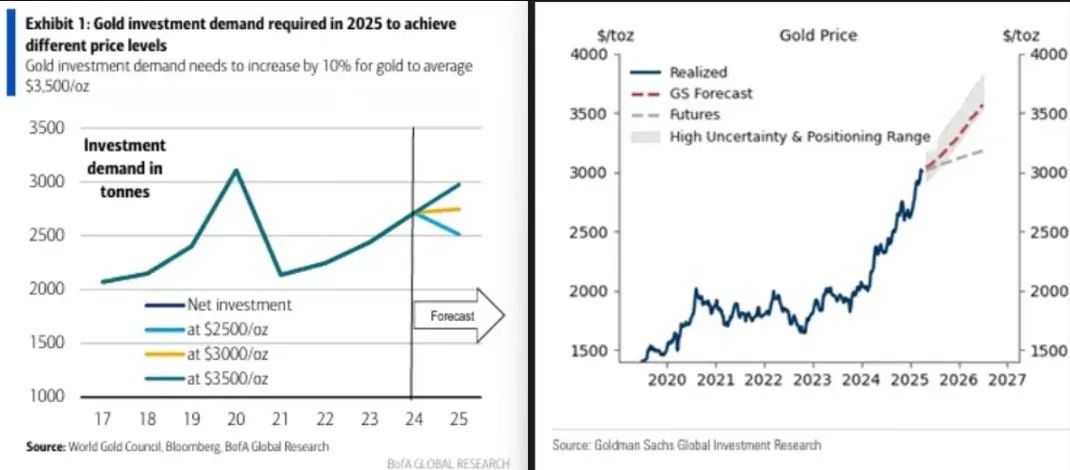

Bank of America says: Gold at $3,500/oz: We believe gold could rally to $3,500/oz if investment demand increases by 10%, so we make this our new price forecast.

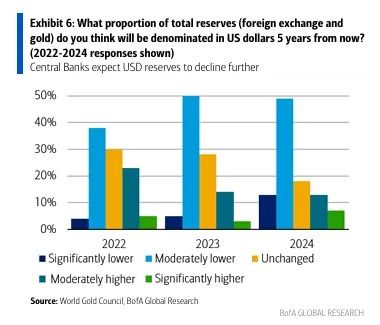

Goldman Sachs says: We raise our end-2025 forecast to $3,300/toz (vs. $3,100) and our forecast range to $3,250-3,520, In extreme tail scenarios gold could plausibly trade above $4,200/toz by end-2025 and exceed $4,500/toz within the next 12 months.

We Say: Gold is now unshackled. Once a proxy for the dollar and interest rates, the metal is free to find a price that reflects actual global demand. Our own Price targets were revealed March 14th where we offered $3600 to 4285 as price targets

Bank of America (left) and Goldman Sachs Raise base targets to $3500 and $3300 Respectively…

The major banks—long tethered to traditional models—are similarly unshackled in their analysis. What was once viewed as a sleepy, correlated asset is now being subjected to fundamental analysis. Analysts are translating measurable demand into constrained supply and developing legitimate price projections. While some of their sentiment might appear euphoric in the short term, it’s not fantasy—it’s based on tangible demand that has emerged and been unlocked.

And now, the big banks are playing to their strengths. Beyond anticipating customer order flow, their core strength lies in quantifying an objective. We’re seeing that in real time. In just the past 24 hours, two major institutions—Bank of America and Goldman Sachs—have announced raised price targets for gold.BOA’s View: China and CBs Have Much More to Buy

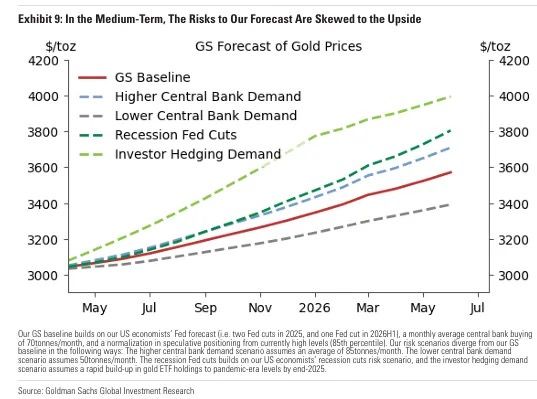

“Central banks (CB) currently hold about 10% of their reserves in gold, and could raise this figure to +30% to make their portfolios more efficient.”

Bank of America’s revised target builds on a theme they introduced last month. Their key idea: If Chinese insurance companies are permitted to purchase gold for both their balance sheets and client-facing products, how much could they realistically buy—and what impact would that have on price?

That’s one of the focuses of their current report.

Another key area—arguably more innovative—is Bank of America’s further quantification of potential central bank gold purchases in the current geopolitical environment. Presently, central banks hold approximately 10% of their reserves in gold. Bank of America presents a case that this share could climb toward 30%. They justify this projection, explain its relevance, and openly discuss the risks involved. We agree.

It’s worth noting: the Chinese insurance company gold purchases are economically separate from central bank buying. Here are the nuts and bolts:

China’s insurance move, we contend, is akin to Ronald Reagan’s early 1980s decision to liberalize stock ownership for U.S. insurance companies. That policy helped trigger what became the largest equity bull market of all time. We cannot emphasize this parallel enough. China is replicating US financialization steps done in the early 1980s but doing it with Gold

- China has initiated a pilot program allowing major insurance companies to purchase gold—both for their own balance sheets and for client investment products. GoldFix believes China domestic insurers have ear marked US$25bn to be invested into Gold per the mandates rules of the pilot program.

- Putting concrete numbers behind this, BOA believes 300 tonnes of gold purchases or 6.5% of the annual physical market would be taken off market.

If BOA is correct, this kind of new demand alone correlates with approximately $500 price dislocation

This will be a similar inflection point for gold—a likely harbinger of the biggest gold bull market we’ve ever seen. Now let’s move to Goldman Sachs for a quick summary of their analysis

Goldman Sachs Steps Forward

“We raise our end-2025 forecast to $3,300/toz (vs. $3,100) and our forecast range to $3,250-3,520, reflecting upside surprises in ETF inflows and in continued strong central bank gold demand.”

Goldman just raised their year-end target from $3,100—their prior conservative estimate—to $3,300. Notably, they were among the first banks to publish a quantification framework for gold demand, detailing the flows from over-the-counter markets in Europe—specifically from London to Switzerland and beyond.

Key to Goldman’s analysis has been upside surprises in CB demand (light blue) in identifying un(der)reported Gold Flows to China…

They applied a methodology where a specific amount of Central Bank demand equals a projected increase in price, supported with real delivery and off take data.

Two weeks ago, before these reports were received, GoldFix published its own target—also grounded in fundamentals—and we projected $3,600 and $4,285. Odd numbers, yes, but that’s what the numbers told us. “Based on ETF flows we should see an additional $600, and possibly $1,285 on top of current prices. Placing the Price between $3600 and $4285 when those ETF levels are reached— Assuming no significant decline or increase in CB buying.”

Back to Goldman.

When the Banks first released its new valuation methodology four months ago, it faced pushback. Some banks resisted, citing Fed rate hikes and a strong dollar as headwinds that would eventually cap gold’s rise.

But even those banks began to adjust, especially after seeing continued—and surprising—central bank buying post-U.S. elections. The scale of these purchases forced a reevaluation.

Today, Goldman Sachs not only reaffirmed their revised $3,300 target, they also upped their aggressive case from $3,500 to $4,500.

In extreme tail scenarios gold could plausibly trade above $4,200/toz by end-2025 and exceed $4,500/toz within the next 12 months. We view this as a very low-probability event, but include it to illustrate the nonlinear upside to gold prices.

That new projection is based on 3 variables:

Goldman also released a detailed 10-question framework to explain their rationale. We’ll be sharing that with premium subscribers this weekend.

- China: They now anticipate even stronger Chinese demand than previously modeled.

“If the largest official buyer–China –were targeting an allocation of 20%, and maintained an average pace of ~40 tonnes per month, in line with recent patterns….”- Insurance Companies: They’re also now publicly acknowledging the insurance company gold-buying angle, as Bank of America already has.

- Western Buying is bullish, western selling is not bearish

“Over the span of 6 weeks, speculative length declined by 150 tonnes, yet prices remained supported by structural demand, including a notable pickup in gold ETF inflows (~80 tonnes) and what we estimate to be ongoing central bank buying amid rising US policy uncertainty”

Final Comment:

The BOA report is incredibly thorough— so comprehensive it alone warrants two separate analyses. The Goldman report also includes discussion on the risk to Gold prices if Russian assets were unfrozen. Both will be covered in full this weekend and shared with our friends at Scottsdale next week. Together, the works disclose much more than these banks generally discuss.

These reports, in combination with the massive Gold repatriation and escalation of tariff risks, make it increasingly likely the slow advance in gold prices over the last 2 years may accelerate as the global divisions become more permanent. The next signpost will be July 1st when Basel 3 begins to rollout in the US.

Its Over, page-26045

Featured News

Featured News

The Watchlist

PAR

PARADIGM BIOPHARMACEUTICALS LIMITED..

Paul Rennie, MD & Founder

Paul Rennie

MD & Founder

SPONSORED BY The Market Online