Over the last few weeks we have had a certain amount of speculation about MEO.

WA-360-P or rather the Artemis prospect within WA-360-P is the point of interest at the moment. There has been conjecture about T/O's, JV's etc. and it has been said that MEO has nothing at the moment and will have nothing if Artemis dusts.

When the announcement does come it is better to know the company on which to base your decisions. I hope the following synopsis helps you:)

Firstly MEO have high equity in four established LNG provinces. Asset estimates as at 19th March 2009 are:

Carnarvon Basin - operator:

WA-361 P (35%): Heracles - Lead (2+Tcf GIP), Hephaestus Sth Lead

WA-360-P (70%) Drill/drop 31-Dec-09: Artemis prospect (20 Tcf GIP), Lady Nora - extn, West Zeus Lead, Eris Lead, Amphion Lead, Hebe Lead - Amphion Lead, Ersa Lead, Pandia Lead.

WA-359-P (60-70%) Drill/drop 31-Dec-09: Hephaestus Nth Lead.

Total estimates - 16.3 Mtpa existing existing LNG capacity, 4.3 Mtpa under construction and 20-35+ Mtpa under consideration. These estimates are conservative especially in light of resent seismic studies of Artemis.

Like Artemis there is a drill/drop date of 31st Dec 09 over WA-359-P so look for this permit as being included in the farminee negotiations. Because of the proximity of all permits then all may be taken into consideration, especially if it is a larger player. If not then MEO may look for an extension on WA-359-P.

Bonaparte Basin:

NT/P68: MEO has 100% title to the 12,070 sq.km exploration permit (petrofac has the option, at cost, tobuy back into a previous 10% share). This permit includes gas discoveries at Heron North and Blackwood. Also within the permit are the Heron South and Epenarra prospects.

Total estimates are 3.7 Mtpa existing LNG capacity.

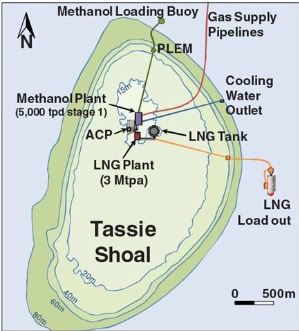

Secondly - Commonwealth environmental approvals have been granted to MEO for the development of the proposed Tassie Shoal Metanol project and the Timor Seal LNG project. These approvals are in place until 2052.

Basically, this project is to build an LNG and Methanol plant on Tassie shoal, an area of shallow water in the Timor sea located 275km NW of Darwin. The gas in the area is CO2 challenged. On land based LNG trains the CO2 is usually buried. At sea this is not possible so MEO's proposal is to convert the CO2 into methanol. With the emphasis on carbon reduction at the moment this is a neat solution. Both LNG and Methanol are cash products. A similar land based solution (in Darwin) would cost $3.2b. The Tassie shoal project has been estimated at $2.04b.

There is > 25Tcf undeveloped stranded gas in the Bonaparte basin in permits surrounding Tassie Shoal (excluding Ichyths). MEO have already stated that:

'there may be 1700 Bcf of raw recoverable gas at Blackwood.

The first methanol plant proposed for the Tassie Shoal Methanol Project requires approximately 1400 Bcf of raw gas (including inerts) to produce 1,750,000 tonnes per annum for 20 years of operation'.

With this in mind the Tassie Shoal projects are viable, once the funding is in place. Hopefully Artemis will assist the implementation of the Tassie Shoal projects. This management team have followed previous managemnt teams in pursuing this end.

As far as saying MEO is a single minded entity - I don't think so. There are plenty of worthwhile prospects in the bag which has been proven by the interest shown in the WA-360-P data room.

Whatever happens to the future of Artemis I believe Tassie Shoal is bound to happen. And Tassie Shoal is the key. The MEO management team have been patiently working towards their goal. We, as shareholders, need to be patient too.

Add to My Watchlist

What is My Watchlist?