...Eric Fry outlines why Gold is your ultimate hedge bet against any Disorder.

...and we know that Disorder rules today, tomorrow and the near future.

Bullish on Disorder, and Betting on Gold

“Gold is a bet on monetary disorder – indeed, on other kinds of disorder, too, including fiscal, geopolitical and presidential,” the astute financial writer James Grant observed recently.

This bet has been paying off nicely for last several months, but I suspect the final payoff has not yet arrived. The world does not lack for any of the disorders Grant mentions, least of all fiscal disorder, an elegant term for soaring government deficits and debts.

Even though trade deficits are the boogeyman du-jour, government deficits can be far more hazardous to the health of an economy. When a nation’s finances spiral out of control, its currency usually tumbles down a long flight of stairs… and rarely recovers.

Many are the countries throughout history that have lost control of their finances, and then watched their currencies take a bad spill. For example, during the “Latin Debt Crisis” of the 1980s, when several countries south of the border defaulted on their debts, massive currency devaluations followed. The Mexican peso lost a staggering 99.8% of its value against the dollar. The Brazilian cruzeiro and Argentine peso fared even worse – meaning they both lost more than 99.8% of their values!

During the Asian currency crisis of 1997, the Thai baht, Malaysian ringgit, and Indonesian rupiah dropped 54%, 50%, and 88%, respectively. The following year, the Russian Debt Crisis slashed the ruble’s value by 75%.

Crises like these create jarring economic dislocations, but gold loves them! To borrow from a famous line in the ancient feel-good movie, “It’s a Wonderful Life”: Every time a currency stumbles, the gold price gets its wings. That’s because a rising gold price is simply the flipside of a falling currency value.

The chart below tales the tale. It shows gold’s price gain against select currencies during the last 25 years. For example, the yellow metal has soared more than 3,300% against both the Brazilian real and the Russian ruble since 2000. It has also gained more than 2,300% against both the Indonesian rupiah and the Mexican peso.

Gold’s massive gains against those four troubled currencies are not entirely surprising. But what is quite surprising is that gold has also produced a massive gain against the world’s reserve currency. Since 2000, the yellow metal has soared more than 1,100% against the U.S. dollar. In other words, even though the value of the U.S. dollar has not visibly collapsed during the last 25 years, its value has tumbled more than 90% in gold terms!

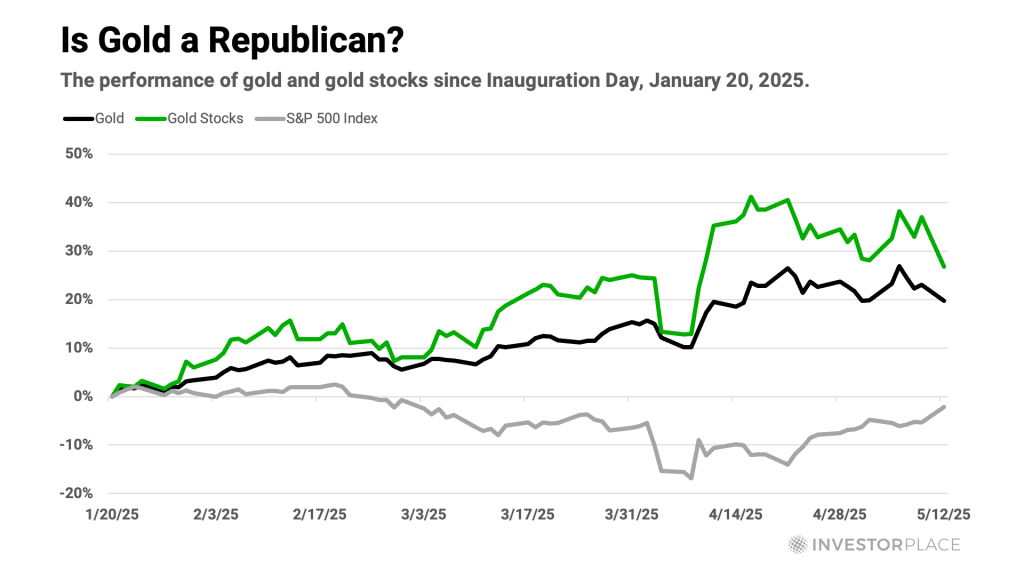

Like a hurricane moving across warm waters, this trend appears to be gaining strength and fury. Since Inauguration Day, the U.S. dollar has tumbled 19% in gold terms.

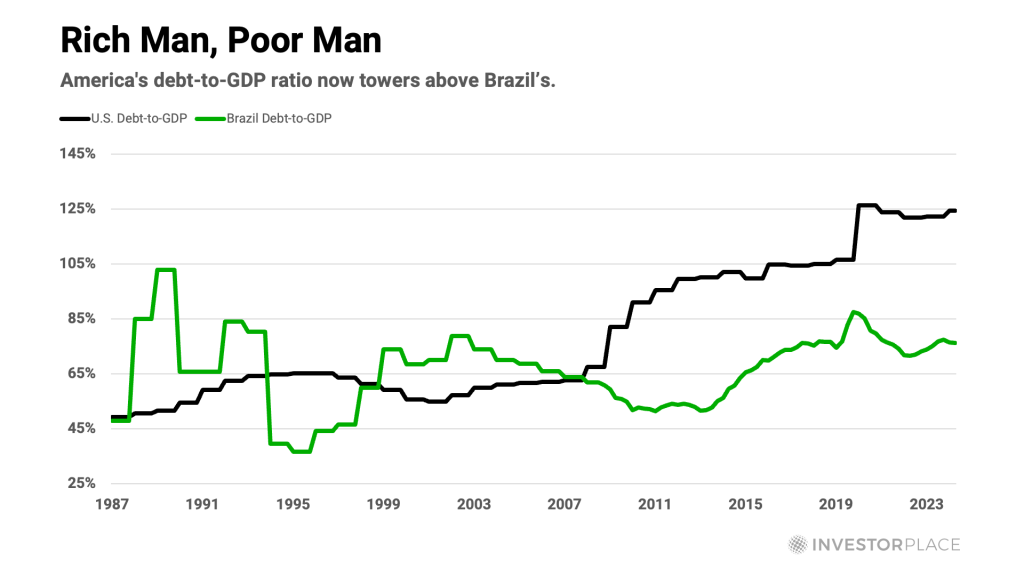

Although several factors are weighing on the dollar’s value, the U.S. government’s towering debt burden is certainly high on the list. The chart below provides a helpful perspective.

It shows the comparative fiscal trends of the U.S. and Brazil during the last four decades. Back in 1990, for example, U.S. government debt totaled just 52% of GDP, while Brazil’s was exactly double that level at 104% of GDP.

U.S. indebtedness inched higher over the next few years, but then dipped lower again during the budget surpluses (remember those?) of the Clinton administration. But it’s been all uphill ever since.

Year-by-year, throughout both Republican and Democratic administrations, U.S. indebtedness has surged. Today, America’s total government debt tips the scales at a hefty 124% of GDP – an embarrassingly high, “banana republic” level.

Meanwhile, our “less prosperous” neighbor to the south has trimmed its debt levels to a respectable 76% of GDP. Several other countries in South and Central America have fortified their national balance sheets as well. Even Nicaragua, which actually exports a significant quantity of bananas, has slashed its debt-to-GDP from more than 100% in 2003 to just 37% today.

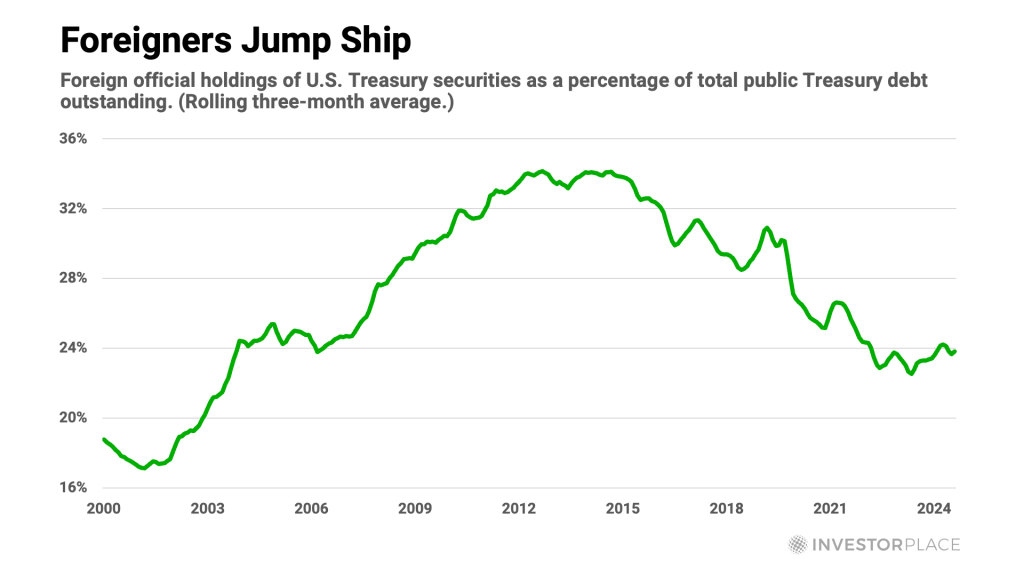

In other words, the U.S. has amassed a titanic national debt – both in absolute terms and also relative to many of the world’s “poor” countries. Apparently, some foreign investors have taken notice of this unsettling trend and are subsequently lightening up on Treasury securities. The percentage of U.S. Treasury debt owned by foreigners peaked at 34% in 2015, and it has been sliding lower ever since.

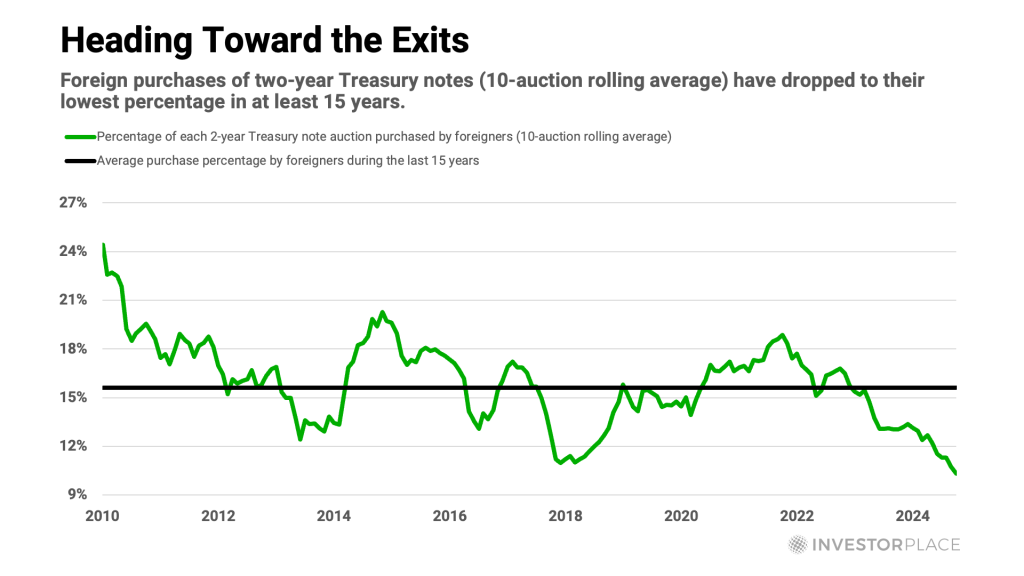

Anecdotal evidence suggests that some foreign central banks have been selling their Treasury securities with greater urgency during the last few months. Foreign purchases of two-year Treasury securities have dropped to their lowest levels in at least 15 years. The foreign appetite for all other Treasury securities from 3-year notes to 30-year bonds is also waning, and also close to 15-year lows.

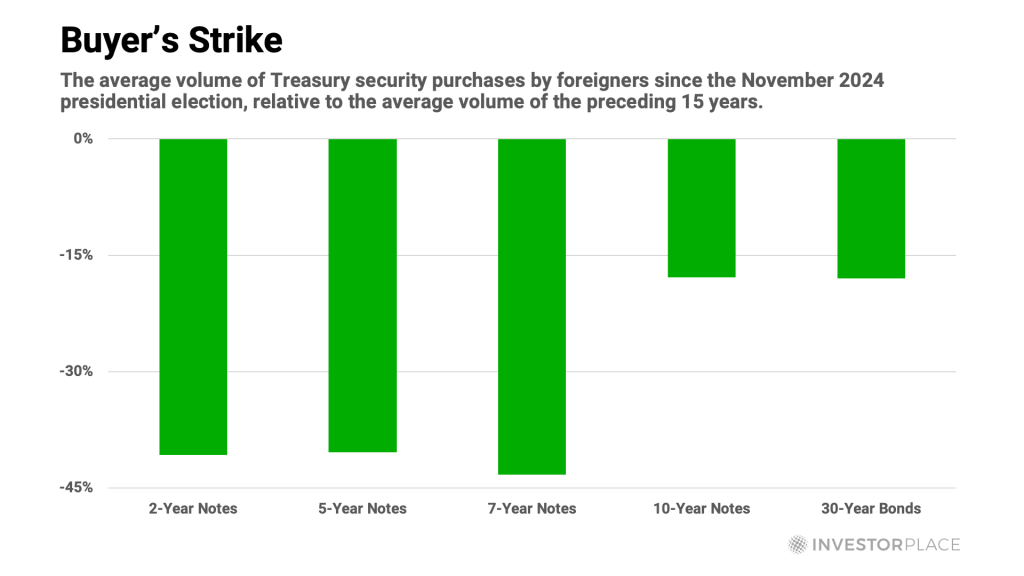

Somewhat ominously, the decline of foreign participation in U.S. Treasury auctions has become particularly pronounced since the November 2024 presidential election. As the chart below shows, the average foreign participation in Treasury auctions has dropped sharply across the entire Treasury curve – from 2-year notes to 30-year bonds.

Each bar in the chart shows the average drop in foreign buying of various Treasury securities at every auction since November 5, 2024, compared to the 15-year average. For example, foreign buying of 2-year Treasury notes since November 5 has been 41% lower than the average foreign buying of 2-year notes during the preceding 15 years.

In addition to their non-buying, some of America’s creditors are also selling Treasurys. Japanese investors, for example, sold more than $20 billion worth of U.S. Treasurys last month.

As foreigners withdraw capital from the U.S., they appear to be funneling a portion of it into the gold market. According to calculations by “The Gold Observer,” the People’s Bank of China (PBOC) purchased about 570 tons of gold last year, lifting its stash of the monetary metal to about 5,065 tons.

In round numbers, therefore, the PBOC forfeited about $1.5 billion of interest income last year by buying gold rather than 10-year Treasurys. But don’t cry for China; the value of China’s gold horde has soared by roughly $150 billion dollars during the last 12 months. Clearly, China’s bet on disorder is paying off handsomely… and could continue to do so.

If, as Grant asserts, gold is a “bet on disorder,” America’s rising indebtedness, along with the waning desire of foreigners to finance it, could provide ample disorder to elevate the gold price. Political Chaos, Golden Reward

Grant also mentions geopolitical and presidential disorder as additional fuel for a gold rally. The aromas of such disorder are wafting on the breeze already, and they could certainly become more pungent and disruptive. A dose of stock market disorder could also trigger the gold-buying impulse.

Admittedly, gold and gold shares have been performing well for months already, which means they could be due for a significant correction. In the longer term, however, I expect the yellow metal and its proxies to continue performing well, and fulfill their historical role as a hedge against uncertainty and disorder.