I never doubted Jeremy's wisdom, I still think he is right. But as clearly 2020 has shown us, being right about how the market ought to behave can be way different to how it actually does.

Jeremy's "mistake" was to take out a big short position on his conviction call i.e the market cannot stay disconnected for that long. He may well be right in the end , but if the powers that be now knows what it takes to prevent the next market collapse, it may take a big oversight on their part for us to experience the next Big Kahuna. Now we have two Fed eyes (Powell and Yellen) not one.

Was watching Scott Phillips of Motley Fools today making his case for a bullish 2021 for *********.

Wary market participants can either do three things - i) too scared to ever venture in again because the market could be too rich ii) decide quickly to get in early and buy the dips (like today) before the Melt-up begins or (iii) like most, wait for the Melt-up to be well in motion before deciding to jump in because it gives more comfort , if you are in Category (i) don't be in Category (iii) (because that's what the 70% of people will do) , if you stay in Category (i) that's fine you won't gain nor lose anything but will need to settle for a lower return , alternatively one can be in Category (ii) albeit progressive cautiously, measuredly and in a calculative manner.

2020 tells us Fundamentals is only one aspect in the overall buy/sell consideration. Another big and important ingredient is market narrative which appears to have a stronger influence on the market. With market narrative being important, it is important that we stay nimble , flexible and open minded.

Buying is the easy part in investing, knowing when to sell and when not to sell and how much to sell, that's the most challenging.

Shorts are dangerous games, as Jeremy has experienced.

I made two right calls over the past weeks & past month, get out of BBOZ/BBUS and lightening up on precious metals. Markets have the tendency to change course over time, what works for a period may not for the next, hence having an exit strategy as well a appropriate risk management is IMO vital to success.

Grantham's Short Call Cost His Hedge Fund Over $2 Billion

by Zero Hedge

Tue, 11/24/2020 - 17:30

Back in June, value investing legend Jeremy Grantham decided he had had enough, and in a historic reversal for his traditionally bullish GMO Benchmark-Free Allocation Fund, took down exposure to US equities from a net 3-4% to a net short position worth about 5% of the $7.5bn portfolio, "perhaps the first time the fund has turned net short US stocks since the crisis."

Grantham laid out the reasons for his bearish flip in a lengthy letter to GMO investors, writing that "we have never lived in a period where the future was so uncertain" and yet "the market is 10% below its previous high in January when, superficially at least, everything seemed fine in economics and finance. And if not “fine,” well, good enough. The future paths include many that could change corporate profitability, growth, and many aspects of capitalism, society, and the global political scene."

In short, the veteran value investor known for calling several of the biggest market turns of recent decades admitted he had lost his faith in an upside case and his sense of direction in a world of record uncertainty "which in some ways seems the highest in my experience" and as a result "in terms of risk and return – particularly of the worst possible outcomes compared to the best – the current market seems lost in one-sided optimism when prudence and patience seem much more appropriate."

Grantham also highlighted the obvious: that the market and the economy have never been more disconnected - a phenomenon which is now known as the K-shaped recovery, and pointed out that while "the current P/E on the U.S. market is in the top 10% of its history... the U.S. economy in contrast is in its worst 10%, perhaps even the worst 1%.... This is apparently one of the most impressive mismatches in history."

However, the value investing legend's most dire prediction was that "if you look back in two to three years and this market turns around and drops 50%, the history books will say ‘That looked like one of the great warnings of all time. It was pretty obvious it was destined to end badly," Grantham said, adding: "If it does end badly the history books are going to be very unkind to the bulls."

Perhaps Grantham will be proven correct and in the summer of 2022 the S&P will be a smouldering post-crash rubble of its former bull market glory, but a little over five months after Grantham made his fateful bearish call, his multi-billion fund is suffering unlike any time since the financial crisis.

According to Bloomberg, GMO’s flagship Benchmark-Free Allocation Fund, which as noted above turned net short in the early summer and which seeks returns of five percentage points above the rate of inflation, has badly underperformed risk assets so far this year. It trails the S&P 500 by 14%, and while its primary equity holdings are in emerging markets, it also lags behind MSCI’s main developing-market gauge.

And in a world where hedge fund clients demand returns here and now - especially with 13-year-old Robinhood daytraders generating triple digit returns - Grantham's dramatic underperformance has meant just one thing: a flood of redemption requests.

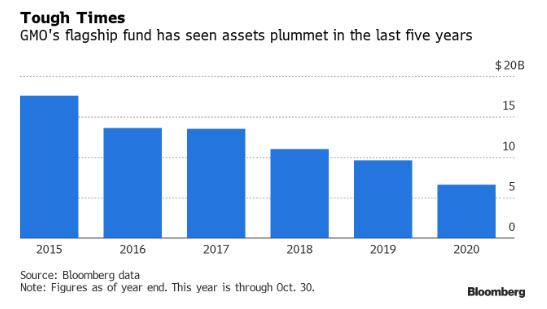

In just the past 10 months, clients have pulled $2.2 billion from the fund with assets dropping by more than half since 2015 to $6.6 billion as of the end of October.

Ironically, just as there has been a rare resurgence in cyclical, value stocks since the Pfizer vaccine news which has crushed the opposing, momentum trade which made so many call-trading teenagers millionaires, GMO's Inker said in an email Monday that he understands why enthusiasm for value investing has dimmed. "The cruel logic of being a value manager is that at the very time when your opportunities are at their best, your credibility with clients is at its lowest ebb," he said in an email and he was spot on. And while he added that over the next five to 10 years, most value stocks seem priced to have a "decent real return," that will hardly impress clients who demand returns now and certainly have no patience to wait another 10 years.

"GMO has experienced periods like the present before," he said adding that the firm is confident in its current positioning. And while we don't doubt that Inker is confident, a few more quarters of multi-billion redemptions and the fund will no longer have capital to allocate to its convictions, a potentially terminal state which has befallen so many other experienced investors in a time when just buying call options on the dumbest momo names has been the winning strategy courtesy of the Fed.

Yet maybe GMO will have the last laugh.

As noted above, the 82-year-old Grantham is famous for being ahead of his peers. He exited Japan in 1987, called the tech bubble and saw signs of the housing crisis in 2006. Even as clients have left the firm - total assets have declined to $60 billion - GMO has expanded its fixed-income lineup, attracted investors with its factor-based strategy and started a climate change fund.

Alas for Grantham, more investors are leaving then joining. Last week, the Sonoma County Employees’ Retirement Association affirmed a decision to pull $140 million from one of the firm’s global asset allocation strategies, ending a 15-year relationship with GMO according to Bloomberg. The strategy hadn’t beaten its benchmark for more than six years.

The Benchmark-Free fund and some of the firm’s other asset allocation strategies have “underperformed for a long time,” said Bobby Blue, a Morningstar Inc. analyst. "It’s tough to stomach."

Sadly with Treasury Secretary Yellen set to unleash a monetary Kraken and buy stocks outright the next time there is a 20% drop in stocks, the underperformance by value funds such as GMO - which bet on logical, rational and reasonable fundamental investment theses which is impossible in a world where central banks have taken over capital markets - will continue for a long, long time.