For the other …um … innocents ?

Currently safer than teddies for when ‘all else fails’ although perhaps not so cuddly?

And one needs to learn to let go :/

…. But not yet!!

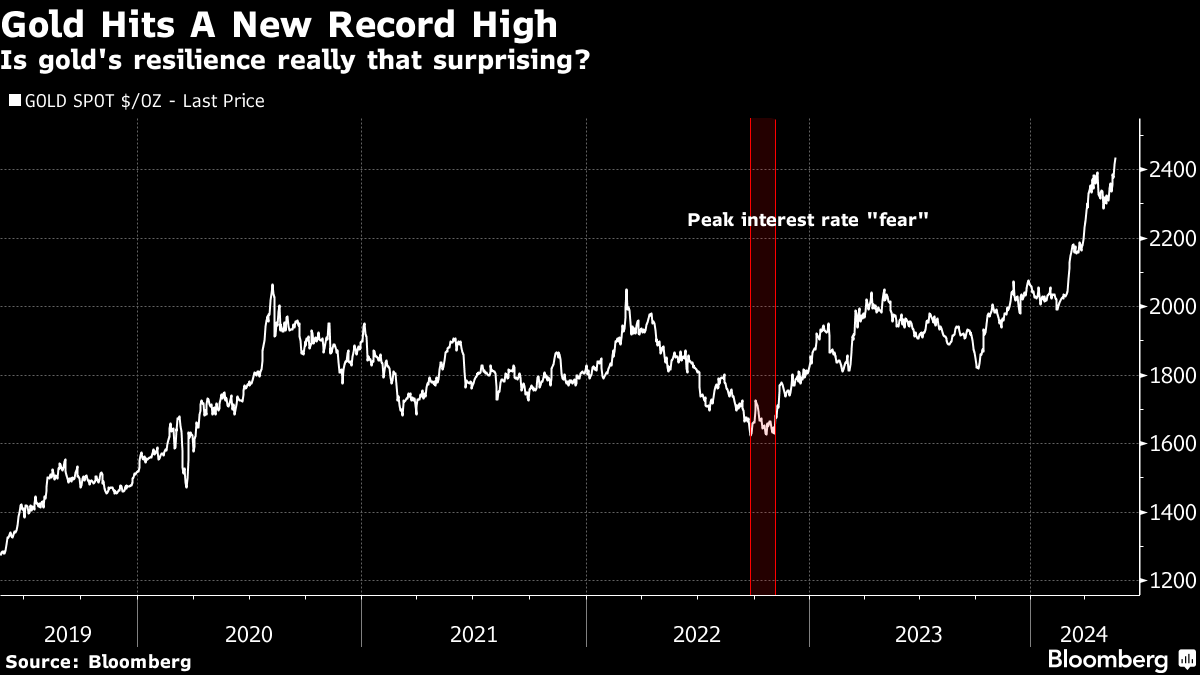

Gold is back at a new record high. The price of the yellow metal is now above $2,400 an ounce.

A number of things strike me as interesting about gold’s current advance.

As I’ve mentioned before, it’s not generating much fanfare, partly because lots of other stuff is hitting record highs too (have I mentioned the FTSE 100 lately?).

Another is that it has largely happened against a backdrop of higher interest rates and a strong US dollar. Neither of those things are traditionally viewed as good for gold. Gold is priced in US dollars (so all else being equal, a rising US dollar should mean a falling gold price); and gold pays no interest, so in a rising rate environment, that’s a drawback.

One factor generally agreed to have kept gold resilient is hefty demand from central banks, and China in particular.

The International Monetary Fund’s first deputy managing director, Gita Gopinath, highlighted this factor in a striking recent speech to the Stanford Institute for Economic Policy Research.

China’s central bank has increased the share of gold in its total currency reserves from below 2% in 2015 to 4.3% last year.

Meanwhile — and the dollar doomsters will find this interesting — it has reduced its holdings of US bonds from 44% to 30%.

Gopinath argues this “suggests that gold purchases by some central banks may have been driven by concerns about sanctions risk.

This is consistent with a recent IMF study confirming that FX reserve managers tend to increase gold holdings to hedge against economic uncertainty and geopolitical including sanctions risk.”

Chinese appetite for gold goes beyond its central banks, and certainly makes sense, as we’ve discussed here before.

That said, if you look at a chart of gold over the past five years (oh look — there’s one below, don’t say I’m not good to you), I’m not sure its staying power is quite as mysterious as it looks.

None of this is exact science. A lot of it is “feels.”

But you’ve got gold hitting a new high in mid-2020 as the Covid money-printing exuberance peaked.

You then have it meandering around before hitting another peak in March 2022, which was very much a geopolitical high (the Russian invasion of Ukraine).

From there, it collapses pretty hard until autumn of 2022 (that’s “fall 2022” for my endearingly literal-minded US readers). If you remember correctly, that’s when bond yields across the globe spiked to fresh highs. (And in the UK, they had a bit of an added shove from overleveraged pension funds and an overly bombastic prime minister).

Thing is, this was also the moment at which US inflation was peaking.

Meanwhile, in the UK, the Bank of England intervened to underpin the gilts market, and markets arguably regained some of their faith in the “central bank put” (the idea that central banks are both able and willing to resolve any heart-stopping moments in markets).

Gold started to rally as bond yields retreated.

We then got another spike higher in global bond yields in October 2023, which bond market gurus — with remarkably good timing — basically decried as a red herring.

Since then gold has been off to the races.

Why?

The inflation rate, while slowing, has been coming in on the warmer-than-expected side. But even given that, it has behaved well enough to allow central banks to continue talking about cutting interest rates. So in essence, you have a perceived bias towards lower “real” (after-inflation) interest rates.

That’s classically a good environment for gold — one where somewhat corrosive inflation appears quite possible but policymakers aren’t motivated to do anything about tackling it.

As Tim Hayes of Ned Davis Research puts it, “the continuation of current yield trends should perpetuate what remains a strong long-term uptrend in gold.”

Anyway, enough chatter about the macro side of things. What does it mean for your investments?

Investing in Gold

As I’ve pointed out many times in the past, I view gold as portfolio insurance and something that should form a (small) part of everyone’s asset allocation. So if you do own it, it’s more a matter of rebalancing occasionally if it starts to form too much (or too little) of your desired allocation. Here’s more on that topic.

In terms of bets on an ongoing gold bull market, that’s trickier. There are plenty of ways to bet on a higher gold price but you have to remember that they all involve market timing.

For example, gold miners have lagged the gold price significantly and although they are now starting to take off, they are still cheap relative to the gold price. But painful history demonstrates that these are cyclical holdings rather than long-term ones.

There are certain companies that you can buy and hold. Gold miners — at least, not in my investing lifetime — have not proved to be among them.

You buy them when they’re low and you sell them when they’re high. They’re a high maintenance investment.

If that’s something you feel comfortable with, there are plenty of exchange-traded funds (ETFs) that invest in various types of gold miner, as well as a handful of actively-managed gold funds. Just remember that you’ll have to set yourself some sort of indicator for getting out and that you will never be able to call the exact high.

(20min delay)

(20min delay)