So:

1) Laurentian is obviously right that lithium is a commodity. Someday it will be in oversupply and the companies that mine that commodity will crash. It's totally consistent with that fact that the EV market could boom and flourish and Lithium pricing could stagnate and collapse. Those two things could happen simultaneously, given the right supply and demand combination.

2) He is just guessing, but he has a decent analysis. The summary of his argument is:

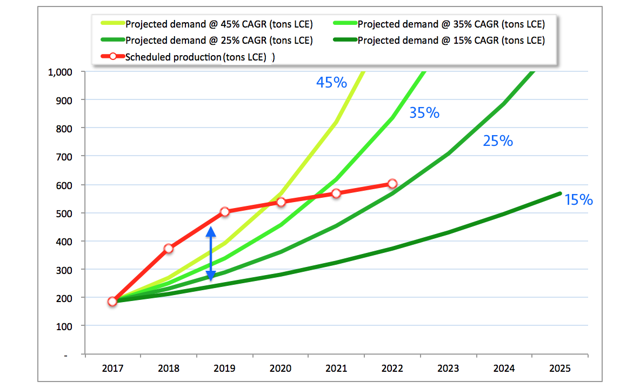

* In the base case of 15% CAGR of demand growth, there will occur a major episode from 2018-2019 of 75-105% overcapacity above demand.

* Even if demand grows at a much higher rate of 45%, production capacity will still exceed demand by 29-39%.

* Such a supply surplus will not be absorbed until 2020 when the completion of a slew of Li-ion battery mega factories pushes the lithium demand to 522 kton of LCE.

3) You only need to look at the price graphs of all of the lithium miners to be reminded how psychotic the market actually is on this pricing issue. The prices ramp and then the prices go into long six-month declines. No one quite knows where the price is heading in a situation where demand had to ramp at huge rates to keep up with supply increases. That should make anyone cautionary about investing after a long ramping period, which is what we have right now.

4) This is a really treacherous mineral in which to invest in a junior with high production costs. Orocobre is one of the only lithium miners I am seriously considering because they have low-cost production.

Add to My Watchlist

What is My Watchlist?