If the US doesn't use its strong USD as a purchasing power to buy more Foreign Reserves. It'll be hard to maintain as a world no1 economy.

The rate is so low and the Fed has been sitting at intersection for A SIGNAL from others. I'm afraid It'll not ride out the NEXT storm. Japan's Strategy To Fix Its Deflation Problem

By George T. Hogan, CFA, FRM, CIPM | Updated April 08, 2015

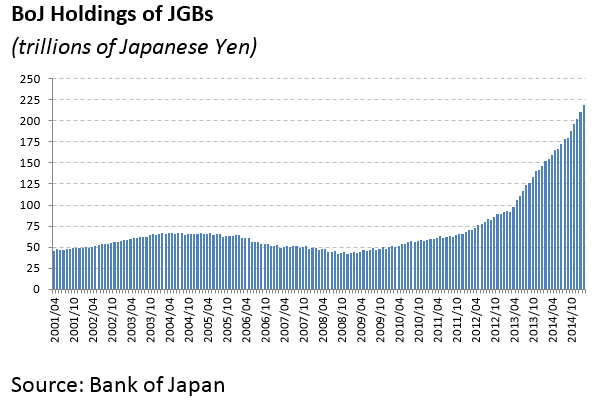

Since April 2014 the Bank of Japan (BoJ) has embarked upon a massive government bond (JGB)-buying program that has seen it purchase JGBs at a rate of ¥5.5 trillion ($46.6bn) per month. In fact, during that time the BoJ’s stock pile of JGBs has rocketed from ¥98.1 trillion to ¥218.5 trillion ($1.8 trillion). Putting that figure into perspective, that’s roughly the size of Canada’s economy (11th largest in the world) at the end of 2014, according to IMF figures.

All of this begs the question, why would the BoJ do this, and how long can it possibly last?

Jump-starting consumption

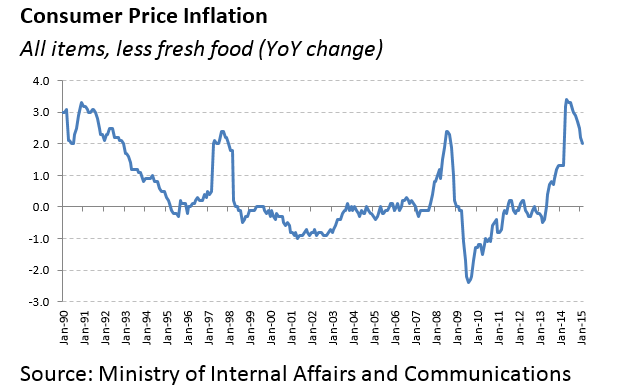

Naturally, the BoJ’s bond-buying program wasn’t a matter of chance, but rather a very deliberate action with a very specific goal in mind: ending deflation and jumpstarting consumption. Japan’s economy has been in a moribund state ever since its bubble economy burst in the early 1990's. This time, now often referred to as “Japan’s lost decade(s)”, has been marked by sustained periods of low inflation and deflation (see chart below). (For related reading, see article: The Lost Decade: Lessons From Japan's Real Estate Crisis.)

Deflation is generally considered to be problematic, because of its negative impact on consumption -- that is, even with interest rates on savings at nearly zero, households have an incentive to defer consumption until later periods when prices are falling. As money sits in the bank and, over time, the price of goods and services declines, the purchasing power of that money increases. So it pays to wait before buying. (For related reading, see article: The Dangers Of Deflation.)

As a result, to counter this negative pressure on consumption (a key component of economic growth itself), Japan's government and the BoJ needed to come up with a plan to force prices to start rising again. One way that was pinpointed for potentially achieving this is by increasing the money supply. If the amount of money circulating in an economy increases, but the supply of goods and services remains constant, then prices should go up, all else being held constant. Or at least that’s the thinking. (To read more about the various initiatives a government undertakes to impact market processes, see article: How Governments Influence Markets.)

So how does bond-buying achieve this? Financial institutions (whether they be banks, credit unions, insurance companies, investment managers, etc.) are key facilitators of the flow of money in any economy. They take money from those households and corporations that have cash to save, and then lend this money back to households that need it (e.g. to buy a house or car, or to make purchases using credit cards), as well as corporations (e.g. to build new plants or hire more workers), and even the government. So if the BoJ starts to buy JGBs from those financial institutions, then the financial institutions end up with a lot of extra cash on hand.

Because those financial institutions are unlikely to just sit on this cash, it is hoped that they will turn back to households and corporations for profit-making opportunities. They can either attempt to offer loans, etc. on better terms, or they may even consider rolling down the credit chain and offering loans to customers that they previously were reluctant to consider. Either way, more households can afford to buy homes, cars, and other goods and services, while at the same time more businesses can get the cash they need to expand their operations by building/expanding factories and hiring workers. And all of this new demand should, in the end, lead to higher prices.

The key magic trick here is this: The BoJ is the institution that has the ability to print money in Japan. So it doesn’t necessarily need to “have” the money in advance that it needs to buy JGBs. Rather, the BoJ simply decides how many bonds it wants to buy, and then it “prints” the cash it needs to do so. Naturally though, the actual process is a bit more complicated than that.

Some Evidence of Success

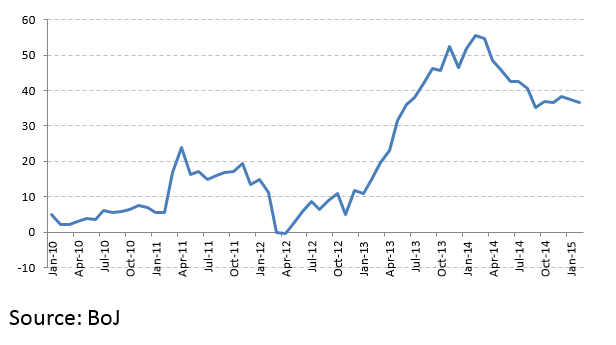

So is all of this working, then? On the one hand, there does seem to be at least some evidence that the program is working. First, according to the BoJ, the monetary base in Japan has seen a massive expansion that has corresponded with the bond-buying program (see chart below).

Monetary Base

YoY growth

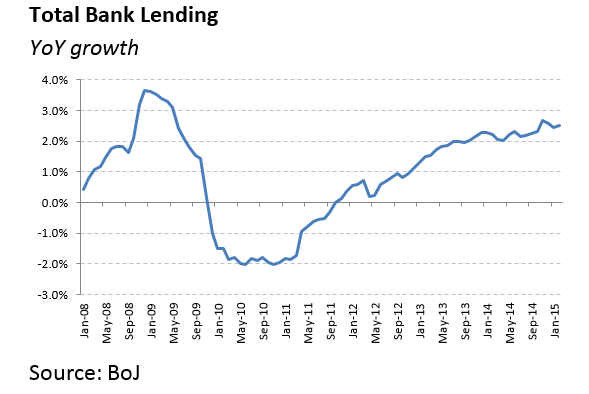

And critically perhaps, bank lending has indeed begun to accelerate subsequent to a sharp decline in the wake of the global financial crisis (see chart below).

Unfortunately, not all indicators paint as rosy a picture.

Causes for Concern

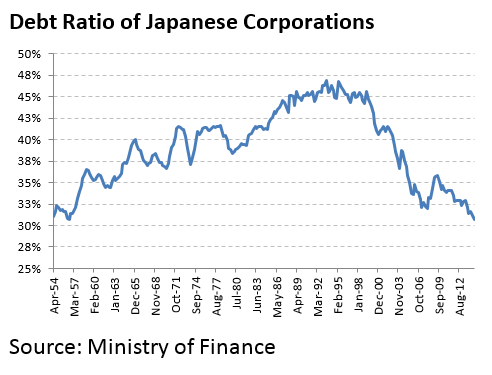

One lesson that has been learned by Japanese corporations the hard way (many would even say overlearned) since the collapse of the bubble economy, is that over-reliance on debt financing can be dangerous. In fact, since peaking out at 46.9% in the quarter ending July 1993, the debt ratio (bonds and borrowings to assets) of Japanese corporations has fallen to its lowest level since the 1950's (see chart below). And their cash position had grown to a staggering ¥164.7 trillion ($1.4 trillion) by October 2014, according to Japan's Ministry of Finance.

In other words, it’s not entirely clear whether Japanese corporations really would want to borrow to expand their operations. Assuming that they did want to expand, with so much cash on hand, why would you need to borrow? As a result, much of the debate regarding the next steps to be taken has focused on how to get corporations to start using their massive hordes of cash.

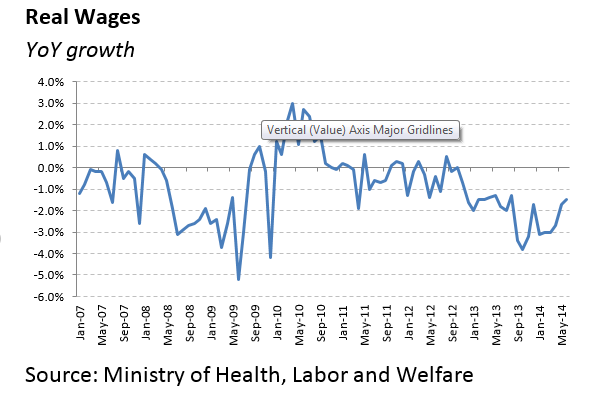

More importantly, perhaps, real wages in Japan have been falling almost continuously during this entire bond-buying program (see chart below). With household wages falling, consumer budgets are shrinking, again suggesting that households themselves may have little demand for any extra lending capacity that financial institutions may have.

But perhaps the most worrisome indicator is inflation itself. In April 2014 the government hiked the national sales tax from 5% to 8%. Adjusting for that hike in sales taxes would suggest that, despite all of this bond buying, real prices have continued to fall (or at least grow much slower than hoped for) throughout almost the entire program.

Difficult Balancing Act

There are deeper concerns as well, first about the unintended consequences of bond buying, as well as the ability of the BoJ itself to continue buying at this pace.

Along with American, German, and British government bonds, JGBs have often been considered the gold standard of low-risk investments. Setting aside concerns from rating agencies like Moody’s and Standard & Poor’s about Japan’s debt load for a moment, these four countries’ government debt instruments represent massive, liquid, and stable markets, and are denominated in four of the world’s most important reserve currencies. (For related reading, see: How Do Central Banks Acquire Currency Reserves And How Much Are They Required To Hold?)

That being said, there are legitimate concerns that the BoJ’s bond-buying program, given its scale, is severely restricting the secondary market for JGBs (where institutions trade bonds between themselves and other investors). If the secondary market dries up, that may make current holders of JGBs concerned about their liquidity, and hence they may avoid buying new issues in the future. At its extreme, this could eventually negatively affect the Japanese government’s ability to raise new debt. (See: A Look At Primary And Secondary Markets.)

Furthermore, Japan’s debt load relative to GDP is already considered to be the largest in the developed world by most measures. Commonly quoted at over 200% of GDP, Japan’s debt load dwarfs even that of Greece, a country which many think is on the verge of bankruptcy and expulsion from the Eurozone. With JGBs already representing 83.5% of the BoJ’s balance sheet, concerns could quickly grow about the viability of the BoJ itself if ever the solvency of the Japanese government came into question.

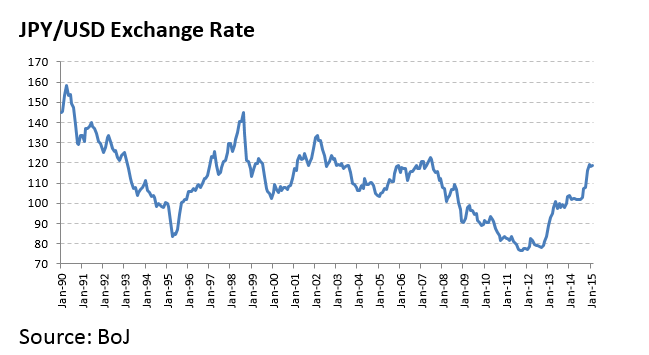

While that scenario may be viewed by many as only minutely possible in the short-term, a more practical concern is the prospect of a global currency war. As the chart below shows, after an extended period of time in which the Yen strengthened against the dollar (and most other currencies), the BoJ’s bond-buying program in combination with other “easy” money policies has helped contribute to a sharp reversal of that trend. (For related reading, see article: The U.S. Dollar's Unofficial Status As World Currency.)

A weak currency is generally favorable for exporters, because it means goods produced at home become cheaper (and hence more competitive abroad). But with the Eurozone limping into yet another potential currency crisis with Greece, the Euro too has been weakening relative to the dollar. If the US government becomes concerned enough about the impact this could have on the American economy, it could embark on its own campaign to weaken the dollar. And that could put the brakes on growth in corporate profitability in Japan, and could even add more deflationary pressure on prices (a strengthening yen would make foreign goods cheaper in Japan, putting more downward pressure on prices). (See: Global Trade And The Currency Market.)

Source: BoJ

Finally, in a worst-case scenario, there is the specter of hyper-inflation (think of Germany post-World War I). The fear here is that the transition from inflation to deflation, and back the other way, is a particularly difficult one to manage. With deflation having become so persistent in Japan, and with many other major economies around the world also eyeing the specter of deflation (including the US, the Eurozone, and some fear even China), the fear is that the actions necessary to resuscitate inflation in Japan may be so extreme that once inflation finally does return, it will be impossible to control. If confidence in the Yen begins to fail, it is feared, then the ability of the Japanese government to raise the funds it needs to operate and service existing debt could also come in to doubt.

The Bottom Line

Few would disagree with the argument that, after over two decades of deflation and economic malaise, bold action was needed in Japan to mark a change in the country’s course. And far fewer would argue that the steps that have been taken thus far are anything but bold (though some have questioned the wisdom of those actions).

However, the government of Japan and the Bank of Japan (BoJ) are engaging in an extremely delicate balancing act with potentially dangerous consequences. The dilemma they face is, don’t go far enough and risk failing to break out of the trend of an extended economic slump, even after having spent trillions of yen, but go too far and risk inviting the potential of hyperinflation, loss of confidence in the Yen, and a government debt crisis. While many remain hopeful that the government and BoJ will manage to thread this incredible needle, that task still appears far from done. (For related reading, see: Quantitative Easing: Does It Work?)

Get Out of Debt – Start Making Money

Want to get out of debt, get a mortgage and save for retirement? Investopedia’s FREE Personal Finance newsletter shows you 7 Steps to Become Financially Independent. Take control of your money and Click here to start managing your finances like the pros