The ISM Non-Manufacturing Business Activity Index Shows to What Unfathomable Extent the US Economy Has Collapsed

by Wolf Richter • May 5, 2020 •

But delivery times explode due to supply chain turmoil. The charts are brutal.

By Wolf Richter for WOLF STREET.

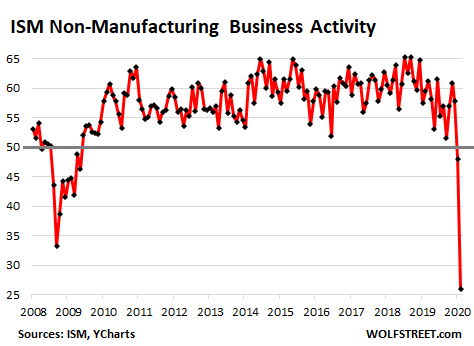

Business activity and production at US non-manufacturing industries in April collapsed to the lowest level since inception of the ISM Non-Manufacturing Index in 1997, from already weak levels in March.

Only one industry, Finance & Insurance, reported an increase in business activity; the remaining 17 industries – ranging from Arts, Entertainment, and Recreation to Utilities – reported a decline in business activity, with some of them essentially shut down in large parts of the US. The ISM Business Activity Index plunged to 26%. A level below 50% means contraction (historic data from YCharts, current data from ISM):

This is how executives see business at their own companies. The Institute of Supply Management gathers these surveys from executives on a monthly basis. The names of the companies are not disclosed in the report. The additional comments by the executives about their own companies are revealing:

Finance & Insurance: “Due to increased loans from [the federal] stimulus package, [we are] seeing an increase in new business.”

Arts, Entertainment & Recreation: “COVID-19 pandemic has forced our business to close as of March 17, 2020. We do not have a re-opening date yet; our purchasing activity has been greatly reduced due to the current business environment.”

Agriculture, Forestry, Fishing & Hunting: “The COVID-19 situation has created significant challenges for the agricultural sectors. Milk prices have declined 29 percent in a few weeks. Milk is being dumped on farms because of the loss of markets. Cattle prices are down 28 percent, pork prices down 24 percent, [and] all agriculture sectors are facing significant price declines. Our agriculture economy is challenged, with poultry, pork, and beef processing plants closed due to COVID-19 cases or impaired due to employees afraid to work side-by-side with other employees. Farmers cannot sell fat cattle locally due to processing plant shutdowns.”

Construction: “COVID-19 is altering the operation, supply chain and sales process of home-building. Stay-at-home orders have hampered business in residential construction. As ours has been deemed an essential industry, we continue to navigate changing guidelines and restrictions on a daily basis.”

Management of Companies & Support Services: “The oil exploration sector is very weak, with the record low price of oil and the country’s shutdown due to the COVID-19 threat. We are hopeful for a bump in activity once the country starts to reopen.”

Health Care & Social Assistance: “COVID-19 has halted much of our standard work to procure items for our organization. It’s halted much of the world, except for health care. Distributors were woefully unprepared for the spread of this pandemic, and many health-care systems/providers depend on them for inventory planning and availability. Combine that with the global [surgical] gown recall just before the pandemic struck — and isolation masks are created from the same material as isolation gowns — and you had a perfect storm for chaos across the supply chain. It will be very hard for major medical distributors who did not manage their core customers well to recover from both the gown recall and the pandemic. It also provided some insight into whether or not the distributor partners were actually skilled at inventory planning and movement. I believe that the healthcare supply chain landscape will change dramatically after this.”

Wholesale Trade: “As an essential business, we have remained open during the month. A significant number of our customers are closed (i.e. schools) and other have substantially reduced their buying (i.e. hotels, office building). Sales of janitorial, sanitation, and paper products [have] increased across all business lines, but other categories are greatly reduced. Overall, reduction in sales of 20 percent to 30 percent.”

Educational Services: “The university abruptly transitioned from students on campus to remote teaching for the spring quarter; however, the number of students registered for the quarter has remained consistent with previous years. Overall, activity dropped 17 percent compared to February and 31 percent compared to March 2019.”

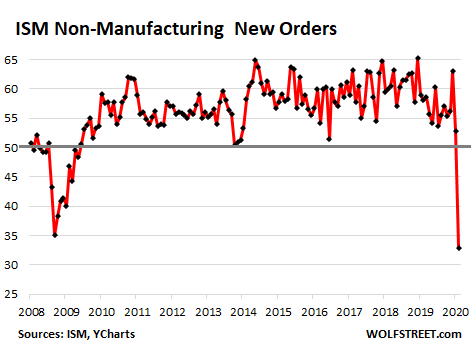

New Orders plunged.

The ISM Non-Manufacturing New Orders Index plunged 20 points to 32.9%. Below 50% means contraction, and this was the first contraction of new orders in over 10 years, amid comments by the executives, such as these: “No new orders booked. Activity level is pretty high, [and we’re] trying to figure how to do business remotely”; and “Core business activities at a virtual standstill.”

Only two of the 18 industries reported growth of new orders: Finance & Insurance and Public Administration. The remaining 16 industries reported declines in new orders (historic data from YCharts):

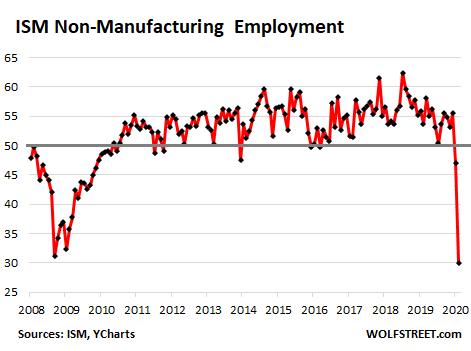

Employment plunged.

All 18 industries reported a decline in employment in April, and the ISM Employment Index plunged 17 points to 30%. Below 50% means contraction, and the March level of 47% was already in contraction (historic data from YCharts):

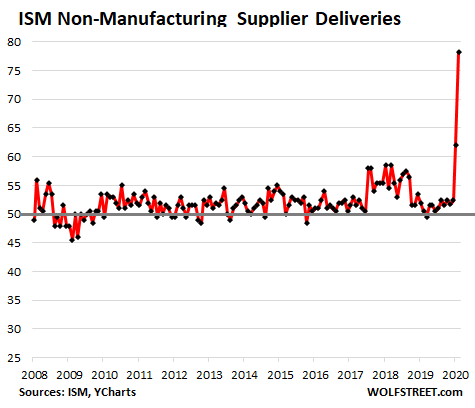

But supplier delivery times exploded to new high.

The Supplier Deliveries Index tracks delivery times by suppliers, and longer delivery times increase the index. Due to supply-chain disruptions, the index surged to an all-time high of 78.3% in April. But during Financial Crisis 1, in 2008-2009, there were no supply chain disruptions, and a decline in demand produced faster supplier deliveries, and the index fell during that time, as would be expected during a normal downturn (historic data from YCharts):

In a normal economy, long delivery times mean there is a lot of demand and a lot of economic activity, so the supplier deliveries index is inverse in the overall Non-Manufacturing ISM Index (chart below) and counts as a positive. But in this lockdown economy, supplier deliveries aren’t slow because of demand but because of supply chain disruptions. And this, the ISM points out, “limited the decrease in the composite NMI.”

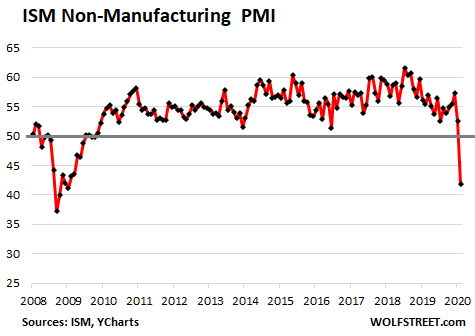

The Composite Non-Manufacturing Index still plunged.

Without the boost by supply chain disruptions to the Suppliers Delivery index, the overall index would have fallen even more sharply, but it nevertheless plunged 10.7 points to 41.8%, the first contraction since December 2009, and the lowest reading since March 2009, amid comments by the executives, such as, “Fewer resources to do work,” and “All non-essential procedures have been cancelled or delayed” (historic data from YCharts) :

In terms of the Composite Non-Manufacturing Index, two industries experienced growth in April:

The remaining 16 industries reported declines in April, listed in order:

- Public Administration

- Finance & Insurance.

The ISM report summarized the comments of the executives in these industries; they “are concerned about the continuing coronavirus impacts on the supply chain, operational capacity, human resources and finances, as well as the uncertain timelines for the resumption of business and a return to normality.”

- Arts, Entertainment & Recreation;

- Agriculture, Forestry, Fishing & Hunting;

- Retail Trade;

- Other Services;

- Wholesale Trade;

- Construction;

- Transportation & Warehousing;

- Mining;

- Professional, Scientific & Technical Services;

- Information;

- Accommodation & Food Services;

- Management of Companies & Support Services;

- Educational Services;

- Real Estate, Rental & Leasing;

- Utilities;

- Health Care & Social Assistance.

The ISM Non-Manufacturing Business Activity Index Shows to What...

Featured News

Featured News

The Watchlist

VMM

VIRIDIS MINING AND MINERALS LIMITED

Rafael Moreno, CEO

Rafael Moreno

CEO

SPONSORED BY The Market Online