You could look to short wheat (after we hopefully get another leg up to previously identified resistances) and go long corn effectively just playing the spread. What this spread represents is a short-medium term bet on the rise of animal protein consumption certainly in Asia, because as you correctly identify that raises demand significantly for feed grains. The higher wheat goes the safer your (educated) bet. I think that is why spreads appeal to sophisticates. Significantly reduces the irrational risk out of the bet if you like because over time the laws of human needs do not deviate from the mean for an extended period. If they do the bet is safer to get back to the norm.

However for now, the premium of wheat over feed grains will move acres to wheat (generally high productivity acres with irrigation capacity as opposed to lower yielding dryland). A significant component of the global feed grain complex by volume can be barley (but largely comprised of corn) and with limited forward pricing opportunities for barley that correlate acceptably, the inability to contract profitability can easily attract acres to wheat over barley. The only futures contract for a feed barley is in Winnipeg. Hedging wheat is a pleasure these days, so many different products available some carrying no production risk at all (is non delivereable like SWAPS). And we can go out 3 years if we want. Wheat is around $300/t atm whereas barley is $220-250 depending on if you can make malting grade. Barley is popular in Canada, Argentina and the whole of Europe, and of course Australia.

You can also get acres moving to wheat if there is weakness in the softs particularly cotton and this land is high productivity if they choose to sow wheat. It is not uncommon to see a cotton price spike after a significant wheat price spike because farmers do respond to pricing signals, particularly in high productivity environments. For a cotton farmer wheat is low cost, cotton is high cost so good wheat prices are a no brainer. We definately saw that in 2007-08 when wheat went to around 1350, and cotton followed later because of the deficit caused by the massive acre shift globally to wheat.

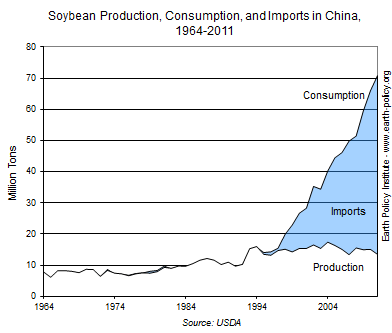

I see hints of an oilseed deficit building too with comparatively strong wheat prices. One to watch for 2014-15. Rationale for this is Chinese demand. Oilseeds are the most water intensive crops to produce and for a country like China which is a massive grain producer in its own right with constrained water and land resources, it makes sense to import the most water/land intensive and calorifically rich commodities like soybeans, canola and palm oil and dedicate local agricultural capacity to cereal grains like corn and wheat. In effect import water credits. Water intensive crops grown where water is not as valuable - ie big ag with few people (eg Brazilian cerado, Argentinian pampas, US midwest). 1t of soy gets you 200kg of oil 400kg of protein. 1t corn gets you 240kg of carbohydrates and 180kg of protein. I like particularly prospects for canola because 1t of canola gets you 450kg of oil and 180 kg of protein yet it is only around$500/t atm. If you gotta import something edible from the other side of the world it appeals to make it nutritionally dense. Check out this graph:

And look at oil and protein rich canola.

Have we seen a low in canola? Certainly looks like a higher recent low has been recorded. Big volumes soaking up inventory at these price levels. Next target 520?

On meat/dairy, undeniably demand is going to rise and perceivably that demand may be rationed by supply but I wouldn't comfortably bet on that generating bankable profits for an investor like you and me. This is not a favourable development for the earth's resources from a central planning perspective as the grain larder is already showing signs of struggling to cope with current demand, so government policy appears to be working against this organic growth in appetite for tastier protein. And of course you can have inflating meat prices in the consuming markets whilst having low prices at the point of production with the meats as is currently evident with low 1970s cattle prices in Australia and record high beef prices in wet markets in Indonesian cities. That has been brought about by govt intervention in trade (ie live trade ban in Australia, same effect with export taxes on beef in Argentina-see below).