A look at the current lithium demand.

Some forecasts of future lithium demand.

My three top picks to play the lithium bull run.

2016 has seen the lithium spot prices explode higher on the back of booming EV sales and a shortage of lithium, as battery manufacturers rush to secure supply. This may be just the beginning of a huge 20-year bull run for the lithium miners. A comparison would be buying the oil companies just around the time Ford (NYSE:F) started to mass produce cars. Of course, there are a lot more cars today, so the potential is even bigger.

In this article, I try to understand how much lithium demand may increase going forward, and which lithium miners are likely to meet this extra demand. Given these supply/demand factors, what is the likely lithium average spot price range in the coming years, and the implications on the lithium miners. Finally, I look at my three top lithium stocks potential to meet the new demand and how that can impact their stock price. For a background, you can read my previous articles on the lithium miners here, here and here.

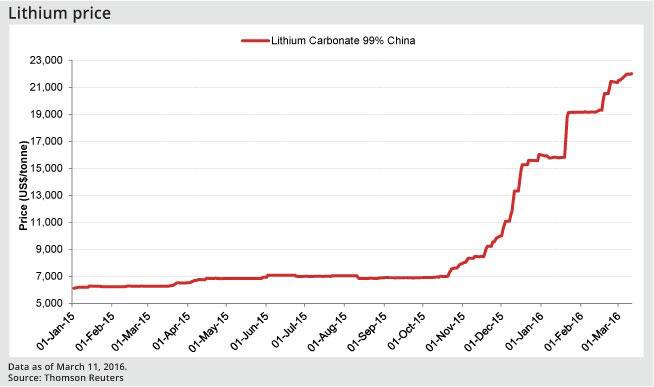

Lithium Spot Price in China

The Current Lithium demand

According to Goldman Sachs in its December 2015 report "Lithium is the New Gasoline":

Total lithium demand today is 160,000mT of lithium carbonate equivalent (LCE) per year.

For every 1% increase in battery electric vehicle (BEV) penetration, there is an increase in lithium demand by around 70,000mT of LCE/year.

2016 has seen the lithium spot prices explode higher on the back of booming EV sales and a shortage of lithium, as battery manufacturers rush to secure supply. This may be just the beginning of a huge 20-year bull run for the lithium miners. A comparison would be buying the oil companies just around the time Ford (NYSE:F) started to mass produce cars. Of course, there are a lot more cars today, so the potential is even bigger.

In this article, I try to understand how much lithium demand may increase going forward, and which lithium miners are likely to meet this extra demand. Given these supply/demand factors, what is the likely lithium average spot price range in the coming years, and the implications on the lithium miners. Finally, I look at my three top lithium stocks potential to meet the new demand and how that can impact their stock price. For a background, you can read my previous articles on the lithium miners here, here and here.

Lithium Spot Price in China

The Current Lithium demand

According to Goldman Sachs in its December 2015 report "Lithium is the New Gasoline":

Total lithium demand today is 160,000mT of lithium carbonate equivalent (LCE) per year.

For every 1% increase in battery electric vehicle (BEV) penetration, there is an increase in lithium demand by around 70,000mT of LCE/year.

The Keys to Lithium Growth

Lower lithium-ion battery costs (now down to around USD 200-kWhr) to make electric vehicles (EVs) more affordable. Tony Seba in his video on "clean energy disruption" and others expect EVs to be cheaper than Internal Combustion Energy (ICE) cars by 2020.

EV (cars, buses, bikes) adoption to increase. Lower price, longer range, and more charging networks are all helping.

Energy storage using lithium batteries becoming more popular.

Lithium Demand Forecasts to 2025

Goldman Sachs - "Growth in EV applications alone could triple the size of the entire lithium market from 160,000 mt today to 470,000 mt by 2025. That is based on 22% EV penetration (BEV, PHEV and HEV combined) in 2025 from under 3% today."

Deutsche Bank in its "Lithium-ion age" stated, "Global battery consumption is set to increase 5x over the next 10 years, placing pressure on the battery supply chain and lithium market. We expect global lithium demand will increase from 181kt Lithium Carbonate Equivalent (LCE) in 2015 to 535kt LCE by 2025."

Summary of Expected Lithium Carbonate Demand to 2025

NB: Current demand figures vary based on the dates of reports being slightly different.

From the above estimates, let's assume the demand will increase by around 340,000 tonnes of LCE pa, over the next 8.5 years. That is an increase of around 40,000 tonnes pa. This leaves plenty of room for existing lithium miners to expand production and for new lithium miners. I think the GS and DB forecasts may prove to be very conservative, more on this later.

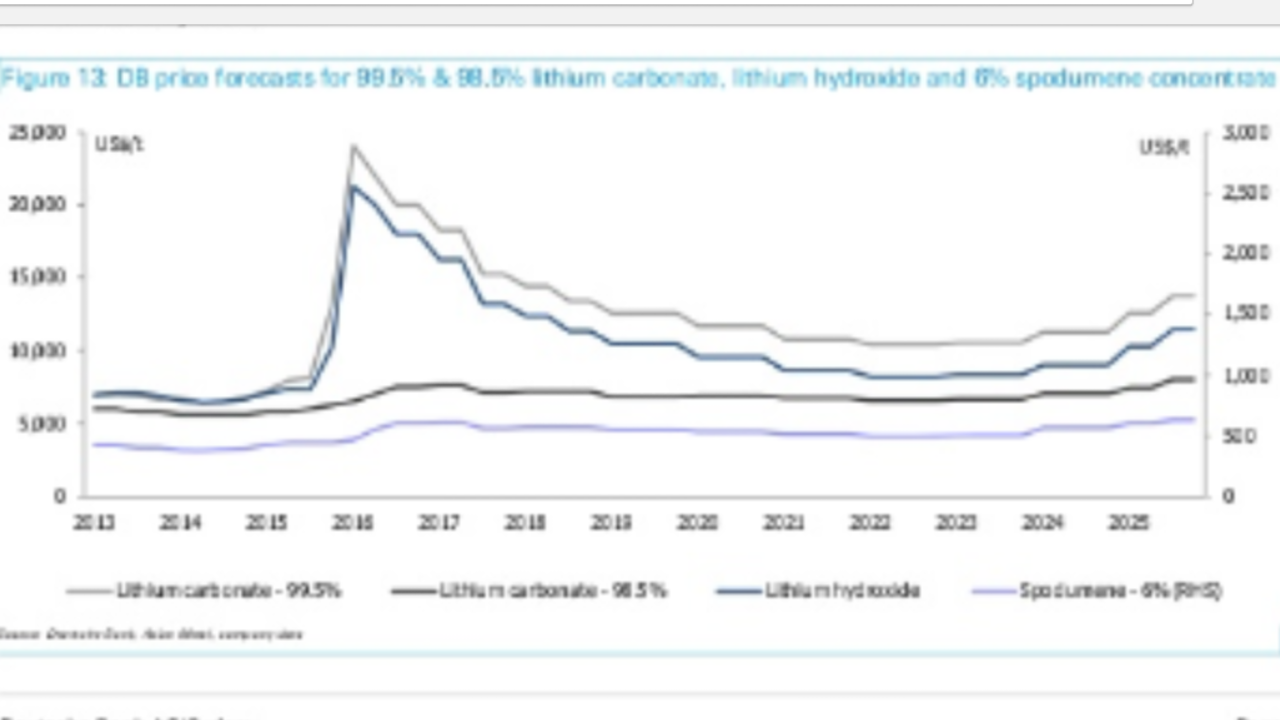

Lithium Carbonate Spot Price Forecasts to 2025

Deutsche Bank forecast 99.5% LCE spot price to average around USD 10,000-11,000 per tonne for the years 2020-2025 (see graph below). Up until 2020, it forecast prices to be elevated from a peak of 25,000/t in 2016 and gradually easing back down towards 10,000-11,000 by 2020.

Deutsche Bank Lithium Spot Price Projections to 2025

How Some of the New Pure-Play Lithium Miners Will Meet This New Demand

NB: Given the potential for higher demand, the above companies may try to ramp quicker and double the above figures.

The above table shows my three top picks in the lithium mining sector - Orocobre, Lithium Americas, and Bacanora Minerals.

The table below shows my stock price estimates for the three. I view Orocobre as a safer core lithium miner as it is already producing and ramping up production. Lithium Americas should be producing by around 2018, and is well valued still. Similar with Bacanora Minerals, which also has a Tesla (NASDAQ:TSLA) off-take agreement in place. You can view more about these stocks in my last article.

Three Major New Producers Coming - 2020 Stock Price Forecasts

Column 1

Column 2

Column 3

Column 4

Column 5

Column 6

Column 7

1

Production (t/pa)

Current Market cap m

2020 net profits est. USD m

Current stock price

Stock price estimate in 2020

Potential gain by 2020 (times)

2

Orocobre

35,000

AUD 913

91

AUD 4.35

AUD 8.49

1.95

3

Lithium Americas

20,000

CAD 251

77

CAD 0.86

CAD 5.16

6.0

4

Bacanora Minerals

17,500

CAD 188

64

CAD 1.93

CAD 12.79

6.62

Assumptions

Production cost price = USD 2,500/t (USD2,700/t for Bacanora); Selling price = USD 10,000/t

I have not adjusted for the capital raisings. It may be safer to adjust above stock price forecasts for by say 25% due to possible future capital raisings diluting EPS.

PE of 15 assumed. SG&A (15% of revenues); Tax and interest expenses - 30%.

Comparison to the Almost Fully-Valued Australian Miners

I have not included the Australia spodumene new producers in the above table as they are difficult to compare. For example Pilbara Minerals (ASXLS) (price = AUD 0.70) expects to sell 300,000 tonnes of spodumene in 2017, with around $400 profit/t, or USD120m profit before other expenses. Assume its net profit is around USD 60m or say AUD 75m (after all expenses). Its current market cap is AUD 742m. Based on AUD 75m net profit, and a PE of 15, its market cap valuation is around AUD 1,125m. So upside is 1.5 times, or a stock price target for 2017 of AUD 1.05. A nice 50% upside, but a lot less than those in the table above. This is mostly because PLS's stock has risen 1,221% in the past year, and I am comparing a 2017 stock price with 2020 stock prices above. Also remember I have not allowed for any stock dilution for those in the table above. For PLS to be as compelling, it would need to substantially increase production levels. Nonetheless a 50% upside for a soon to be producing lithium miner is still good.

The other Australian spodumene miners such as Galaxy Resources (OTCPK:GALXF) (ASX:GXY) has been quick to ramp up production as spodumene can come into production quicker than brine. General Mining [ASX:GMM] and Altura Mining (OTC:ALTAF) (ASX:AJM) will also benefit from increased lithium demand.

These companies also have very strong potential to do well despite many of them rising over 1,000% in the past year. Investors can buy some now and more on any market dips. This is the strength and potential of the lithium boom. "For every 1% increase in battery electric vehicle (BEV) penetration, there is an increase in lithium demand by around 70,000mT of LCE/year."

I take this point further in the table below. Let's do some forecasting and assume EVs become 100% adopted by 2040. The S curve of new invention adoption suggests a slow start, followed by an exponential rise. You can read about this here, where I discuss how "EVs will most likely be the next big thing".

My EV Penetration and Lithium Demand Forecasts to 2040

Column 1

Column 2

Column 3

Column 4

Column 5

Column 6

Column 7

1

Year

2015

2020

2025

2030

2035

2040

2

EV (BEV) penetration

1%

5%

20%

40%

70%

100%

3

EV lithium demand ('000 tonnes pa)

70

350

1,400

2,800

4,900

7,000

If BEV penetration is at 20% by 2025 (i.e. 20% of all new vehicles sold are 100% battery electric vehicles), then we will need an extra 1.4 million tonnes of LCE per year. As you read earlier, that is about triple the figure Goldman Sachs (470Ktpa) and Deutsche Bank (535Ktpa) are currently forecasting. I think it is quite likely we are underestimating how quickly EV adoption may occur. The issue will then be finding enough supply of lithium to meet surging demand. Those miners that can bring new lithium to market to meet this demand will get high prices and rapidly rising volumes. A recipe for rapidly rising profits and stock prices. If the EV boom goes mainstream, as happened before with smartphones, then there will be fortunes made in a short period of time. It will also make my forecasts for my top three lithium miners look way too conservative, even if they seem quite optimistic here in 2016.

Risks to the Above Forecasts

EV adoption does not take off. Given all the ICE companies are now involved and EVs are mechanically better and will soon be cheaper to buy, I see this as unlikely.

New battery chemistries will replace lithium. This is possible, but again unlikely given lithium's unique properties.

Lithium oversupply will occur. This is the greatest risk. To combat this risk, I prefer to buy the lowest-cost lithium miners.

Conclusion

Continual EV adoption and perhaps energy storage using lithium-ion batteries will lead to an enormous new demand for lithium (as well as cobalt and graphite).

Since the Tesla Model 3 launch success in April 2016 and the tripling of lithium spot prices in 2016, the market has begun to realize the enormous opportunity.

I first wrote about "Chinese electric vehicles about to boom" back in March 2015. By December of 2015, I could see the sense in buying the lithium, cobalt and graphite miners as I outlined here and here. The later article titled "Solar, Electric Vehicles Could Make Oil And ICE Cars Obsolete - The Era Of Oil Is Almost Over", was met with some skepticism. Yet, fast forward to now, and we have entered the lithium boom.

In this article, I highlighted the huge potential demand should EV adoption continue growing strongly. In fact, I present a case that the demand will be a lot stronger than what is currently forecast. For example, in 2015 in Norway, 23% of all new cars sold were EVs. I believe Norway is showing us a sign of what's to come next.

My view is we are just at the beginning of a 20-year EV, lithium, cobalt, and graphite bull run.

I think right now that the best investment potential is in the lithium miners that are soon about to become producers. This is because they are still not reflecting the full valuations of the producers, and because their earnings will ramp from zero to around $64-91m pa by 2020 or slightly earlier.

The three best valued new producers (by 2020) in my opinion are Orocobre, Lithium Americas, and Bacanora Minerals.

Orocobre is the safest as it is already producing, and I see potential 1.95 times or more upside in the stock by 2020.

Lithium Americas has the potential to rise up to 6 times, although share dilution may reduce this to around 4.5 times. More risk, as not yet in production.

Bacanora Minerals has the potential to rise 6.62 times, or after some share dilution around 5 times. Also more risk as not yet in production.

I also agree the current pure-play lithium producers from Australia such as Galaxy Resources, and soon Pilbara Minerals and Altura Mining can do very well.

Having said that, if EV adoption and energy storage grow exponentially, then all the producing lithium miners, cobalt miners and graphite miners will do extremely well, and we will have one of the best bull runs ever seen.

Disclosure:I am/we are long TSLA, ASX:ORE, TSX:LAC, TSXV:BCN.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: The information in this article is general in nature and should not be relied upon as personal financial advice.

Editor's Note: This article covers one or more stocks trading at less than $1 per share and/or with less than a $100 million market cap. Please be aware of the risks associated with these stocks.

The Keys to Lithium Growth

Lower lithium-ion battery costs (now down to around USD 200-kWhr) to make electric vehicles (EVs) more affordable. Tony Seba in his video on "clean energy disruption" and others expect EVs to be cheaper than Internal Combustion Energy (ICE) cars by 2020.

EV (cars, buses, bikes) adoption to increase. Lower price, longer range, and more charging networks are all helping.

Energy storage using lithium batteries becoming more popular

The Keys to Lithium Growth

Lower lithium-ion battery costs (now down to around USD 200-kWhr) to make electric vehicles (EVs) more affordable. Tony Seba in his video on "clean energy disruption" and others expect EVs to be cheaper than Internal Combustion Energy (ICE) cars by 2020.

EV (cars, buses, bikes) adoption to increase. Lower price, longer range, and more charging networks are all helping.

Energy storage using lithium batteries becoming more popular

A personalised tool to help users track selected stocks. Delivering real-time notifications on price updates, announcements, and performance stats on each to help make informed investment decisions.

LS) (price = AUD 0.70) expects to sell 300,000 tonnes of spodumene in 2017, with around $400 profit/t, or USD120m profit before other expenses. Assume its net profit is around USD 60m or say AUD 75m (after all expenses). Its current market cap is AUD 742m. Based on AUD 75m net profit, and a PE of 15, its market cap valuation is around AUD 1,125m. So upside is 1.5 times, or a stock price target for 2017 of AUD 1.05. A nice 50% upside, but a lot less than those in the table above. This is mostly because PLS's stock has risen 1,221% in the past year, and I am comparing a 2017 stock price with 2020 stock prices above. Also remember I have not allowed for any stock dilution for those in the table above. For PLS to be as compelling, it would need to substantially increase production levels. Nonetheless a 50% upside for a soon to be producing lithium miner is still good.