On Monday I indicated that it was time to lighten up long positions in preparation for a downdraft. Since then the XJO has lost 2.4% and may be the beginning of further falls ahead especially if the S&P500 closes below 2800 tonight (this is the real test).

Those who followed this thread would have noted my opinion that our ASX would always be lagging the US market indices for reasons I mentioned in my post on 1 May. One major factor is that we do not have the monsters of tech stocks that the US have - and our tech stocks are in no comparison whatsoever (they are not global market leaders by any measure). The other is that US market is flooded with liquidity at least in the short term and their companies do more share buybacks and we are more conservative when it comes to valuation.

So for all the upside potential the US markets have, we do not have the same attributes that can ensure our local market can positively correlate in direct proportion. However, we have the same or worse correlation if and when US market falls. What the, right?

Right now, the risk-reward for our local market is not good and I outlined below why it is so

(1) Technically XJO has moved down below MA50 today and MACD looking to turn down as well (confirmation tomorrow) (and we are just slightly below 3% move to break the all important 5200 support, which if broken marks the end of range bound sideways trade since 6 April, yes we barely moved on the XJO since then although we enjoyed broader market gains thank you very much)

(2) Market is vulnerable to profit taking on stocks that have made very notable recent gains, including APT and WAAX stocks

(3) Bank stocks are vulnerable to extended selling as the XLF (US financials) has broken down its channel and starting to look bad

(Note that Wells Fargo hit a 52 week low yesterday , yes lower than when it was on March 23, the index only masked it because the monsters of tech is up 8% YTD), with NZ contemplating negative interest rates early next year, will Australia follow suit? And that means more pressure on bank margins

(4) Prevailing uncertainties in relation to future China actions on trade with Australia that could potentially have far reaching impacts across a broad sector of industries, hopefully it does not get so bad and that it shall pass (but everytime we open our

mouth it makes it more unlikely for it to pass, even if we do not see immediate ramification, we would never know until we see the real numbers a number of quarters after the virus has subsided but the uncertainty stays and markets dont like

uncertainty). US Bill to impose sanctions on China would also play a part in this strained relationship as we are lumped under

the US bucket

(5) Now Norwegian Sovereign Wealth Fund is considering dumping BHP because of its exposure to thermal coal

(6) Local market saw what the shutdown did to our unemployment numbers and despite our re-opening efforts, it is still wary

of a possible second wave happening here - what has happened in Wuhan recently which now mandates a test of all Wuhan

citizens is telling us how intractable this pandemic issue is and that it is too early to celebrate

(7) Our Government's desire to wind back Jobseeker and possibly also Jobkeeper is ending the "honeymoon" period for all

struggling individuals and entities and unfortunately the pain will start to bite. Expect to hear more companies getting into liquidation which would not help market sentiment.

(8) We have yet to fully understand the full impact of the COVID pandemic on ASX listed company earnings. And we have more

like shrugging off recent revelations e.g 60% drop in Cochlear's April sales announced on Monday didnt even dent its share

price until today. In time to come, when exuberance starts to wane, more people would be asking the very question they

should have asked themselves before they bought "how is it that the share price is barely below their 2019 prices when their

earnings have dropped rather sharply and the future outlook is no better, did I pay too much for the shares?" . In such times,

I'd rather hold shares that are not expected to deliver any profits than those considered safe with high expectations (hint:

CSL)

...and that does not even include a full raft of risks coming from external, all suggesting that the risk potential outweighs the reward potential which increases the probability that we are about to end the range bound sideways market to something lower.

The Stock Market Sell-Off May Only Be Starting

|May 13, 2020 1:32 PM ET

Mott Capital Management

Reading The Markets

Using fundamentals, technical charts, and options to find the next move

Summary

Yesterday, an investment firm made several large block trades to unload ETFs.

There also were a number of massive bearish bets placed on the SPY ETF.

Meanwhile, the market is grossly overvalued.

It seems somebody wanted out of the stock market very severely yesterday, triggering a late-day plunge in stocks. Yesterday around 1 p.m. across several large ETFs there was a massive sell program that appears to have taken place with millions of shares trading in a short period. These trades were made, it seems, as block trades, and as these ETFs reacted to the trades, it forced selling across the stocks that were held in their baskets.

If that wasn't enough, there was a significant amount of put buying yesterday in the SPDR S&P 500 Trust ETF (SPY). This activity suggests that traders are betting the ETF falls sharply over the next two months. Additionally, earnings estimates for the S&P 500 continue to plunge, making the valuation for the market even more stretched.

Block Trades

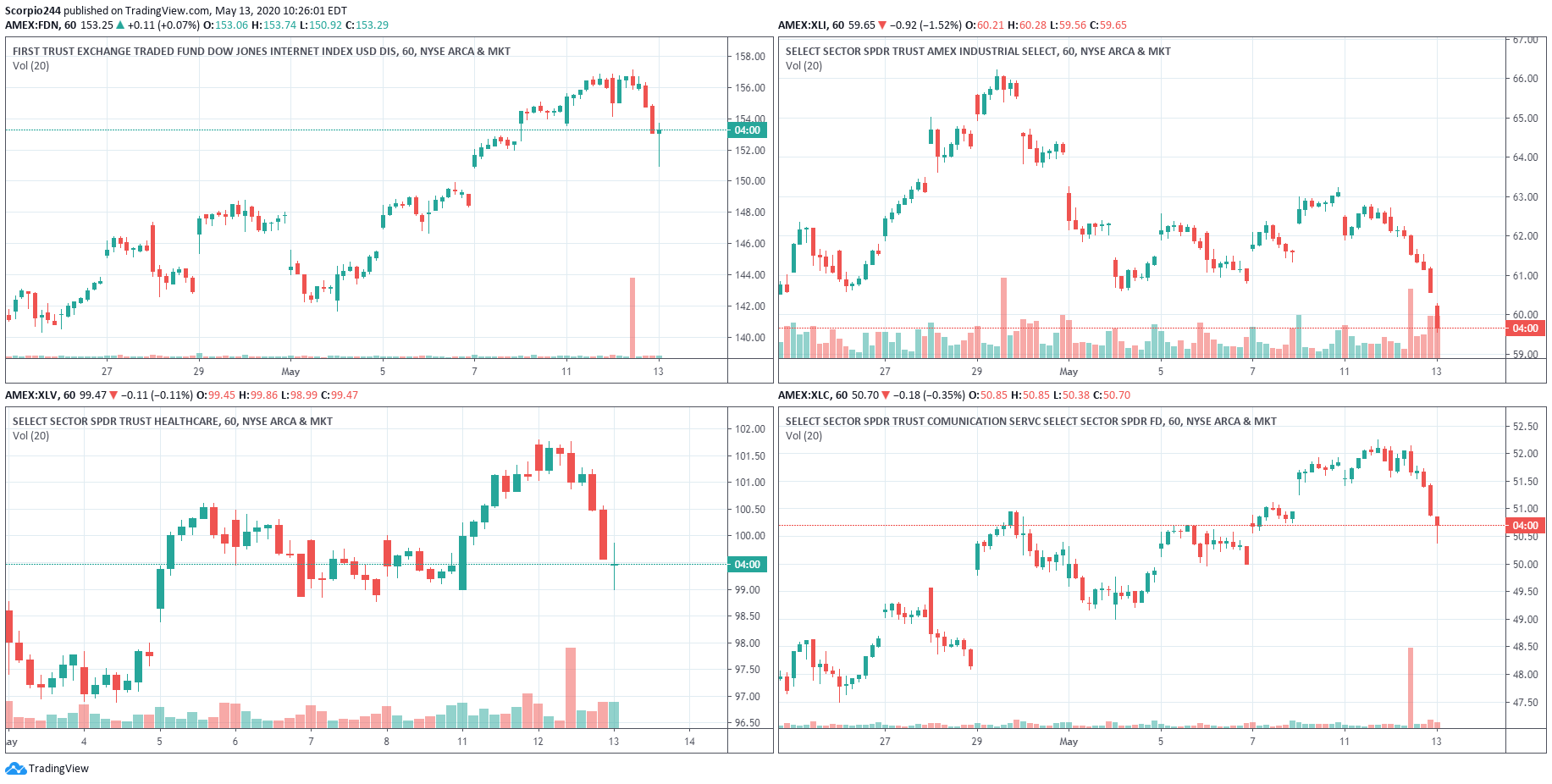

The chart below shows four of the ETFs, the First Trust DJ Internet ETF (FDN), the Industrial Select Sector SPDR ETF (XLI), the Health Care Select Sect SPDR ETF (XLV), and the Communication Services Select Sector SPDR Fund (XLC). It's safe to say it's reasonably visible, given the massive volume spike. The sizes were enormous. The FDN traded a block of about 4.1 million shares, the XLV traded a block of about 7.6 million shares, the XLC about 10.1 million shares, and XLI about 4.1 million shares.

The trades did help start a cascading effect of pushing the ETFs lower throughout the balance of the day.

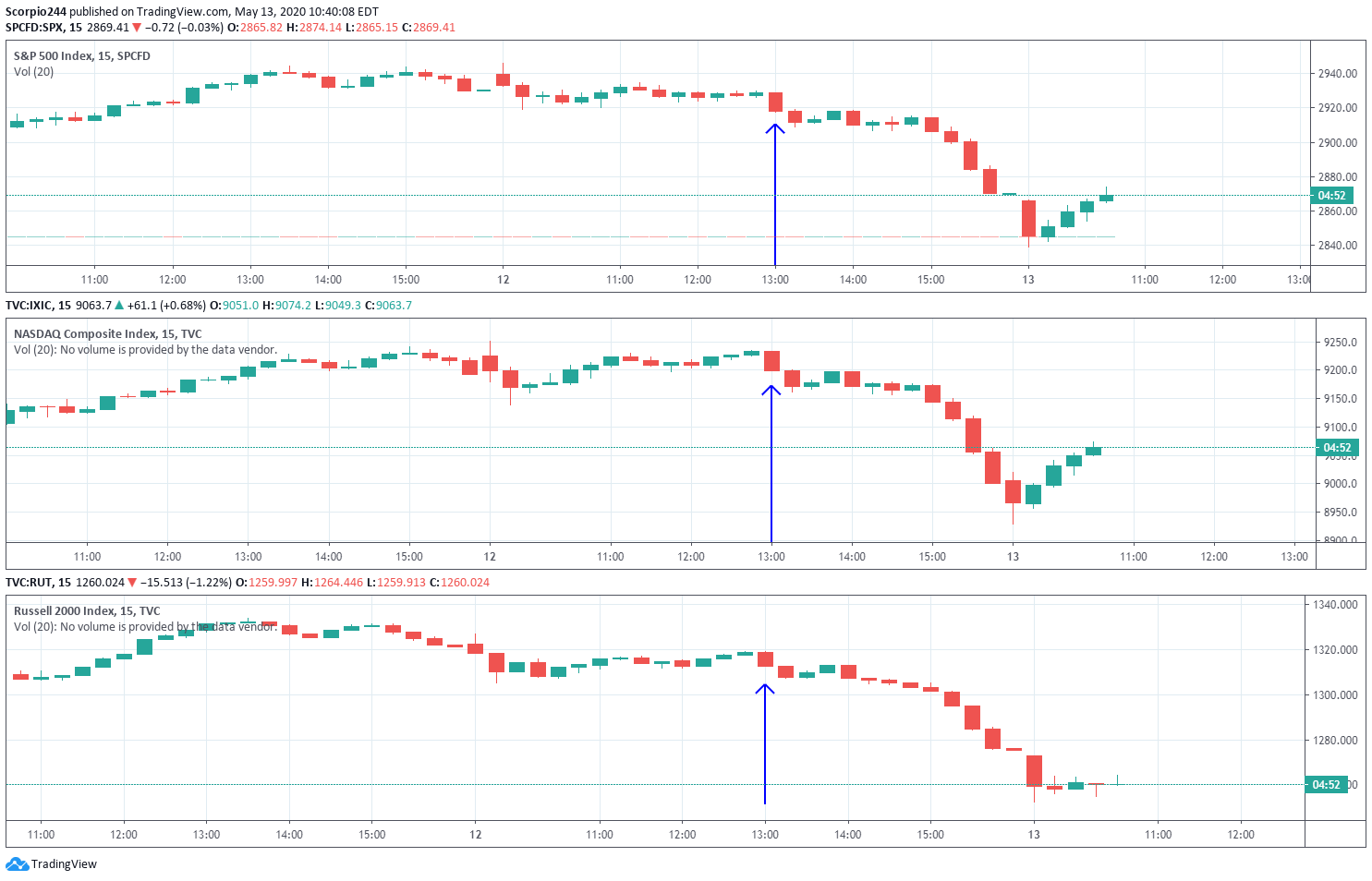

The next chart shows the sharp turn lower that followed starting at the 1 p.m. time on the charts for the S&P 500, Nasdaq, and Russell 2000.

The trades could have been made for any number or type of investment firm that simply wanted to get out of these holdings, and completed the block trades with an ETF desk at a sell-side firm that can do the creation or deletions of ETFs. That would seem to be the quickest and easiest way for an investment firm to move positions of this size quickly. At least, that's how I would have done it if I was still a trader on a buy-side desk. In this case, there's no buyer of the block, because the sell-side desk simply hedges away the risk of taking on the block by going short the same basket, which is something we talked about in my morning commentary among my Marketplace readers.

Earnings Collapsing

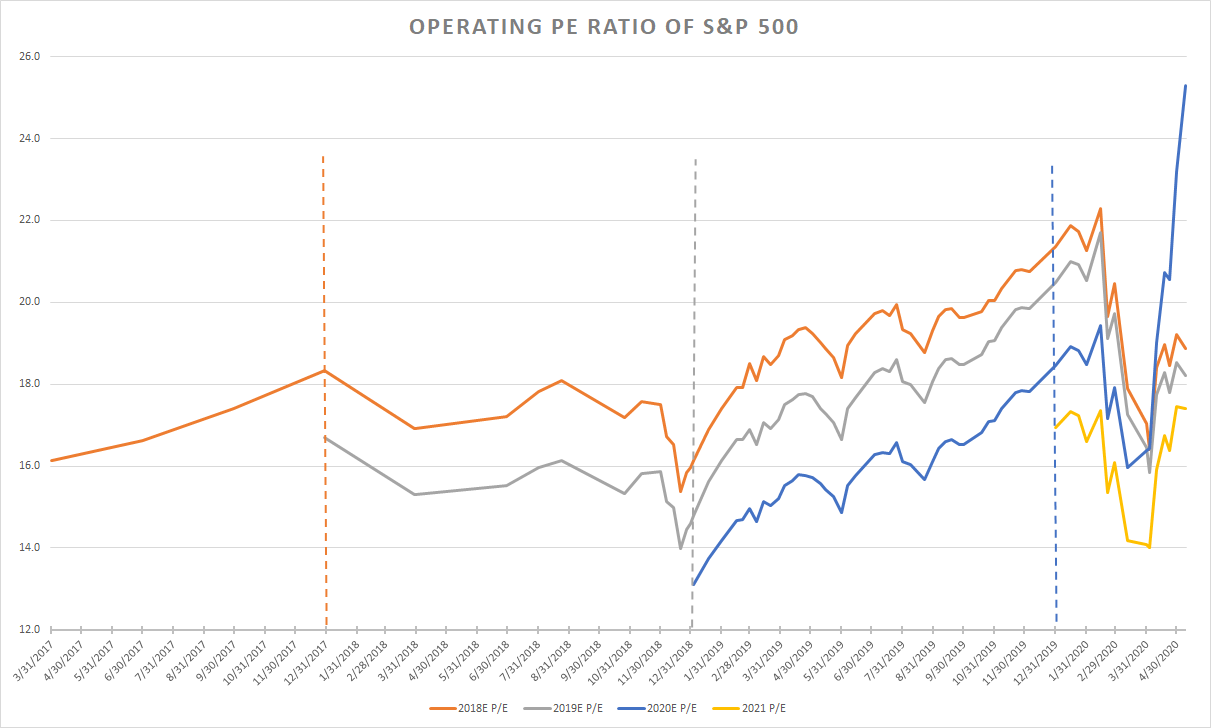

The latest data from S&P Dow Jones now shows that earnings are expected to fall in 2020 to by 28% to $113 per share from 2019's roughly $157 per share. That's down from $175.65 per share on Dec. 31, a drop of more than 35%. It leaves the index trading for a stunning 25.3 times 2020 earnings estimates. By far, the highest forward PE ratio in years.

(DATA COMPILED FROM S&P DOW JONES)

Additionally, earnings estimates for 2021 now stand at $164.20 per share, which would be an increase of about 45.3% from 2020 estimates. However, estimates for 2021 also are down sharply from their Dec. 31 peak of $191.22, a drop of more than 14%. It leaves the S&P 500 trading at 17.4 times 2021 earnings estimates. It makes the index more expensive today than where it stood on Feb. 14 before the coronavirus swept across the developed world.

(DATA COMPILED FROM S&P DOW JONES)

More amazing is that index today is trading for just about the same valuation on a one-year forward PE basis as it did at the end of last year when many people were screaming about how overvalued the market was.

Bearish Betting

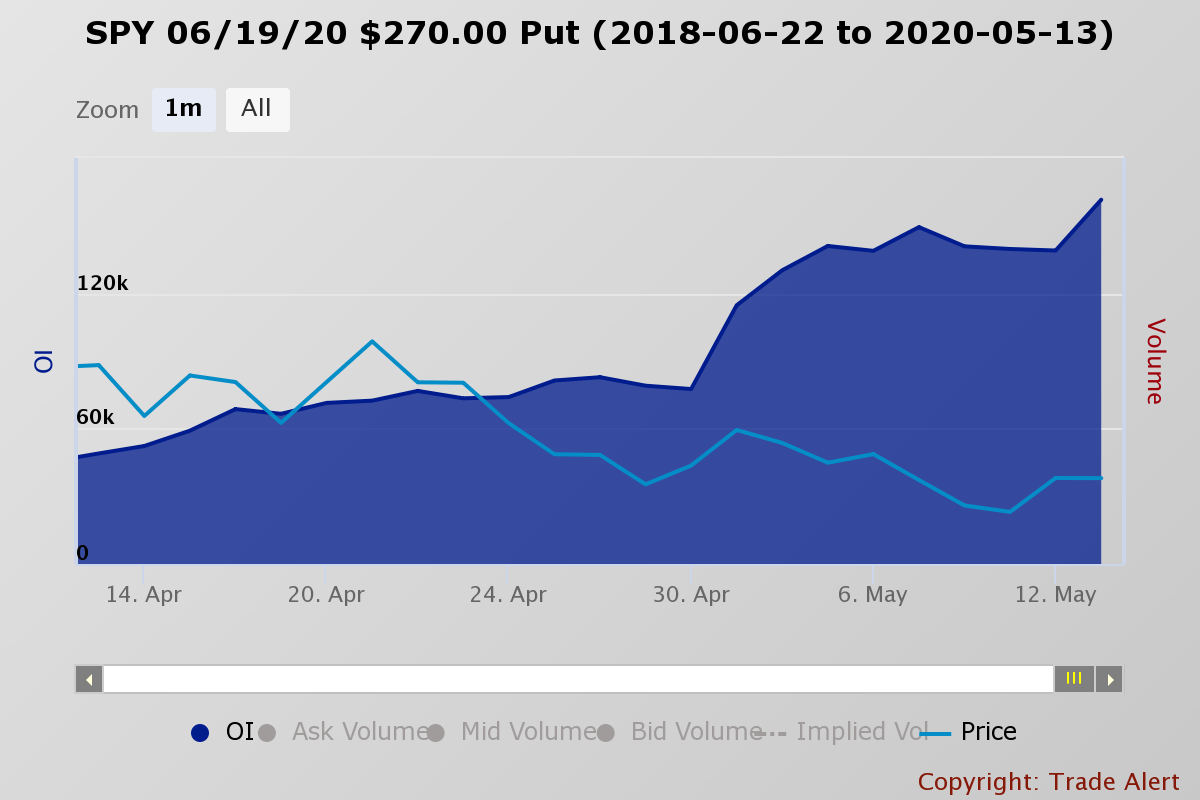

Even worse are the massively bearish bets placed on the S&P 500 ETF yesterday. For expiration on June 19, open interest levels at the $270 puts increased by 22,505 contracts. These contracts traded on the ASK and were bought for about $3.75 per contract. It means the SPY needs to fall to $266.25 or roughly 6.5% to start earning a profit.

Meanwhile, the SPY $270 puts for expiration on July 17 increased by 26,553. The puts also traded on the ASK for about $9 per contract, and that means they were bought. It suggests that the ETF has to fall to $261 or 8.5% for the buyer of these puts to earn a profit. It's a huge bet as well, with the premium paid of nearly $23.9 million.

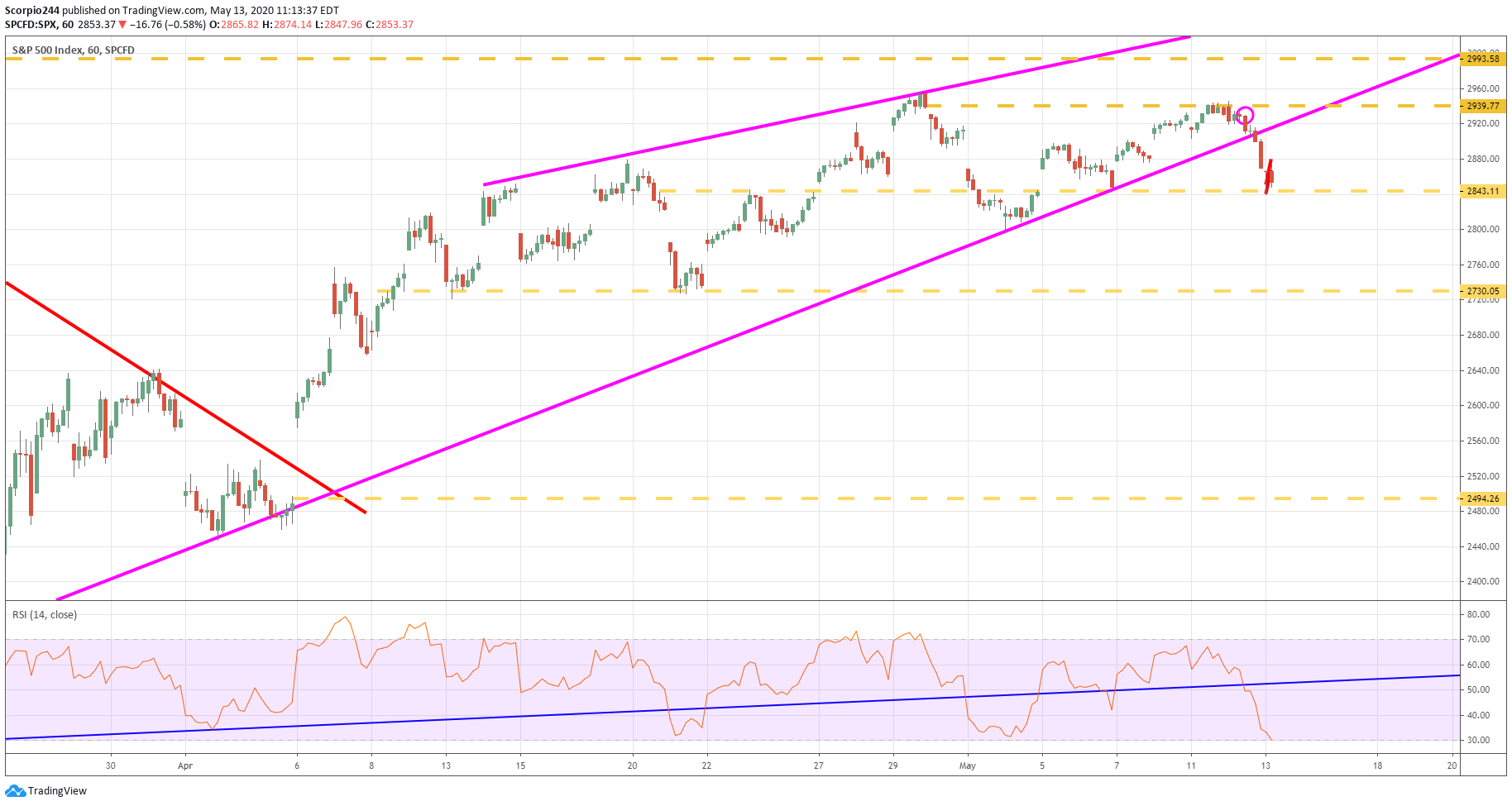

Technicals Breaking Down

If that wasn't enough for you, there is, of course, the technical charts breaking down, with the index now clearly below the lower bound of what appears to be a rising wedge pattern. A drop below technical support would open up a further decline in the index to around 2,730, and potentially for a fall back to 2,495. At 2,495, there's a substantial technical gap that resides from a sharp move higher on April 6.

Risks

There are, of course, plenty of risks here, with most of them surrounding an improvement in the outlook for the economy. Should reopening go better than expected, it seems possible that S&P 500 earnings have fallen too far, and are likely to begin rising again. That could make the market's valuation more attractive. Additionally, should the index manage to hold support at 2,840, then it could quickly snap back to its recent highs around 2,940.

At this point, as I have been saying since the start of April, the risks to this market have not been the fear of missing out, but the chances for a giant pullback, based on horrible valuations and a deteriorating economy. It seems we are now on the very cusp of that enormous pullback I have been suggesting was likely to come.

-Mike

On Monday I indicated that it was time to lighten up long...

Featured News

Featured News

The Watchlist

VMM

VIRIDIS MINING AND MINERALS LIMITED

Rafael Moreno, CEO

Rafael Moreno

CEO

SPONSORED BY The Market Online