Most people consider gold to be a defensive hedge. While it can be at times, it’s more of a risk hedge than anything. Over the long-term, its correlation with equities is virtually zero, which means it’s an asset class that really does its own thing. When we see a sharp increase in gold prices, however, that’s when I think investors are using gold for defense.

Generally speaking, the dollar rises when interest rates are rising. As investments in dollar-denominated securities look more attractive because they’re paying comparatively higher yields, the dollar index tends to drift higher with it. We’ve obviously seen that recently because persistent inflation has kept Treasury yields. Bond yields also rise because stocks look more attractive and investors sell off their bond positions. Whichever of the reason, a strong dollar is generally a positive sign for U.S. risk assets.

While gold has zero correlation with stocks over the long-term, it historically has a negative correlation with the dollar. If a strong dollar is considered a bullish sign, it would make sense that there’s a lower demand for gold at the same time.

So what happens when gold and the dollar are moving higher at the same time when they traditionally have a negative correlation to each other?

As it turns out, usually nothing good.

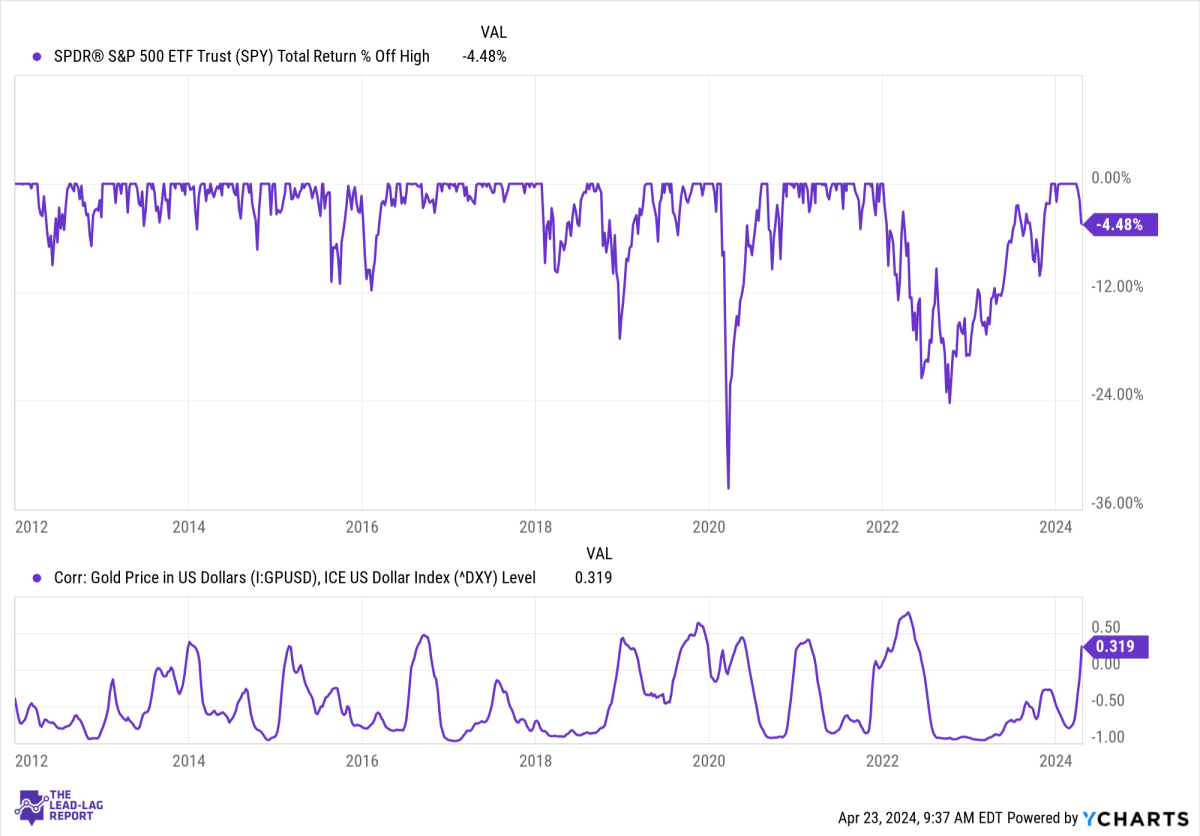

To lay a little groundwork for this discussion, let’s look at a chart of the gold/dollar correlation overlaid with drawdowns of the S&P 500. Even with a quick look at the chart, you can see a pretty explicit trend.

Before we dive into the details of this, let’s first try to answer the question of why this would occur.

When gold rallies steadily, it tends to be part of a flight to safety trade. In other words, it can regularly move up or down without trend, but when it moves decisively and consistently in one direction or the other, it’s usually for a specific reason.

The dollar also has flight to safety qualities. The dollar is the global reserve currency and traders tend to flock to it (or at least overweight it) in times of uncertainty. I’m not sure if global sentiment is necessarily risk-off at the moment, but the U.S. economy is pretty clearly in better shape than almost anywhere else. Higher than average economic growth will also attract dollar-linked investments and that’s probably also helping the case.

In short, I believe gold is acting as a risk-off asset right now and the dollar is acting sort of as a risk-off asset. But we can unquestionably say that their correlation has turned decidedly positive as we can see with the chart above.

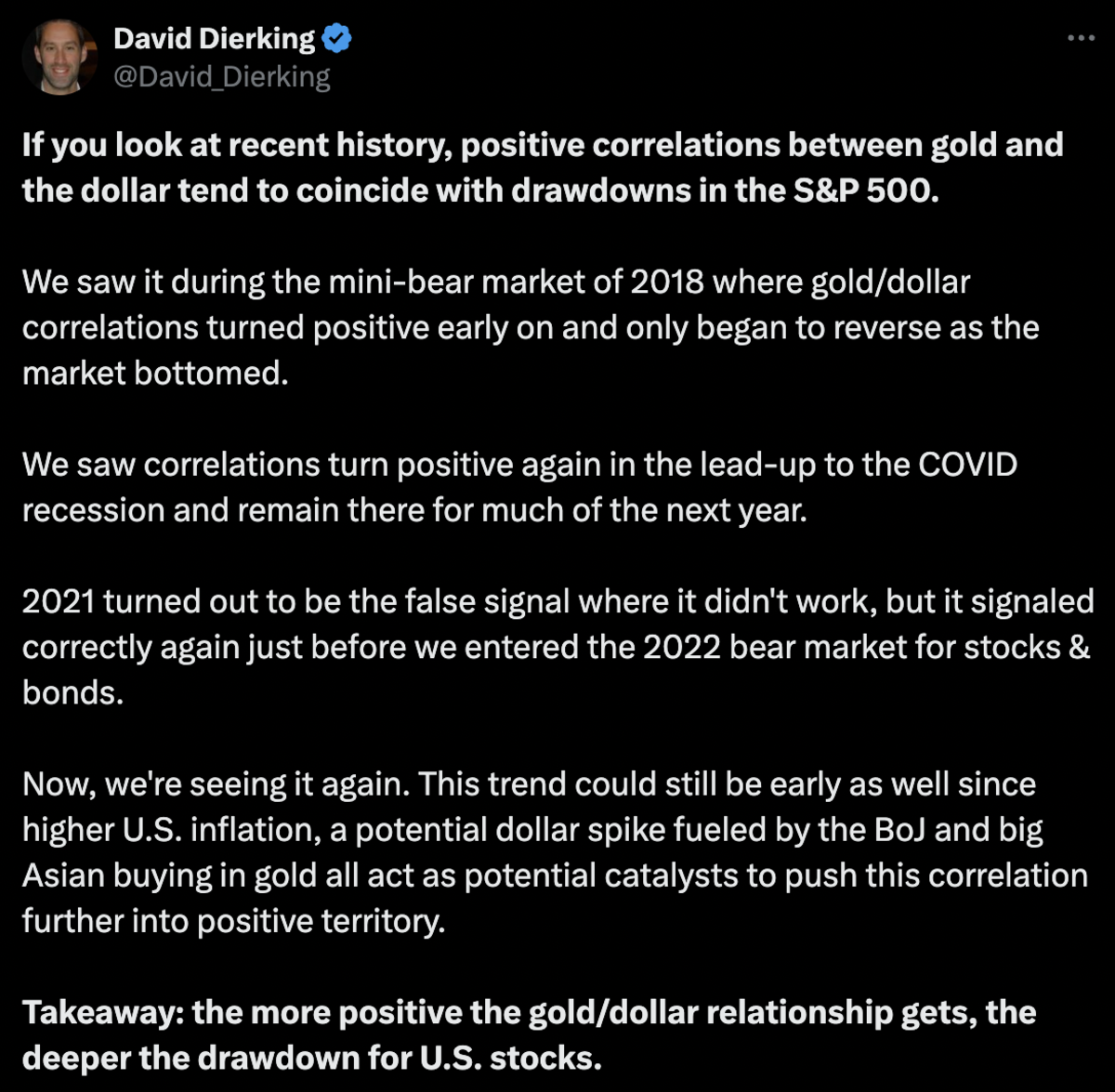

As I posted on Twitter, here’s what we know about the gold/dollar relationship when correlation turns positive.

The takeaway is the most important thing here. The higher the correlation between gold and the dollar, the deeper the S&P 500 correction tends to be.

The two times that the gold/dollar correlation went above 0.50 in recent years was just before the COVID recession and during the 2022 stock/bond bear market, the two deepest drawdowns since the financial crisis. The correlation nearly hit 0.5 in late 2018 and coincided with a 20% drawdown in the S&P 500.

As I mentioned in the Twitter post, 2021 was the outlier, but that might have been a function of conditions at the time. This was around the time that inflation really started taking off and investors were likely getting very nervous about the potential consequences. At the same time, the economy was getting flooded with liquidity & stimulus cash and that prevented the big drawdown in equities that probably should have happened during that time.

In summary, the dollar/gold relationship correctly signaled deteriorating conditions, but the government stepped in to save risk assets.

The current dollar/gold correlation has already shot up to 0.32 and it’s probably moving higher before all is said and done. As it stands right now, the S&P 500 (SPY) is only about 4% off of its all-time high.

If the correlation gets above 0.40, we’re in danger territory where 10% corrections become more likely than not. When the correlation gets above 0.50, we usually run the risk of a 20%+ correction. Again, we’re already at 0.32 and sharply trending higher.

Does that mean a further correction is imminent? Not necessarily. 2021 demonstrated that, but a high correlation between gold and the dollar tends to mean bad things more often than not. Final Thoughts

The U.S. equity market has experienced only a modest pullback thus far, but it looks like it could potentially get much worse. All of the catalysts are there too - no rate cuts coming, inflation re-accelerating, consumer credit issues coming to a head, Japan at risk.

Even if you use 2021 as the reasoning for believing that things might be different this time, remember that that market was characterized by huge liquidity in the system. We’ll be seeing the opposite of that this time around, which furthers my conviction that this time will not be the exception.

I firmly believe that we’re at high risk right now of a deeper drawdown ahead.