It’s been a long wait but it looks like we are going to be rewarded handsomely for it.

I for one will be taking up my full entitlement and any as many shortfall shares as I can muster, as I’m sure most of you will.

I anticipate a strong run until the ex-date in June caused by investors rushing to buy in to receive their in-specie entitlement in LLL so that they don’t have to pay $1.50 - $2.50 for them later in the year.

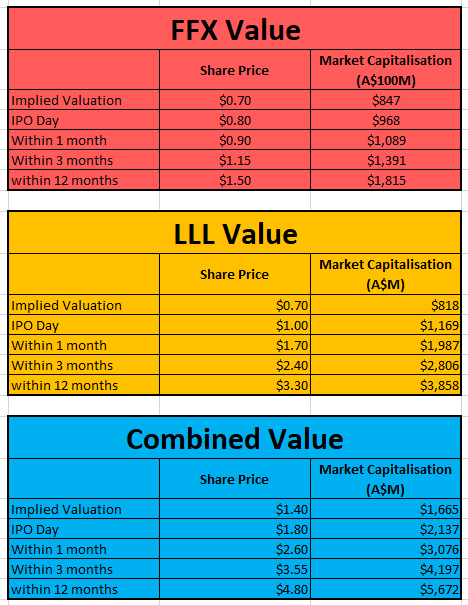

I’ve had a crack at running some back of the envelope numbers to value each company once they are separated, to break down the value proposition initially, with some reasonable potential future valuations based upon fundamental analysis & peer comparison.

I have assumed that the maximum amount of shares are issued, given that everyone is going to be scrambling to get their hands on LLL shares at 70c.

LLL Value

Fundamental Analysis

I’ve posted extensively on how Goulamina is in the top 3 hard rock lithium assets globally and certainly #1 of the ASX listed projects, refer back to those or company presentations but to summarise:

- Large scale (>100Mt), yet has barely been explored with the deposit open in all directions = large production rate (>800ktpa), scope to increase to meet global demand

- High grade (>1.5%) = lower costs & increased production

- Excellent metallurgical and mineralogical characteristics = lower costs & superior product

- Lowest OPEX of ASX listed projects = increased profits & protection in a downturn

- Partnership with Ganfeng = funding & security of offtake

- Advanced, with construction underway and ordering of long lead time items commenced - Low CAPEX & Capital Intensity – no longer worth worrying about as the project is fully funded, but worth mentioning in regard to further expansion

The DFS completed in 2020 demonstrated a post-tax NPV of $4.1B (45% attrib. to LLL).

Given that the project is much more advanced, fully funded, and SC6 prices are up to $6,000/t from the ~$1,000 used in the DFS, I think it’s safe to say that LLL is worth >$4B now.

Things to look forward to: Goulamina will ultimately end up a >8Mtpa mine. Vertical integration with the production of lithium hydroxide & sales directly into Europe must be next, followed by the development of other lithium projects in Mali & Ivory Coast.

Broker Valuations

Cannacord, J Capital (an interesting contender!) and Euroz have price targets on FFX of ~$1.90/share with a large weighting towards the value of Goulamina.

Cannacord's sensitivity analysis below gives an indication of the change in NPV based upon higher SC6 prices.

At $2,300/t SC6 pricing, the post-tax NPV of the project is >$11B (>$5B attributable to LLL).

With current SC6 pricing >$6,000/t, contract pricing of $2,300 is in the bag.

I would like to see Cannacord’s figures at $5,000/t contract pricing. I imagine that would imply a valuation of >$10B for LLL.

Peer Comparisons

LLL’s peers are valued much higher in terms of sheer market capitalisation, let alone market cap/NPV.

Our closest peer, AVZ who are also developing a large-scale lithium mine in Africa are trading at >$3.5B.

Other peers are trading in the $2.5 - $3.5B range but more interestingly are trading well above their DFS NPV’s.

This should put an absolute floor price on LLL at ~$2B, but an equivalent value of >$3.5B.

As discussed above, LLL has several advantages to it’s peers i.e. OPEX, production volume, advanced stage, offtakes, permits, etc therefore FFX should trade at a premium to some of these peers.

FFX Value

Fundamental Analysis

Again, I have posted extensively on the exceptional characteristics and upside potential of the Morila gold mine and Massigui project, however a short summary:

- Fully funded 4.5Mtpa project

- Growing production to >200kozpa

- Low AISC of $1,124/oz which is set to reduce in the upcoming mine plan

- Resources of >2.5Moz and growing with the Morila orebody open, and several significant targets in the project area being tested

Based upon the numbers in the Life of Mine Plan from 2021, I calculate a post-tax NPV of >$650M. This figure will increase significantly on the back of the revised LOMP later this year with a larger & higher grade reserve, >200kozpa production, lower AISC, additional LOM etc.

20% LLL Holding: $233M (LLL at $1 – this obviously increases significantly as LLL grows)

Cash: $100M

Therefore, an initial valuation of $900M would be reasonable.

This equates to just above 70c. FFX should be well supported here with institutional buying on the back of their raising to fund their 20% stake in LLL.

The project has advanced significantly since this point, with significant capital invested, mining of the main orebody commenced, and production increasing to 100kozpa, and 150-200kozpa by the end of the year.

Not to mention the price of gold is much higher and on the rise due to inflation.

Peer Comparison

Our closest peer, WAF in Burkina Faso is producing 230kozpa at an AISC of around $950/oz. They are currently trading at $1.4B.

This is pretty close to where FFX will be by the end of the year with ramped up production to 150 – 200kozpa from the current rate of ~40kozpa.

Plus FFX will own 20% of LLL which will likely be trading at >$3B = ~$600M in value to FFX.

I suspect FFX will flip this holding in a year or so at a hefty premium to enable the acquisition of additional gold projects – Tongon anyone?

Scenario

Here is an example of what you are entitled to if you own 100,000 FFX shares, and how I think that investment will grow from now to the next 12 months:

I think my guesses of the opening prices of $0.80 and $1 are quite conservative, especially for LLL – we could see it gap up significantly more, check out how IPO’s are performing lately (100 – 200% gap ups from their proposed IPO prices).

The question will be, how badly do people want to lock in LLL shares now + get the FFX sweetener vs paying >$2 for LLL alone just around the corner?

The run will be on now, and could be exacerbated if the lithium sector goes on another tear.

Time to GameStop this b*tch to the 6th of June and beyond!