Company Profile: K2fly (ASX:K2F)

September 21, 2020 |Company Profiles

K2fly is a company that Track Record News reported on 24 August 2020 under the title “successful software entrepreneur with £105m exit, now CEO of fast growing ASX SaaS company.”

This article is a detailed break-down of K2fly (“K2F”) which is listed on the Australian Stock Exchange (ASX) under the tickerK2F.

..Overview/Summary

K2F is one of the fastest organically growing SaaS companies on the ASX (ASX:K2F).

Its Annual Recurring Revenue (ARR) has grown from approximately AUD850k to AUD2.36m in the last 12 months (177% Year on Year (YoY) growth) as at 30 June 2020. The company has achieved this growth while achieving cash flow break-even last quarter and maintaining AUD3m in the bank.

Also, the company’s current Total Contract Value (TCV) has grown a phenomenal 663% YoY (~AUD1m at 30 June 2019 to AUD7.5m at 30 June 2020).

Its SaaS based operational metrics fall in the 75th and 90th percentile when compared to global B2B SaaS companies at its current stage (e.g. Sales and Marketing efficiency (Magic Number), Gross Profit Margin (GPM) and Annual Recurring Revenue (ARR) growth).

K2F’s growth and operational excellence are similar to that of another listed SaaS company, which has seen its value increase by more than 2,000% (20x) in the last 3 months.Track Record reported on 3DP and its operational excellence when it was at 2.4c and since then it has traded as high as 50c. However, it is important to note that their respective Go-To-Market (GTM) strategies, underlying products and business models are completely opposite.

What they do share in common is operational excellence and a capital efficient distribution machine that allows them to grow recurring revenues in a very low cost way. This is what sets them apart from other listed SaaS companies, and is often not understood (until a billionaire technology investor comes along and realises, which was the case with 3DP).

In terms of K2F’s growth trajectory, its ARR is currently growing at 177% Year on Year (YoY), which means it is potentially on track to follow theTriple, Triple, Double, Double, Double(T2D3) path of a unicorn SaaS company.

Lastly, a noteworthy mention to Canary Capital, the lead broker on both 3DP and K2F who has made a name for supporting the best up and coming SaaS and technology companies early.

..Who is behind the management team at K2F?

Brian Miller and Nic Pollock are the CEO and CCO of K2F, respectively. K2F is listed on the Australian Stock Exchange (ASX) under the ticker K2F (ASX:K2F). Both Brian and Nic have track records of successfully building and selling software companies for hundreds of millions of dollars.

Brian was a Co-founder of AMT-Sybex,which was acquired by Capita Plc for £105m in 2014.

AMT-SYBEX is part of Capita plc. AMT-SYBEX Group Ltd. creates enterprise asset management software solutions and provides associated services to infrastructure, energy retail, transport, water, nuclear, retail, aviation, and energy industries. It offers its Ellipse application to manage the asset life cycle, from design, work management, and maintenance through to replacement planning. The company turned over $55m per year with a profit of $16m at the time of being acquired.

Nic has a track record of success in mining software, namely his involvement running Gemcom Asia Pacific, which was acquired byJMI Equity for CAD180m in 2008(CAD2.90 per share). When Nic joined the company’s shares were valued at CAD50c.

Gemcom Software International Inc. (TSX:GCM) was the largest global supplier of specialised mining productivity solutions.

..What does K2F do?

K2F provides technical assurance enterprise Software-as-a-Service (SaaS) solutions that deliver environmental, social and governance (ESG) outcomes.

ESG is considered the most important consideration and biggest risk to mining companies globally. As a result, its current solutions have seen tailwinds as a result of regulatory changes and its upcoming solutions aim to benefit from increased regulatory burden on miners.

Also, K2F currently provides consulting services to top tier miners, and plans to transition to a pure SaaS company over the coming quarters.

..What is Environmental, Social and Governance (ESG) and why is it a massive problem for mining companies?

In July 2020, the most successful mining financier in the world, Robert Friedland, said ESG will change the way metals are priced.

ESG encompasses a variety of factors, including climate change, waste water, pollution, human rights, community, ethics, taxation etc.

Clearly Brian and Nic saw this huge opportunity and leveraged their experience successfully building asset management software companies before putting together the right team, business model and Go-To-Market (GTM) strategy to do it all over again!”

..What are K2F’s SaaS solutions and how do they solve big ESG pain points for mining companies?

Products are the past

Historically, K2F has provided SaaS products to the mining industry.

For example, their RCubed product is a reserve and resource reporting solution that has grown Annual Recurring Revenue (ARR) 5x in less than 12 months (AUD400k to AUD2m). If this doesn’t scream early signs of Product Market Fit (PMF), then I don’t know what does!

Its other SaaS product is Infoscope, which is a land management solution that comprises multiple modules.

https://www.asx.com.au/asxpdf/20200508/pdf/44hp7lj4m43w4l.pdf

Solutions are the future!

K2F has recently moved away from providing SaaS ‘products’ to providing ‘solutions’ as part of a strategic change in their Go-To-Market (GTM) strategy. This change is important for their ongoing growth and increased distribution efficiencies (which I will discuss in detail further down) because it creates multiple ‘solutions’ from their two existing ‘products’, RCubed and Infoscope.

K2F now provides SaaS solutions for Land Access, Community Heritage, Rehab, Dams and Tailings and Resource Inventory.

The objective of the new solutions approach is to leverage existing IP within their products. For example, Dams and Tailings solution leverages IP that sits within RCubed and Infoscope.

This will enable them to provide their existing and new clients with a broad suite of solutions for their problems, instead of two products. This modularised approach gives them the ability to cross-sell following successful commercial outcomes with other solutions, instead of selling one product and then only having one other product to sell. As a result, the company can now capture more of the economic value they create for the clients (in the form of Return on Investment (ROI) from efficiency gains and savings on the bottom line), which should translate into increased ARR per client and more deals.

Further, all of K2F’s solutions are in demand as a result of new, and continuously increasing, regulation and standards requirements imposed on mining companies globally. The severity of these changes is evidenced by the uptake of K2F solutions by the largest miners in the world and exponential growth of the company’s ARR and ACV.

The upcoming Tailings and Dams solution is evidence of the severity of the problem for mining companies.The solution is currently being co-developed with Wesfarmers backed Decipher and SAP. The partnership aims to create an integrated monitoring and governance platform for tailings storage facilities, which will provide an elegant solution to effectively manage mineral waste and monitor risk.

..What traction have their SaaS offerings had?

The company’s stated objective is to transition toward a pure SaaS company over the coming quarters and substantially grow ARR (current ARR makes up only 36% of total invoices, up from only 10% 12 months ago).

https://www.asx.com.au/asxpdf/20200728/pdf/44kx4qcgfncnqp.pdf

*Please note that the dates in the pie graphs above are incorrect, they should be FY18/19 and FY19/20, respectively (left and right).

K2F is the fastest organically growing SaaS company on the ASX.Its ARR hasgrown from AUD850k to AUD2.36m in the last 12 months (177% Year on Year (YoY) growth) as at 30 June 2020.

Also, the company’s current Total Contract Values (TCV) have grown 663% YoY (~AUD1m at 30 June 2019 to AUD7.5m at 30 June 2020).

https://www.asx.com.au/asxpdf/20200728/pdf/44kx4qcgfncnqp.pdf

K2F solutions are deployed, or being implemented, in 47 countries across more than 460 mine sites globally.

Also, K2F boasts some of the largest global Tier 1 mining companies as clients.

..How have their SaaS products performed and why are they solving an important problem for mining companies?

RCubed is the only off the shelf solution that provides reports that need to be produced by some of the world’s largest mining companies, which has seen its ARR grow 5x in less than 12 months

RCubed was the game changer, which was acquired by K2F in mid 2019. They acquired it about a year ago and grew ARR for the product from AUD400k to AUD2m (5x). RCubed is a resource and reserve reporting solution. The SEC has imposed a Jan 2021 deadline on compliance with reporting this info and RCubed is the only off the shelf solution in the world (hence why they have signed the biggest global mines in the last year, including those that aren’t in the US – Fortescue, South32, Vale, Rio, Glencore etc).

There is another regulatory and compliance change that K2F is building a SaaS solution for and it should see similar uptake and exponential ARR growth like RCubed.

As discussed above, the company plans to cross-sell its suite of solutions to existing RCubed and Infoscope clients, including its upcoming Dams and Tailings Management solutionand is already in discussions with several large global miners.

According to a recent KPMG report, tailings management is one of the top 10 risks in 2020 for the mining industry.

Decipher CEO Anthony Walker noted in a recent release that‘the resources industry needs a solution that is cost effective, comprehensive and accessible, and [K2F and Decipher] can deliver on that”.

In August 2020, theGlobal Tailings Review launched its new Global Industry Standards of Tailings Management (GISTM), which aims to prevent tailings disasters such as theBrumadinho collapsethat occurred in January 2019, killing 259 people. Also, Mining giant BHP is currently facing one of the largest group claims in UK legal history over the failure of one of its Tailings dams in Brazil.

The management of dams and tailings is one of, if not the biggest risk and talking points on mining decision makers going forward. It’s no surprise that the billionaire mining magnate Robert Friedland stressed the importance of ESG on mining companies a few months ago!

..What opportunities and TAM’s are available to K2F outside of mining?

https://www.asx.com.au/asxpdf/20200508/pdf/44hp7lj4m43w4l.pdf

The company plans to expand its range of mining products in an industry with a likely AUD1bn TAM (it’s always hard to put a figure on it when they are broadening their suite of products in such a large potential market). Also, mining seems to be at an inflection point where it is primed for decades of growth as it comes out from a trough. This should see the number and size of mining companies grow in an environmentally and socially responsible way.

Lastly, once K2F has dominated the mining market, K2F intends to move into the AUD2bn Oil and Gas markets. The objective is to help companies in these adjacent markets solve similar ESG issues using K2F’s solutions.

..Why is K2F more likely to continue to grow fast and in a capital efficient way compared to other SaaS companies?

A multi-channel sales approach that leverages their position as a thought leader, promotes customer intimacy and incentives their distribution partners such as a SAP to help them distribute their solutions

The company uses its position in the market as a Thought Leader and its proven global distribution partnerships (e.g. SAP, Esri etc) to generate leads with very little cost, which are then managed and closed by a small group of salespeople, which can be scaled up efficiently.

In addition to direct sales (outbound) by their SaaS business developers and account managers, the company’s consulting division continues to build new client relationships that indirectly benefit the SaaS side of the business.

As a result, the company has a capital efficient distribution model that should allow them to continuously build their ARR and deliver innovative solutions in their target markets.

..Why do I think K2F will continue to grow fast and efficiently?

Most SaaS companies spend 1 dollar to make 80 cents in ARR. This is not sustainable, and it is often seen only after they massively slow down. Many investors are left scratching their head asking why did it slow down when it was growing so fast?

All they had to do was look into how much their sales and marketing costs are. However, this can be challenging as it is not part of the usual investor checklist.

K2F has excellent operational metrics. Its ARR growth is top-tier (75th to 90th percentile) and the trajectory looks like that of a VC backed unicorn, but it could very easily stall and drop back to earth.

I have demonstrated below why I don’t think this will happen by comparing K2F’s most important metrics against global B2B SaaS benchmarks (using a combination of listed, PE, VC data).

..How does K2F’s ARR growth compare to other global SaaS companies?

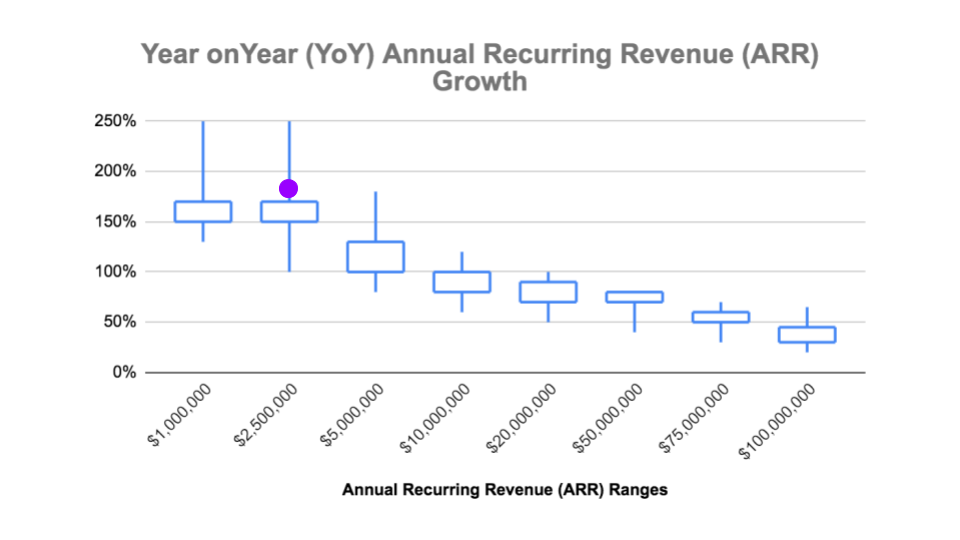

Benchmarking K2F’s ARR growth against comparable B2B SaaS Metrics, its 177% YoY ARR growth rate puts it between 75th and 90th percentile for a company between the AUD1m to AUD2.5m ARR stage (refer to graph below, where I have marked that K2F sits just above the 75th percentile of B2B SaaS companies between 1m and 2.5m ARR using the purple dot).

Please note that the square on each candle in the graph below denotes the 50th and 75th percentile range, and the top and bottom of the stick denotes the 90th and 25th percentiles respectively (90th percentile being the best, 25th percentile being the worst).

Also, for a more detailed breakdown on how I analyse operational metrics and unit economics, I suggest you readmy Pointerra (ASX:3DP) article. Reading the 3DP article before the K2F article will give you a better understanding of the most important B2B SaaS operational metrics and unit economics, how to calculate them and why they are important to determine a company’s potential.

This means it is looking like it will be shortly following the Triple, Triple, Double, Double, Double (T2D3) path for a unicorn SaaS company, which is the trajectory for SaaS companies that reach a USD1bn valuation.

The playbook for T2D3 is to hire a sales leader and team once you have a solid base of a few million dollars in ARR. This seems to be the area that K2F is at, so using the tailwinds from the ESG push in the mining industry and their current and upcoming products, means K2F is well placed to capitalise on this opportunity.

..How capital efficient is its sales and marketing compared to other B2B SaaS companies?

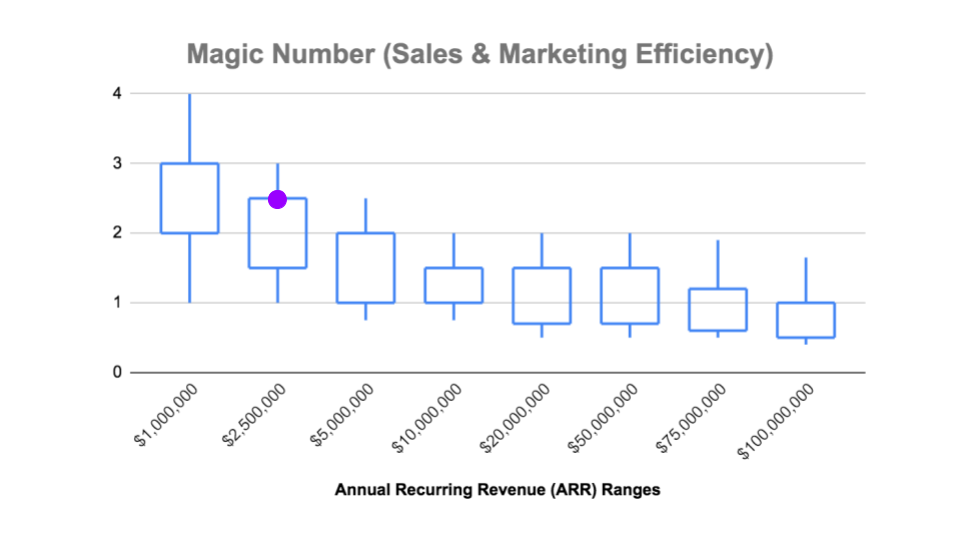

The Magic Number (Sales and Marketing Efficiency)

Simple. It spends 1 dollar to make 1 dollar in ARR (it actually spends 1 dollar and makes 2.2 dollars of ARR, which I’ll explain below). Essentially, its sales and marketing engine is very capital efficient.

A SaaS company’s Sales and Marketing (S&M) Efficiency is commonly referred to as the Magic Number.

I use a derivation of the Magic Number, which is closer to the Bessemer CAC ratio.

As suggested above, you can read more about the Magic Number and other operational metrics and unit economicshere).

Based on my analysis, this means they have a Magic Number (Bessemer CAC ratio) of ~2.2 and puts it around the 75th percentile when compared to global venture backed SaaS companies. Refer to the graph below for a benchmark comparison.

This means its sales team and marketing spend is super efficient and productive, which puts the company in a position to scale in a capital efficient way.

However, the downside of underspending on S&M means that potentially the company is not growing as fast as it could and not taking as much market share as it may otherwise be able to.

I usually prefer underspending and discipline early than overspending and then working out how to operate efficiently.

Lastly, keep in mind that K2F is about to move from the AUD1m to AUD2.5m ARR range to the AUD2.5m to AUD5m range, which if it continues the same 2.2 Magic Number it would be in the 90th Percentile.

..What other important metrics demonstrate K2F’s excellence?

As an Enterprise SaaS company, the quality of K2F’s ARR is the highest it could be because the contract terms are longer than if their clients were small businesses or consumers and they are less likely to churn (currently around 3 years with an average of AUD130k ARR and TCV of AUD400k).

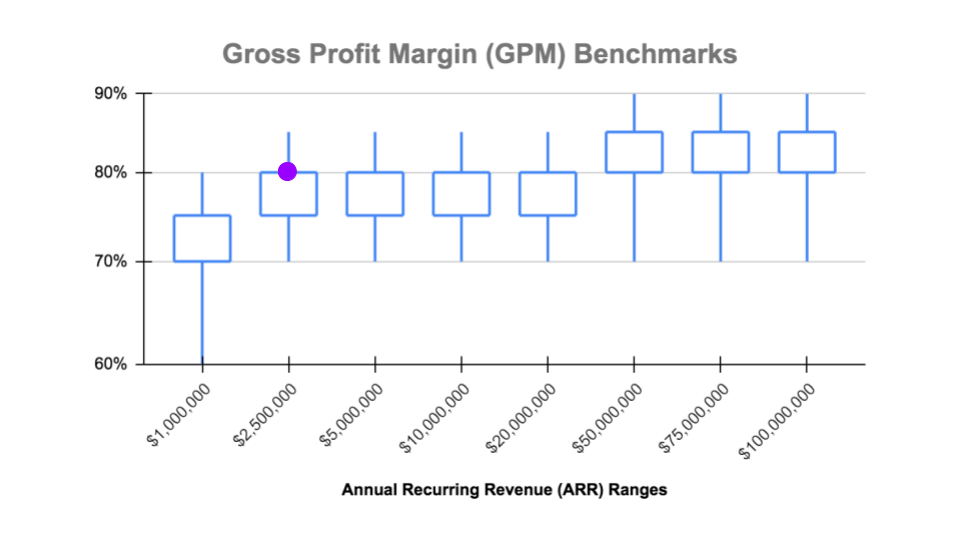

Also, products like K2F’s usually enjoy Gross Profit Margins above 80%, which increases over time. 80% GPM is in the 75th Percentile for a company with AUD2.5m ARR.

This means that K2F should command a greater valuation than other SMB or Consumer SaaS companies.

..Where to from here for K2F?

I believe K2F’s SaaS based operational metrics put it in the 75th and 90th percentile when compared to global SaaS companies at its current stage.

In terms of what’s next for K2F, there is no guarantee of continued success and growth.

However, using operational benchmarks allows an investor to make the most informed decisions andremove some of the emotional-biases when investing in B2B SaaS companies.

Also, the company is transitioning to a pure SaaS business, leveraging the ESG push in the mining industry, continuing to build and acquire additional complementary SaaS products and scale their sales and marketing.

..How is the company being valued now and what opportunity might this present for investors?

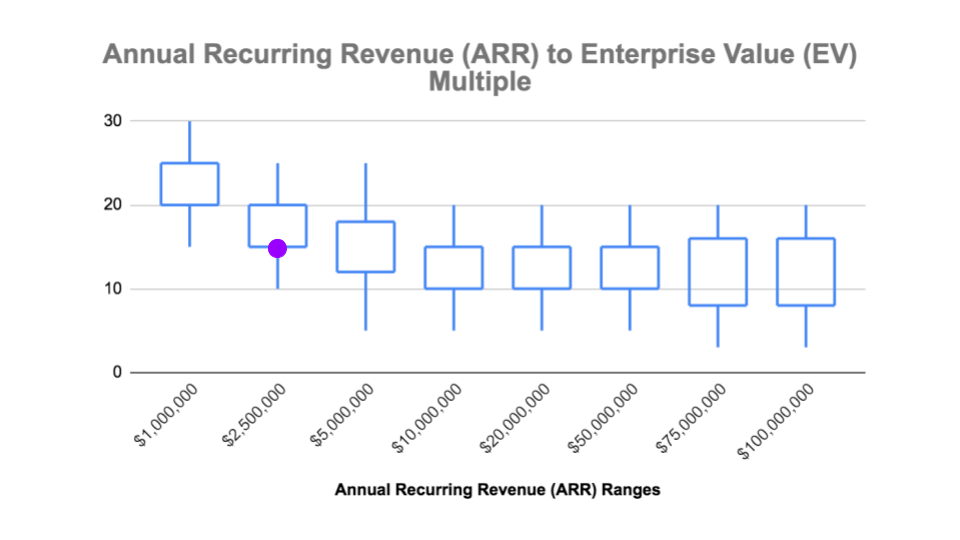

Its current EV is approximately AUD35m (as at 20 September 2020), which puts its EV/ARR Multiple at only 13x (comparative ASX SaaS companies have 20-30x multiples growing at half the speed and similar size ARR).

Having regard to the benchmarks in the graph above, this means K2F is being valued like an average (median) early-stage SaaS company. This means that the market has potentially not factored in its operational excellence and therefore its likelihood of continued fast growth and capital efficiency.

In terms of its TAM and potential additional market opportunities, I think ESG will continue to be a major focus for mining companies big and small, and this trend will be similar for other market opportunities such as oil, gas, electricity etc.

As a result, this may present a rare opportunity for the savvy investor who understands the nuances of B2B SaaS companies.

Disclaimer: At the time of publishing this article, I own shares in ASX:K2F.

Source: https://trackrecord.news/company-profile-k2f-asxk2f/

K2F Profile: 70c+ share price target

Add K2F (ASX) to my watchlist

(20min delay) (20min delay)

|

|||||

|

Last

9.3¢ |

Change

0.007(8.14%) |

Mkt cap ! $17.38M | |||

| Open | High | Low | Value | Volume |

| 9.3¢ | 9.3¢ | 9.3¢ | $2.272K | 24.42K |

Buyers (Bids)

| No. | Vol. | Price($) |

|---|---|---|

| 1 | 98938 | 9.2¢ |

Sellers (Offers)

| Price($) | Vol. | No. |

|---|---|---|

| 9.4¢ | 55066 | 2 |

View Market Depth

| Last trade - 10.43am 03/05/2024 (20 minute delay) ? |

|

|||||

|

Last

9.2¢ |

Change

0.007 ( 6.98 %) |

||||

| Open | High | Low | Volume | ||

| 9.2¢ | 9.2¢ | 9.2¢ | 17048 | ||

| Last updated 10.43am 03/05/2024 ? | |||||

| K2F (ASX) Chart |