from intelligent investor weekend briefing and why Americans should look carefully at who they elect as presidentThe Powell Enigma

Jerome Powell was clear in his press conference on Wednesday that the Fed believes monetary policy is restrictive at the moment, despite the rebound in inflation, the tightness of the labour market in the US. He even said he thought the first quarter slowdown in GDP growth to 1.6% was underselling America's economic strength.

His whole tone was that the Fed isn't too worried about inflation and thought that price growth would soon resume its decline towards the target of 2%: "I think it's unlikely that the next policy rate move will be a hike. To hike we'd need to see evidence policy is not sufficiently restrictive — that's not what we see."

But he also suggested rate cuts aren't on the way either, saying: "If we had a path where inflation proves more persistent than expected, and where the labour market remains strong but inflation is moving sideways, and we're not gaining greater confidence, that would be a case in which it could be appropriate to hold off on rate cuts."

Well, that's where things are now, so it's pretty clear that he's saying the Fed will hold off on rate cuts. Robert Armstrong in the FT called it "The Frozen Fed", that "on the evidence of yesterday's statement and chair Jay Powell's press conference, is utterly frozen between two poles, unable to even gesture in either direction."

And by the way, when asked whether there was any danger of stagflation, Powell said he could see neither "stag" now "flation" ahead.

This is all good for markets. As Steven Blitz of TS Lombard pointed out (quoted by John Authers of Bloomberg): "The market seems to understand that when the economy is raising interest rates rather than the Fed, it signals growth. The near-100-basis-points change in market pricing of the funds rate in January 2025 has rallied markets as opposed to the opposite last fall."

So when the Fed or RBA is on hold, and credit markets are raising rates instead, stock markets love it because it means growth that won't be stomped on. It truly is the time of Goldilocks.

Will the Fed go too far, as usual, and break something? Viktor Shvets says it doesn't matter anymore because if something goes wrong in the morning, it can be fixed in the afternoon.

He wrote yesterday:

"We maintain that today is truly different. Why?

1. For the first time ever, we reside in a world of abundant not scarce capital, with financial assets being 5x-10x larger than GDP (depending on treatment of derivatives and contingent liabilities). Although this excess capital is not fairly or efficiently distributed, there are no shortages.

2. Unlike previous eras, we enjoy instantaneous risk re-pricing, enabling the Fed to turn on a dime, with communications policies playing the most important role in reshaping markets.

3. The Fed is now rolling out new policy instruments at warp speed (usually over the weekend), quickly plugging holes (à la SVB or repo lines) to avoid systemic risks. Investors should expect that in due course Fed is likely to roll out other policies designed to address specific concerns. In this world the Fed might commit a policy error, but perpetuating it is neither likely nor necessary."

But he raises a note of caution: "Alas, risks do not disappear, they migrate - in our case, away from markets to social and political spheres. Thus, there is a price to pay: ... shallower growth, unpredictable investment rotations, polarisation, geopolitical and social pressures. However, deflation of bubbles is not on the menu, and for a while, assets should remain in the Goldilocks zone."

And of course there is plenty of evidence of the migration of risk to geopolitical and social pressures, the latest being the university campus protests in America over Israel's behaviour in Gaza.

And then there's...

The Trumpocalypse

I can't stop thinking about this quote from Rabobank's Australian macro strategist, Ben Picton, in this short note about interest rates this week:

"Rabobank revises our RBA policy rate forecast to include 2x further 25bps hikes (August and November of '24) to reach a terminal rate of 4.85%, slightly above our terminal Fed Funds forecast - We have removed future cash rate cuts from our forecast in accordance with our house view that Donald Trump will win the US election and enact structurally inflationary universal tariffs."

So Ben thinks Australian interest rates will rise because Trump will win the US election and impose a universal tariff! Goodness me. And he's right! There's not enough discussion in Australia about what happens if Trump wins - it's arguably the biggest risk facing the country.

After reading Ben Picton's note, I read this interview with Trump in Time magazine, in which they asked him in detail what he would do as President.

On tariffs he was asked: "You have floated a 10% tariff on all imports, and a more than 60% tariff on Chinese imports. Can I just ask you now: Is that your plan?"

Trump: "It may be more than that. It may be a derivative of that. A derivative of that. But it will be somebody—look when they come in and they steal our jobs, and they steal our wealth, they steal our country.

When you say more than that, though: You mean maybe more than 10% on all imports?

Trump: More than 10%, yeah. I call it a ring around the country. We have a ring around the country."

He's also going to incarcerate and deport tens of millions of people from America, using the National Guard, and he wants to give police immunity from prosecution.

It's a grimly fascinating interview, worth reading in full. If Trump wins, the polarisation that Viktor refers to will definitely come to pass; the concern is that it will come to pass if he doesn't win as well.

Oxford Economics says that if Trump did impose a universal tariff of 10% and an even bigger one against China, then China would devalue its currency by 10%. This would wipe out Australian manufacturing because presumably, the Australian Government would not match Trump's tariffs.

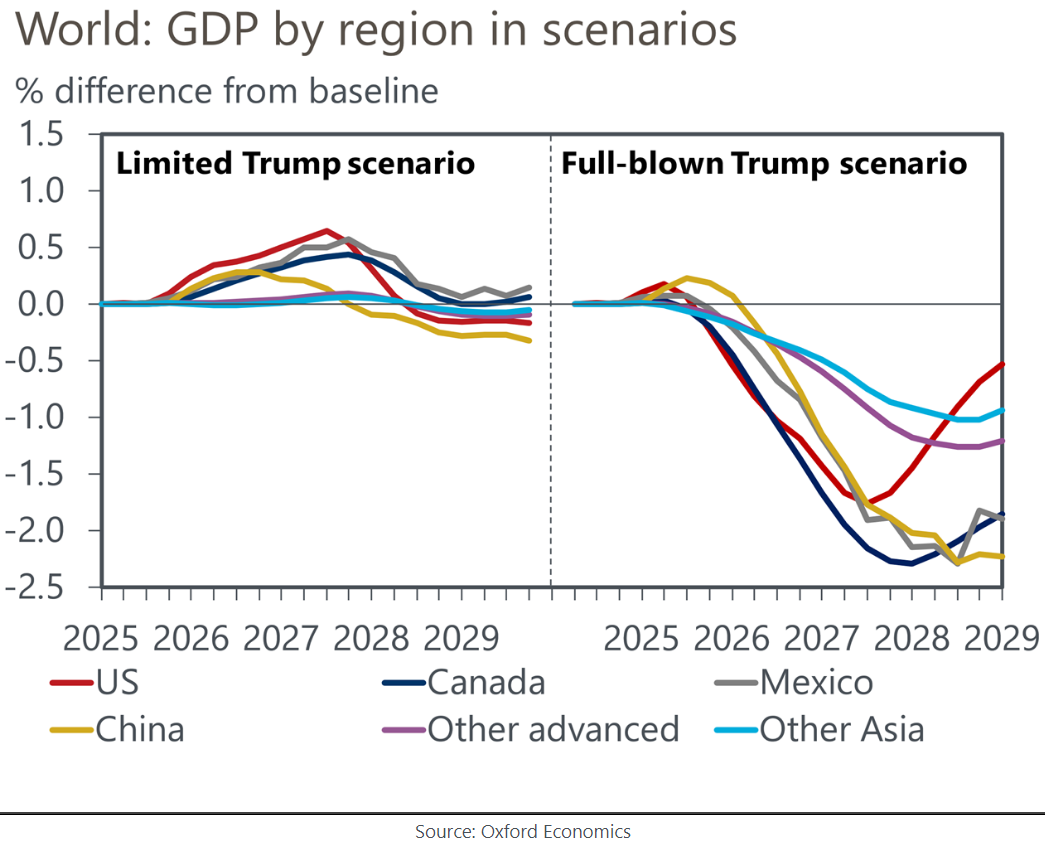

That's what Oxford Economics calls the "full-blown Trump" scenario, which it says is less likely than "Limited Trump", although that looks like wishful thinking to me.

Limited Trump is: looser fiscal policy thanks to extending personal tax cuts and the federal debt-to-GDP ratio rises 4.5 percentage points by 2033; 25% tariffs on targeted imports such as metals and autos are levied on the EU and China, who retaliate; and immigration is cut by 30%. Full-blown Trump is better for the US budget because the tariffs would reduce the deficit.

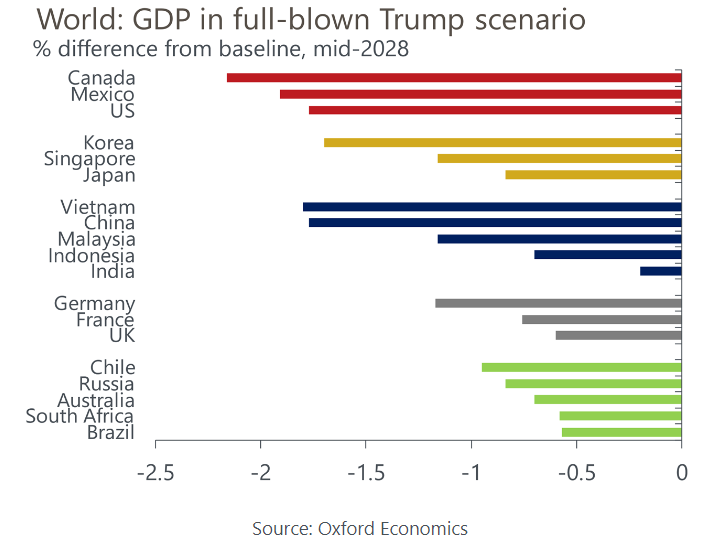

Full-blown Trump would probably cause a global recession - it would certainly hit countries hard that depend on exports to the US. Here's Oxford Economics' view of the difference between the two Trump scenarios:

A full-blown Trump world would have both "stag" and "flation" - that is, slow growth and possible recession, coupled with higher inflation.

Nobody wins in such a world, but the relative winners in stagflation, like during the 1970s, would be commodity-exporting countries like Australia:

So to sum up: if Trump wins, Australia's manufacturing sector would be crushed but resource stocks would do relatively better, and Australia would become more of a quarry than it already is.

About a month ago, Evan Solomon, who is with a think tank called GZero North, focusing on Canada-US relations. Solomon wrote about what he called the "Preparing for Trump (PFT) Industry" following a meeting with a senior Canadian minister. He recalls there was a "hot political minute" when Canadian PM was the "Trump Whisperer" but that all went pear-shaped when Trump called him two-faced and the bromance ended in ashes.

"Trump carries a grudge the way Thor wields a hammer — so expect carnage if Trudeau is still in power when the new trade deal is renegotiated in 2026.

The first Trump administration was, like all presidencies, a mixture of political ideology and political policy, with the president surrounded by advisors who acted as guardrails to his impulsive aggressions. They kept the alliances intact. That's no longer the case. Those internal guards have been purged in favor of hardened partisans running a permanent war room campaign that has a strong animating force: Revenge. Just this past week Trump's own Truth Social media channel raised billions of dollars, feeding a media ecosystem that insulates him and his team from any uncomfortable intrusions of facts that might upend his self-reinforcing political narrative. Political appetites will devour logical policymaking. So, what is the strategy in that scenario?

In 2024, PFT means trying to find a way to give Trump something that he can publicly claim as a "win," without looking weak to your own voters.

And what is that?

Jobs.

Maybe the PFT industry is why Trump supporters say he's so effective. Before he's even in power, he already has the upper hand. His threat of over-the-top retaliations has effectively put the US in a stronger negotiating position on trade, security and diplomacy — and he's not yet in office. His plausible threat to collapse the status quo is his most effective negotiating tool. It may make for less trustworthy alliances, weaker international treaties and a more dangerous, less prosperous world, but it fulfills the number one Trump promise to his supporters: America First.

Is there a 'Preparing for Trump' industry in Australia? It doesn't look like it, although maybe it's going on behind the scenes.

Another thing a PFT would do is prepare for worse global warming. Trump has promised to achieve "lowest cost of energy of any industrial country." To do it, he will ditch Biden's green transition and the Inflation Reduction Act and pivot back to exploiting US domestic fossil fuel resources, principally oil and gas.

GaveKal says this means scrapping direct subsidies and tax credits for wind and solar projects, ending tax breaks for electric cars, tearing up Biden-era energy efficiency rules, dropping emission standards, and reversing the recent ban on new liquefied natural gas export facilities.

At the same time, the government will resume licensing oil and gas exploration and production on federal land, encourage drilling in the arctic, promote investment in oil and gas infrastructure including pipelines, and overhaul electricity pricing to favour natural gas generation.

I imagine this would mean the whole global effort on climate change would break down as other countries follow the US.

As for monetary policy, Jerome Powell's term is due to finish in May 2026, 16 months into Trump's presidency. He will presumably appoint someone who was more pliable, if not a lackey prepared to do his bidding. That would mean lower interest rates and higher inflation, especially if, as expected, taxes are cut and the deficit blows out further (mind you, the deficit will blow out whether Trump or Biden wins in November).

What does it mean for sharemarkets? That's not at all clear, or uniform. GaveKal says that "Rising yields could weigh on multiples, but deregulation and tax cuts will generally be positive for equity prices. Individual sectors and companies may be injured or favored by tariffs, and by a swing away from green subsidies and towards fossil fuel incentives."

"Beyond the first year of a new Trump term, markets could begin to get nervous that Trump could replace Powell with a Fed chair prepared to keep monetary policy loose and to buy up much of the new debt that the Treasury will be issuing. "If so, the US dollar could sell off dramatically, inflation expectations could surge, and foreign appetite for treasuries could abate. In this scenario, the moderate rise in bond yields anticipated for 2025 could give way to a surge in bond yields, as in the late 1970s—with all the associated collateral damage inflicted on the US dollar."

and new tech in USA

A flame-throwing robot dog can now be purchased in America. Price: US$9,420. It's called the Thermonator. Throwflame claims that its product is good for "wildfire control and prevention," "agriculture management," "ecological conservation," "entertainment and SFX," and "snow and ice removal," although it also seems like it would be especially good for committing arson. (Gizmodo)

from intelligent investor weekend briefing and why Americans...

-

- There are more pages in this discussion • 1 more message in this thread...

You’re viewing a single post only. To view the entire thread just sign in or Join Now (FREE)

Featured News

Featured News

The Watchlist

SER

STRATEGIC ENERGY RESOURCES LIMITED

David DeTata, Managing Director

David DeTata

Managing Director

SPONSORED BY The Market Online