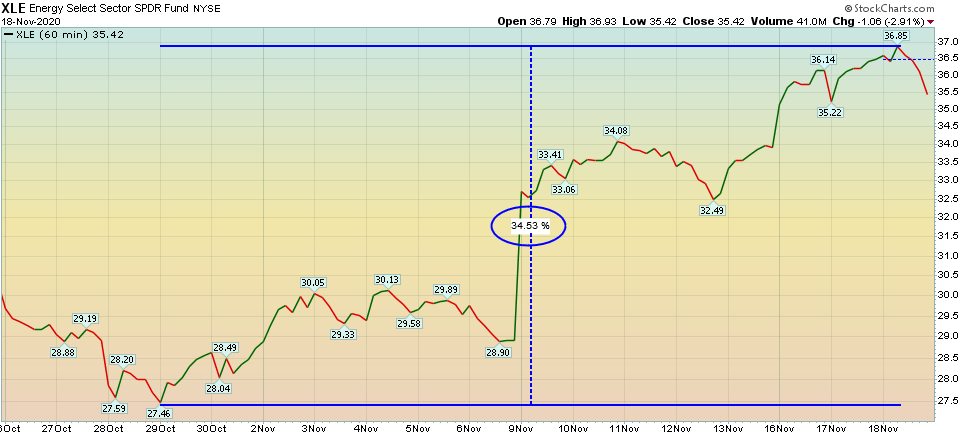

The Rotation is Real Energy up 34.5% since October 29, 2020.

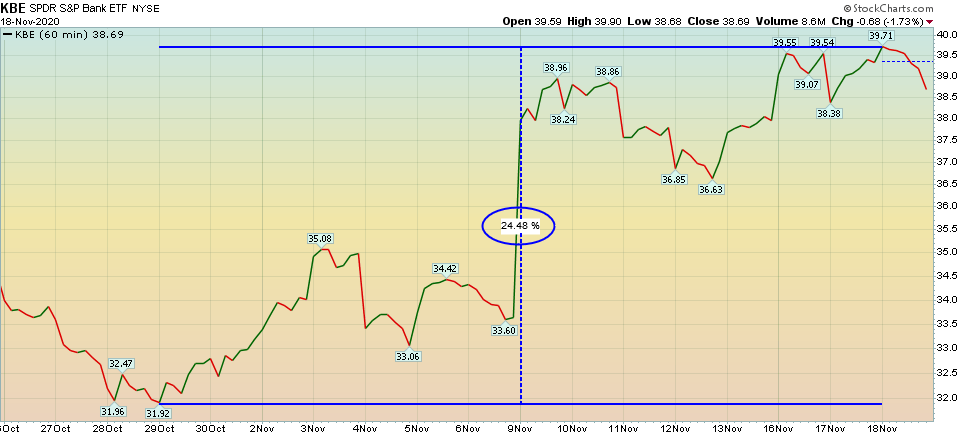

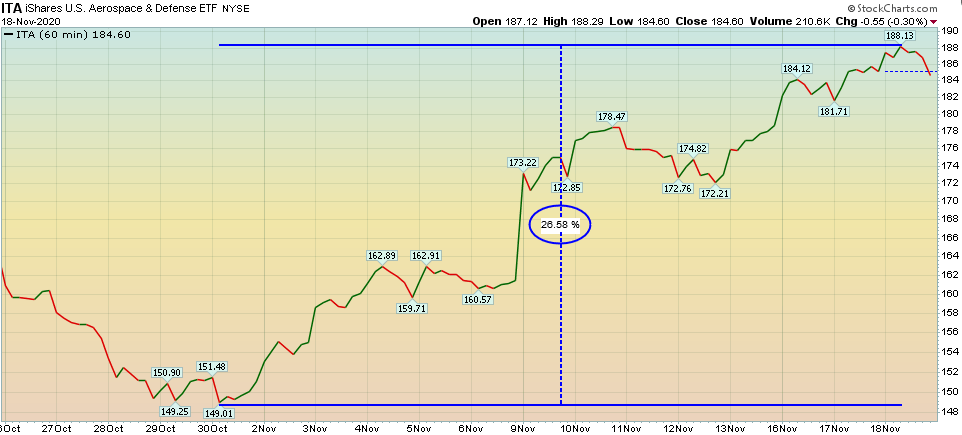

Banks up 24.5% since October 29, 2020. Defense Stocks up 26.5% since October 30, 2020.

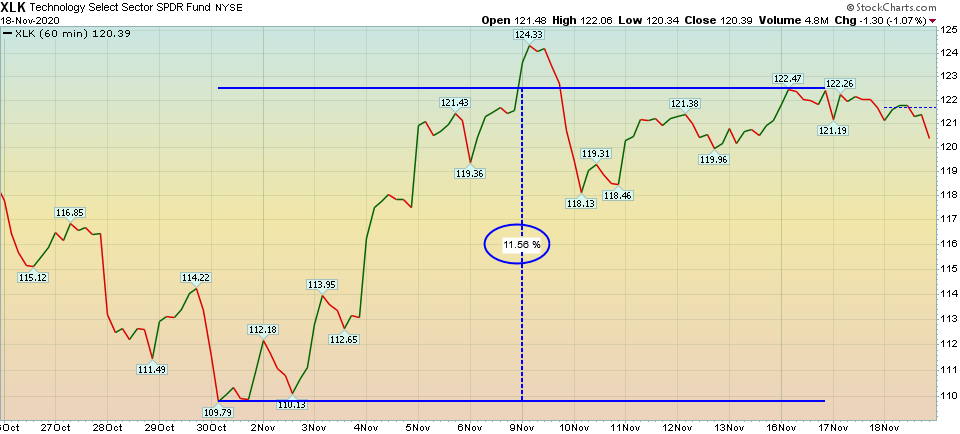

COMPARE THAT TO TECH WHICH IS UP LESS THAN HALF AS MUCH: Tech Stocks up 11.5% since October 30, 2020.

The announcement of the Pfizer/BioNtech/Moderna vaccine data last week and this week was a game changer. Cyclicals took the lead with Energy having its best week EVER, and Value out-performing growth by its widest margin since 2001.

Banks came in hot and will be a major contributor to UPWARD EARNINGS REVISIONS in 2021 as the big 4 money-center banks are over-reserved by >$20B – which will come back as earnings in future quarters. There are now $110B of reserves for the banking sector that were taken in Q1/Q2 (due to COVID). It is likely that ~half will come back as earnings power – that is not priced in at present. These reserves were taken in Q1/Q2 when people were expecting 20% unemployment. We are now at 6.9%.

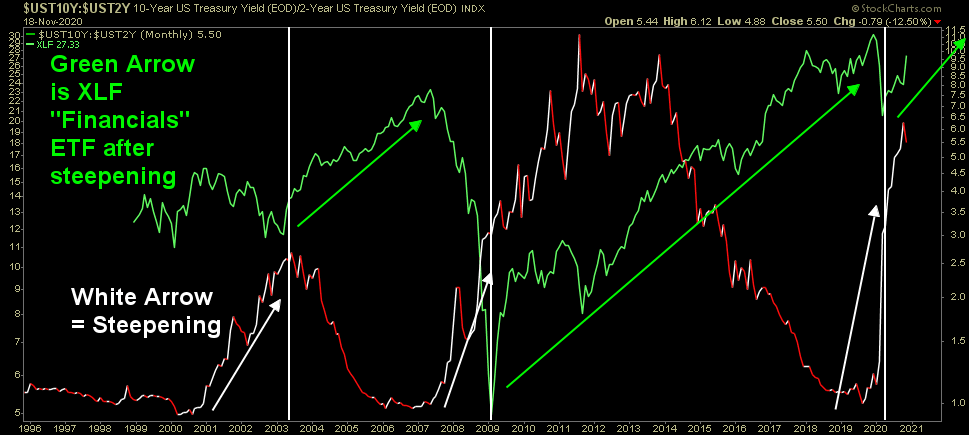

The other factor that will help banks is the yield curve steepening – helping NIM (net interest margin):

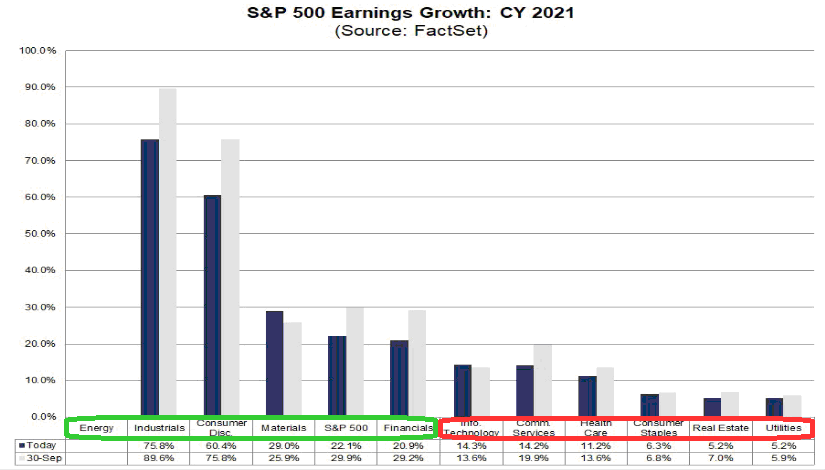

The move into cyclicals is consistent with 2021 Earnings Estimates. Cyclical sectors (Energy, Industrials, Materials, Financials) will have the highest earnings growth off of low bases, whereas, tech/communication services pulled forward meaningful earnings in 2020 and will lag the S&P earnings growth rate in 2021:

2 Additional Tailwinds for Cyclical Stocks:

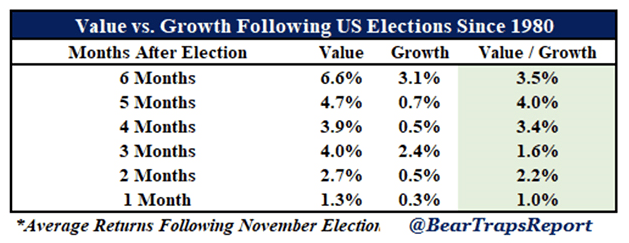

Value historically outperforms Growth in first 6 months after Presidential Election.

Cyclicals historically outperform in first ~8 Quarters of new business cycle (which we just started in Q3 after 2 quarters of negative GDP growth – Q1/Q2). You can review the analysis here:

Earnings:

-With 92% of the S&P having reported Q3 results, 84% beat EPS (highest % in over a decade). 78% beat on revenues.

-2021 EPS estimates continue to revise UPWARD with consensus now at $168.38 (as of Friday). This may be too low for 3 reasons:

Increasing NIM/Reserve Releases for Banks.

Un-grounding of Boeing 737Max (coupled with increase air travel demand due to vaccine) could have a material impact on earnings. China domestic air travel exceeded the previous year for October 2020. They are 2-3 months ahead of us in recovery. Review China data from last week’s note here:

3. Getting a vaccine this quickly was not priced into estimates. There is global pent-up demand that will be realized once people feel safe. Potential Short-Term Headwinds/Chop:

1) Retail Investor Sentiment is running a bit hot in the short term – as we discussed in last week’s note above. Institutional sentiment is getting somewhat aggressive as well (we will discuss below).

2) Cases are elevated and vaccinations will not start for weeks. This may lead to regional restrictions and shutdowns – which would impair growth in the short term (although they seem to be peaking – just as schools are deciding to shut down):

The key question is whether market will look through this… Intermediate Term Outlook Positive:

While the “easy money” has been made in the general indices (since the March lows) – in the short term, I think the “easy money” is just getting started in “left for dead” sectors/stocks (Cyclicals/Value). We believe Banks, Defense Stocks and pockets of Energy will be as good – if not “orders of magnitude” better – than buying the general market in late March. Here are the 7 key catalysts:

Vaccine (PFE)/Treatments (LLY/REGN/GILD) are finally here or nearly here.

Political Gridlock is good. Corporate tax rate stays at 21%.

Uncertainty with policy/trade should diminish in coming months.

5-6%+ GDP growth in 2021 – lagged effect of ~25% M2 money supply growth yoy.

Accomodative Fed. Short end will stay pinned at 0-25bps. Long end will expand – steepening the curve (good for banks/credit expansion).

Stimulus: $500B-$2T within the next few months.

With economic growth coming back (>5-6% GDP in 2021), managers will have many options where they can find earnings growth (economically sensitive/cyclical stocks). This contrasts to 2020 where managers loaded into a narrow group of stocks that could provide earnings growth in a slow economy – thereby bidding up the multiples.

Earnings multiples on 2020’s “stay at home”/Tech/SAAS stocks will start to moderate as money flows into economically sensitive sectors that will resume growth in 2021.

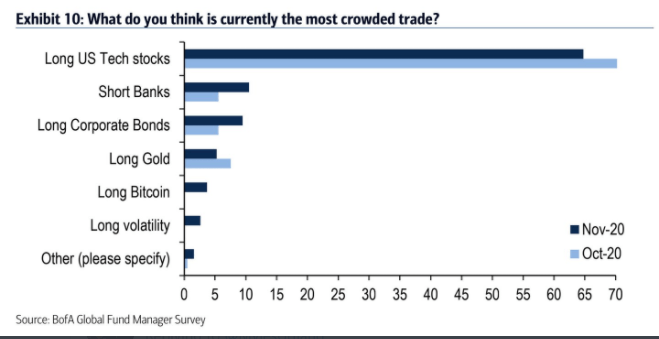

Institutional Sentiment

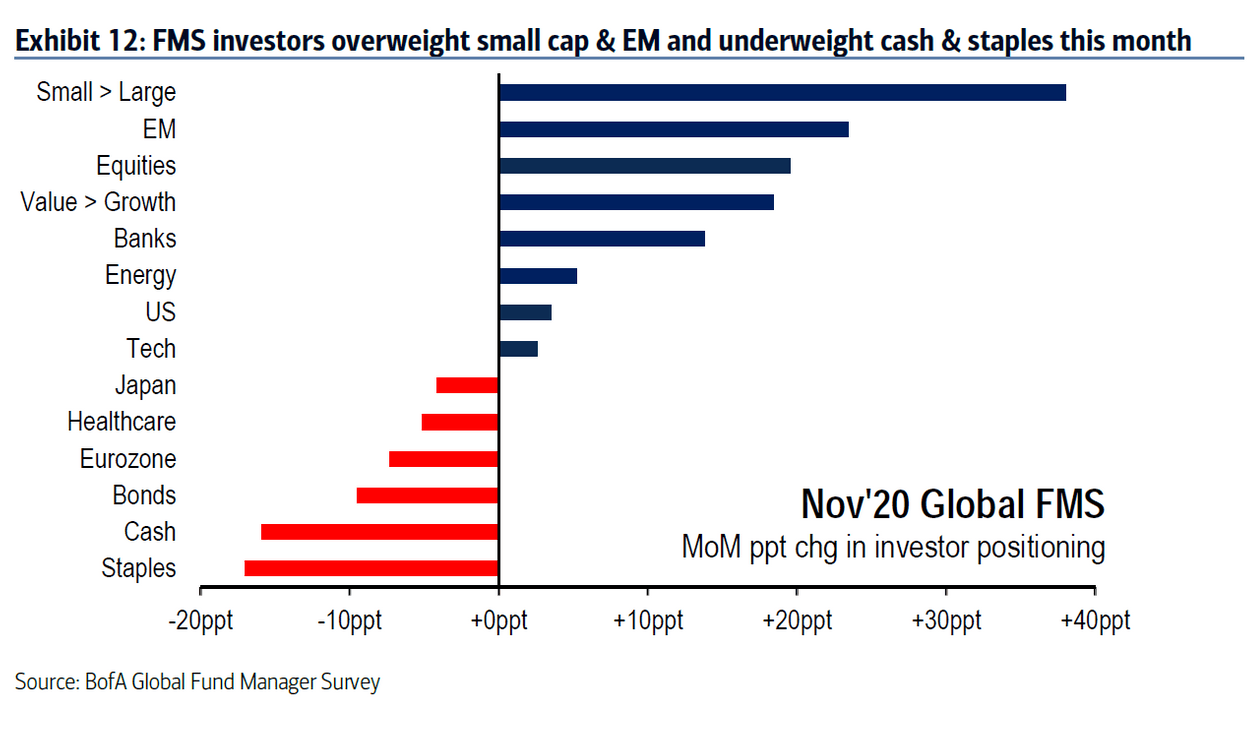

This week, Bank of America published its monthly “Global Fund Manager Survey.” We put out a summary of the key points which you can review here:

The key takeaway is that managers went from flatfooted before the election, to near exuberant as of last week. So we have to balance the fact that most managers still have to chase year end performance – while at the same time recognizing that many indicators are nearing extremes.

My sense is that because most market participants are now cognizant of the near euphoria – and missed the aggressive post-election bounce, the “pain trade” may still be up into year end. The caveat is to pick your spots. As we said to conclude last week’s note, we believe the easy money off the march lows has been made in the indices. However, the easy money may be JUST GETTING STARTED in the cyclical stocks/sectors we discussed in recent weeks.

Institutional money JUST started to move in our direction this month, but because they are steering tankers, it will be a long upward trend that takes time and lasts for many quarters. The change in this month’s survey was pronounced. Like we always say, “opinion follows trend.” Come on in, the water’s warm… what took you so long?

This month’s survey interviewed 190 Managers overseeing ~$526B AUM. Here are the key points:

Net 24% of surveyed investors expect value stocks will outperform growth stocks, highest since February 2019.

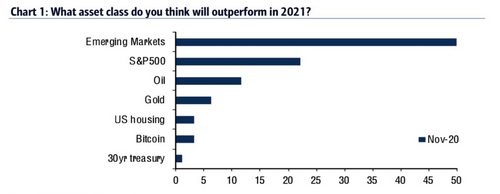

Assets that investors expect to outperform next year: emerging markets, S&P 500 and oil.

Rotation to Emerging Markets, small cap, value, banks funded by lower allocation to cash bonds, staples.