...you read it, the Supreme Court has overruled state's authority to ban Trump from the ballots.

...Biden's incompetency to even put crooked Trump behind bars speaks volume.

...the Dems would soon be forced to implement Plan B.

...the Trump threat is gradually factored by the market well before the election day ...listen up Chinese stocks, lithium, green investments, AUD.

-----------------

This is from David Llewellyn-Smith:

As we head deeper into the year, it’s time we consider the implications for the AUD of the US election.

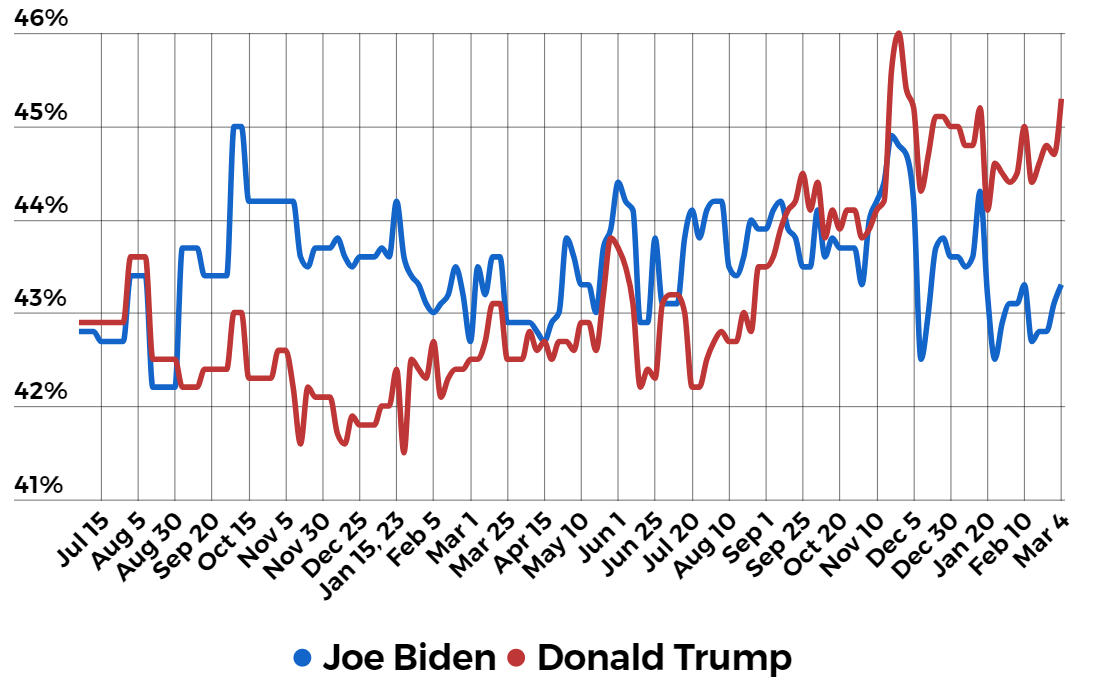

Polling has Donald Trump favourite:

At this stage I would take that with grain of salt. But after last week’s Supreme Court decision to hear the immunity case, the odds are firming that Trump will at least make it to polling day.

While that possibility firms, market will have discount his policies, which are very DXY bullish and AUD bearish.

Most notably, a 60% Chinese tariff and border closure of some type with Mexico.

There are many uncertainties at this juncture. The court cases against Trump and Biden’s brain are just two. So, I don’t expect DXY to go tearing away.

As well, we still have Fed easing ahead, and a bounce in global industrial production coming, both of which will weigh against DXY.

But the election is already DXY bullish at the margin, and any firming in the odds of a return to Trump will push that further, faster.

Trump’s platform will do material harm to China and is equally inflationary for the US.

He is an outright AUD destroyer.

...you read it, the Supreme Court has overruled state's...

Featured News

Featured News

The Watchlist

NUZ

NEURIZON THERAPEUTICS LIMITED

Dr Michael Thurn, CEO & MD

Dr Michael Thurn

CEO & MD

SPONSORED BY The Market Online