A long but good read

https://www.readwriteinvest.com/p/producing-in-the-fast-lane

regards

DF

Producing in the fast lane"Overcapacity" in the Chinese auto manufacturing sector

The narrative of “excess” or “overcapacity” in the Chinese industrial sector is re-emerging, particularly with the geopolitically sensitive auto sector. It is related to overarching themes about China’s propensity to support supply-side producers at the expense of demand-side consumers, necessitating other countries to meet the demand shortfall.

Here, in a recent report whose title “Overcapacity at the Gate” pays homage to the leveraged buyout classic1, research firm Rhodium writes:

China’s National People’s Congress concluded in March 2024 with an explicit focus on industrial policy favoring high-technology industries, and very little fiscal support for household consumption. This policy mix will compound the growing imbalance between domestic supply and demand. Systemic bias toward supporting producers rather than households or consumers allows Chinese firms to ramp up production despite low margins, without the fear of bankruptcy that constrains firms in market economies.

In this piece, I want to focus on “overcapacity” in the auto industry. First we need to discuss exactly what “overcapacity” means.

“Overcapacity is a Feature, Not a Bug”

If you follow me on Twitter/X, you may have noticed that I have been somewhat of a broken record2 on this phrase because many do not seem to fully understand what “overcapacity” means in a China context and to Chinese policymakers3.

Traditionally, the term “overcapacity” was usually used when referring to mature industries. Rhodium describes the term here:

The simplest and most widely accepted definition of overcapacity is when factories’ production capacity is under-utilized. While temporary overcapacity can be harmless and a normal part of market cycles, it becomes a problem when it is sustained through government intervention. Structural overcapacity happens when companies maintain or grow their unused capacity without worrying about making a profit (or a loss), often due to a lack of economic pressure to operate efficiently, like a hard budget constraint.

Chinese policymakers often consider “overcapacity”4 in the context of nascent, developing industries like electric vehicles.

In his book 置身事内:中国政府与经济发展 (English translation entitled “How China Works: An Introduction to China’s State-led Economic Development”)5 Lan Xiaohuan, a professor at the School of Economics at Fudan University, discusses how “overcapacity” can help a new industry get started from scratch and why it is not perceived as a risk in the same way others do6. Pekingnology provides an excellent translation of the passages here.

First, “overcapacity” is less of a risk at the early stages of any industry, especially for developing countries where adoption curves are highly predictable, providing comfort that demand will grow into the new capacity.

Second, there are learning spillovers that can lead to the accumulation of human capital.

Third, done right “overcapacity” creates competitive conditions that can ultimately drive production efficiencies.

There is an element of creative destruction that is reminiscent of the ethos that has driven Silicon Valley to become one of the most productive regions on this planet.

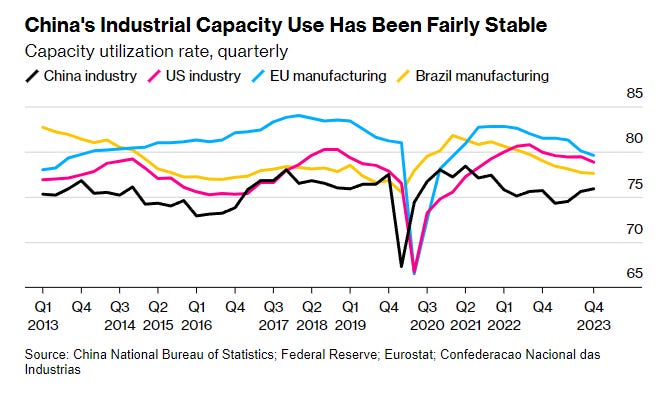

On the flipside, Chinese policymakers themselves are quite sensitive to overcapacity7in mature industries. Following a buildup of industrial capacity following the 2008 GFC8, in 2016, Chinese policymakers enacted a series of policies to reduce excess capacity in the steel and coal industries9 that proved to be effective10.

Here we can see how China’s industrial capacity utilization rate (black line) rebounded from lows in late 2015.

The ICE-to-EV transition and China’s evolving role as a car exporter

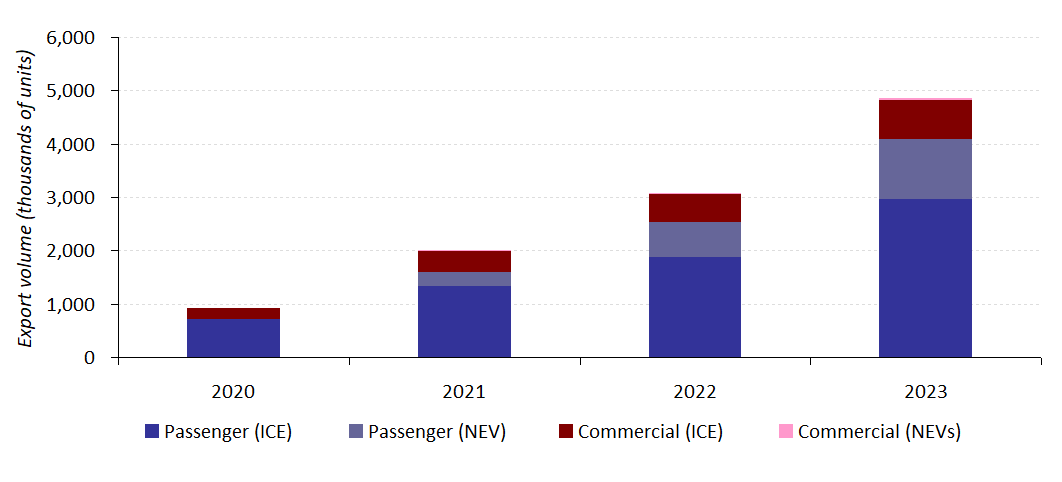

Of particular concern to Western automakers have been rising exports of Chinese automobiles. These have risen significantly in recent years to 5 million in 2023, making China the largest vehicle exporter in the world, surpassing Japan. Some conflate rising exports with “overcapacity” and “weak demand”.

Auto manufacturing is a geopolitically sensitive industry — anybody who was around in the 1980s remembers the backlash against Japanese automobiles11. Four decades later we are going through a similar cycle with Chinese cars.

There are a number of factors behind rising Chinese exports but the most impactful is transport electrification. Rapid rise in NEV adoption in China has been driven by the combination of feature improvement and price reduction that make them very competitive with ICE vehicles.

However, not all car exports are created equal and there is more to this story than just transport electrification. This requires digging deeper into the numbers.

First, we need to focus on the passenger car segment. Out of the 4.9 million vehicles exported in 2023, 769k were commercial vehicles like buses, tractor trailers and light to heavy trucks. Many of these commercial vehicles are sold into markets like Russia/ CIS, the Middle East, and Southeast Asia and are less of a concern to incumbent automakers.

Note: these figures include additional categories from CAAM data including minibuses. Source: @tphuangThis leaves approximately 4.1 million passenger cars. Out of this number, we can further segment this out by ICE (3.0 million) and NEV (1.1 million) car exports. Each of these categories is driven by a different set of dynamics.

Passenger ICE vehicle exports

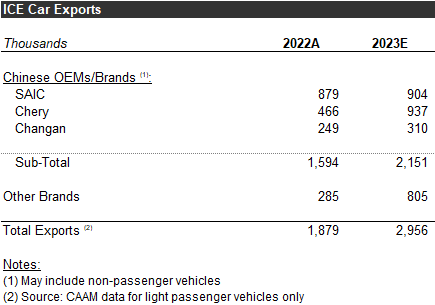

ICE vehicle exports have been boosted from rapid consumer adoption of NEVs. Within the ICE market, there is a bifurcation between Chinese brands and foreign brands manufactured through joint ventures.

As domestic market share has dwindled, Chinese ICE brands like Chery are finding success diverting some of the newly freed up capacity towards export markets, primarily in developing countries.

However, foreign JVs were not originally structured with the intention of exporting and have been bearing the brunt of declining capacity utilization. Many foreign automakers that do not have competitive NEV offerings are opting to exit the China market. A recent example was Mitsubishi which gave up its share of its JV to its partner GAC Aion last October.

Meanwhile, ICE factories are being converted into NEV factories. Following the shutdown of the joint venture, GAC Aion has converted former ICE manufacturing facilities into NEV production, even expanding production capacity by 50%. It takes time to build a “greenfield” NEV factory and starting with an existing “brownfield” facility can shorten lead times. Expect more consolidation of ICE factories in the coming years, which will result in the absorption of excess capacity.

This excess ICE capacity does not fit the definition of “structural overcapacity” defined earlier in the Rhodium report. It was added mainly by foreign joint ventures where there was a profit expectation and shareholder “pressure to operate efficiently”. The investment decisions were made by economic actors subject to Kornai’s “hard-budget constraint”.

When these plants were built, very few expected the speed at which they would be made obsolete by NEVs. Things do not always turn out exactly as one expects at the time investments are made; this happens in many industry sectors and is a normal part of doing business. The key here is that this excess ICE capacity has a limited lifespan and will be absorbed as quickly as automakers can setup new NEV lines.

Passenger NEV exports

For many, the most concerning aspect of rising Chinese exports are NEVs — as they represent a direct threat to incumbent automakers. People see the decimation of the ICE industry in China and very easily imagine the same thing happening in their own sectors12.

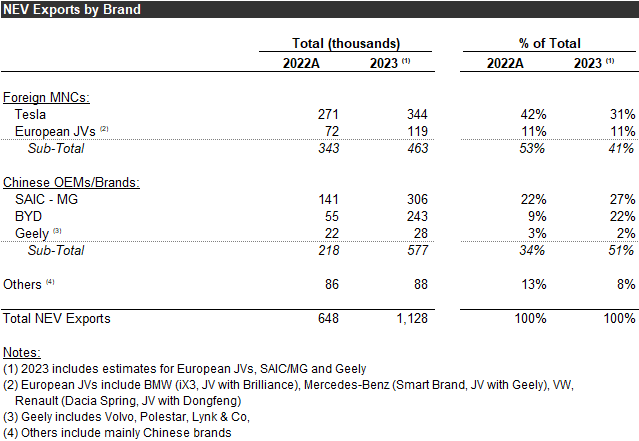

China’s NEV exports generally fall into two camps. First, there are exports of higher-value foreign brands that are produced in China and exported abroad, mainly to Europe13. This includes Tesla, MG14, Volkswagen, BMW, Mercedes-Benz and Renault. Second, some Chinese brands like BYD and Geely are just starting to explore export markets.

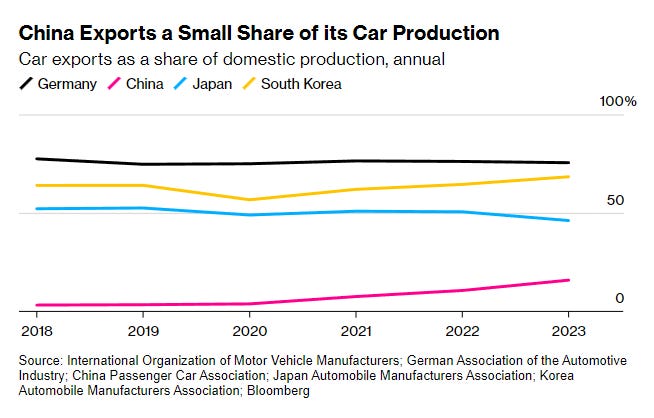

It is notable here that the foreign brands are relying on China as an export base more than Chinese brands. For example, last year, Tesla exported 36% of its China production. In contrast, only 8% of BYD cars were exported15.

It indicates how Chinese car companies are more focused on the domestic market for their NEV offerings. Unlike the export-oriented industrialization boom of two decades ago, Chinese domestic demand is supplying the energy to drive its advanced industries. Compare this to the auto manufacturing industries in Germany, Japan and South Korea, where the majority of domestic production is exported.

It also means that exports by foreign brands are naturally displaced as they open up their own local manufacturing facilities — for example, NEV exports to Europe declined in the first two months of the year, likely due to the ramping up of Gigafactory Berlin which began operation in 2022 and has been gradually ramping up production.

Some also conflate rising Chinese NEV exports as indications of “weak domestic demand” and “overcapacity”. However, export demand is real demand — Chinese NEVs are selling overseas because of their competitiveness; they are typically sold at much higher prices16 offshore compared to onshore.

Chinese automakers are also aggressively investing in manufacturing facilities abroad. Again in sharp contrast with the export-oriented industrialization boom from the 2000s, Chinese automakers are focusing on developing markets instead of trying to fight rising protectionism in developed economies. BYD is building local manufacturing facilities in Thailand and Brazil. Chery just announced a plant in Vietnam. As these manufacturing facilities ramp up, NEV exports from China will be replaced by locally manufactured vehicles.

Claims of automaking “overcapacity” not supported by the numbers

The hard data does not support the idea that there of significant overcapacity in auto manufacturing.

To the extent there is excess capacity in China’s broad industrial sector, it tends to be in categories that have been hit by the decline in housing construction like cement and glass. As you can see (black line below), auto manufacturing has actually been ticking upwards after bottoming out in the middle of 2022 during Zero-COVID.

Claims that China has upwards of 48.7 million17 in annual automaking capacity likely includes significant obsolete capacity in their calculation.

Other measures of overcapacity also corroborate the capacity utilization figures. The turnover of non-current assets (mostly factory assets) for auto manufacturing (yellow line below) has, if anything, been trending upwards over the past two years.

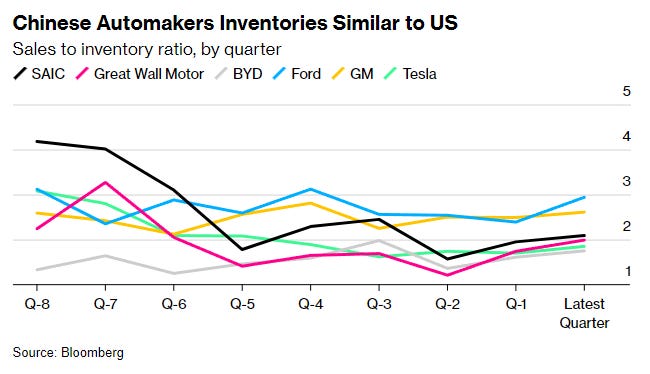

Inventories of Chinese automakers are also at normal levels18. There aren’t tons of cars piling up in dealer showrooms. Indeed, the transition to NEVs is also changing the way cars are sold. One under-appreciated aspect of the transition to electric vehicles has been the use of more direct-to-consumer sales approaches, famously pioneered by Tesla as it sought to disrupt the Big Three oligopoly in the United States.

Xiaomi, which made a name for itself in selling smartphones directly to consumers, recently demonstrated the power of this approach with the launch of the Porsche-esque SU7, racking up 88,898 reservations on the first day of its release for deliveries starting in April and May.

This distribution approach mitigates the amount of inventory required by linking demand directly to production. Moreover, advances in manufacturing19, simpler designs and deepening of the supply chain mean shorter manufacturing lead time and lowers the risk of building up excess capacity in the system. Capacity utilization at NEV automakers in China is generally much higher than traditional ICE manufacturers20.

With the industry moving rapidly from ICE vehicles to NEVs — over half of domestic sales are expected to be NEVs this year — the auto industry’s capacity utilization and working capital requirements are poised to continue improving over time.

China’s car market is right now hands-down the most brutally competitive market in the world with even Tesla’s Q1 sales wilting from the competition. Consumer subsidies for NEVs were phased out at the end of 2022 and after a brief dip, NEV sales have started accelerating once again.

NEVs are taking over because they have long surpassed ICE vehicles in total cost of ownership and the brutal competition continues to wring out impressive gains in production efficiencies throughout the supply chain. Lower prices unlock new sources of demand and drive further market growth.

Indeed, not only are Chinese NEV makers not suffering from overcapacity, they face real constraints of not being able to open up new factories and production capacity fast enough. To merely reach Taiwan levels of vehicle penetration (~350 per 1,000)21over the next decade, China would have to increase automaking capacity by 3-4 million per year, every single year22. This is roughly the equivalent of South Korea’s entire domestic production capacity and Japan’s domestic sales.

Given the huge consumer surplus and quality of life benefits from Chinese households switching over to NEVs, from a long-term perspective it is probably far more accurate to say the industry is woefully under-supplied.

1An unmistakeable reference to “Barbarians at the Gate” which told the story of KKR and its hostile buyout of RJR Nabisco.

2September 8, 2023

“Over-capacity is a feature, not a bug, of industry evolution in China. Understanding where we are industry development cycle by looking at past examples can help us predict how the EV and battery industry will evolve in China.”“Over-capacity at this stage is a feature, not a bug. It’s a filter in the Darwinian process of weeding out less-competent or qualified competitors. More important to capital efficiency in the long run is getting through this phase quickly.”

January 26, 2024

“Overcapacity is a feature, not a bug, of advanced tech-centric manufacturing when industries are in rapid growth stage. You need to scale up with highly automated manufacturing to drive down unit costs. Lower unit costs then unlocks new demand.”March 5, 2024

“ ‘Over-capacity is a feature, not a bug’ of the clean energy transition. Over-capacity in clean energy is going to save this planet.3The “feature, not a bug” part is a reference to how Chinese policymakers think about it. Namely, they do not see it in the same negative connotation, like how Michael Pettis uses the term here. On the contrary, they see it as an important element of industrial development.

4I put quotes around the term “overcapacity” because it typically carries a negative connotation of deviating from established standards whereas it has actually been instrumental in raising the living standards of Chinese people for decades.

5“How China Works”, like “How Asia Works” by Joe Studwell, is an excellent read. There must be something magical about the “How X Works” title format.

6Lan Xiaohuan, 置身事内:中国政府与经济发展 via Pekingnology translation:

Predictable adoption curves:

“To start with, a developing country, such as China, can see trends in developed countries. Certain products that became everyday items in developed countries first, such as color TVs, refrigerators or washing machines, are surely to catch on in developing counties later.”

Learning spillovers:

“Firstly, local factories not only provide employment, but they also help to serve as training grounds for local workers, helping local peasants’ transition to industrial roles”

“the factory essentially assumed an educational function for the industrial economy and had a strong positive externality on the economy, and it should be subsidized and supported”

Competition:

“… benefit of overinvestment is that it increases competition. Overcapacity has made price wars a norm for many products in China. Therefore, for a long time, innovation in cost reduction was the main type of innovation pursued by Chinese companies”

“Functional simplification and cost innovation are very important”

“But when these [Western] products are introduced to Chinese consumers for the first time, they are too fancy and too expensive”

“It is exactly in this stage of brutal competition that the industry is developing quickly, numerous small firms rise and fall fast, and resources and technologies are quickly concentrated in the hands of leading companies. Both technology and product improve rapidly.”

7Here I do not put the term in quotes, because everyone agrees that excessive capacity in mature industries is bad.

8Following the 2008 GFC, there was the notable resource rotation from export-oriented processing factories into concrete- and steel-intensive housing and infrastructure industries. To support this, Chinese industrial companies made heavy investments to increase capacity in domestic manufacturing. However, after growth plateaued in 2014-15 (triggering a global commodities bust), industrial companies suffered from low capacity utilization.

10Tao Ren & Xiaotan Zhang (March 2023), “Does China’s overcapacity-cutting campaign take effect as intended? Evidence from listed manufacturing companies”

11Chinese Americans in particular remember the beating death of Vincent Chin, an autoworker in Detroit.

12To be clear, this is a very clear threat. I am personally in favor of ensuring we can develop a competitive domestic electric vehicle market and supply chain. The primary focus of this piece is on whether exports qualify as “overcapacity”.

14MG is a British brand that was acquired in 2005 after its collapse by Nanjing Auto (now owned by SAIC). MG was rehabilitated under SAIC ownership and is now thriving as a competitive brand with both ICE and NEV offerings.

15They also tend to be exported more to developing markets like Brazil, Thailand and Indonesia.

16Bloomberg (December 2023), “China Pulls Punches to Keep Pricey Electric Cars Flowing to EU”

“EVs made in China, such as BYD’s Dolphin compact crossover and SAIC-owned MG Motor’s MG 4, fetch roughly double on average in Europe compared to their home region, customs data show.”17Just Auto “The polarisation of China’s automobile production capacity”. Review of bottoms-up capacity calculation includes commercial vehicle manufacturers as well as defunct legacy auto manufacturers and plants.

18Bloomberg (April 2024) “China’s Overcapacity Is More About Solar and Batteries Than EVs”

19Notably, new advanced manufacturing facilities are designed to be highly automated and easier to convert between different product lines. If demand for vehicles were to plateau at a lower level than expected, these factories could be converted into other use cases relatively easily.

20Bloomberg (April 2024) “China’s Overcapacity Is More About Solar and Batteries Than EVs”

21Source: Wikipedia (April 2024). Note: Taiwan’s vehicle penetration is not even that high by OECD standards. Chinese cars are already now more affordable relative to incomes than Taiwan.

22Based on my internal forecasts showing a ramp-up from ~8 million in domestic NEV sales in 2023 to ~43 million in 2033 and an increase in the passenger fleet from 336 million to 480 million plus assumptions on vehicle retirement rates. This does not include exports.

Subscribe to reading, writing & investing

By Glenn Luk · Launched 4 years ago

Mental models for business, investing and economic development

Lithium Related Media Articles, page-21955

Add LTR (ASX) to my watchlist

(20min delay) (20min delay)

|

|||||

|

Last

$1.43 |

Change

0.025(1.79%) |

Mkt cap ! $3.454B | |||

| Open | High | Low | Value | Volume |

| $1.40 | $1.43 | $1.38 | $15.16M | 10.75M |

Buyers (Bids)

| No. | Vol. | Price($) |

|---|---|---|

| 2 | 89338 | $1.41 |

Sellers (Offers)

| Price($) | Vol. | No. |

|---|---|---|

| $1.43 | 99382 | 10 |

View Market Depth

| Last trade - 16.10pm 16/05/2024 (20 minute delay) ? |

|

|||||

|

Last

$1.41 |

Change

0.025 ( 0.24 %) |

||||

| Open | High | Low | Volume | ||

| $1.40 | $1.42 | $1.38 | 2394503 | ||

| Last updated 15.59pm 16/05/2024 ? | |||||

| LTR (ASX) Chart |