- ABOUT BEN KRAMER-miningWEALTH Weekly Update

Home / Free Articles / miningWEALTH Weekly Update

Graphite

There’s been no news impacting the graphite companies we follow other than a small announcement from Great Lakes Graphite (TSX.v: GLK) (GLKIF), which expanded its financing by C$100,000 (at 8.5%, comes with 250,000 warrants at C$0.10/share expiring Sept. 15, 2019 and convertible at C$0.10/share).

Given that there is little news we decided to look briefly at the Li-B market. There is a very strong consensus that the Li-B market is going to take off like a rocket, and that this is going to drive graphite demand much higher over the next several years. In fact many argue that a new supply/demand paradigm dominated by Li-B consumption is in the works for graphite (not to mention lithium). Until now we have seen rapid growth, but we are about to see new markets that can bring about a quantum leap in demand: EVs and stationaries. Li-B bulls expect both products to become ubiquitous, and given their size we should expect to see far more Li-B cells being produced.

We dislike such universal consensuses generally and believe that the “Li-B demand to the moon” thesis has to at least be subjected to negative analysis, even if only to disprove it and to support the consensus.

What Can Impede Li-B Demand Growth?

Some of the demand growth projections for Li-Bs are astronomical given the aforementioned shift in the market towards larger products.

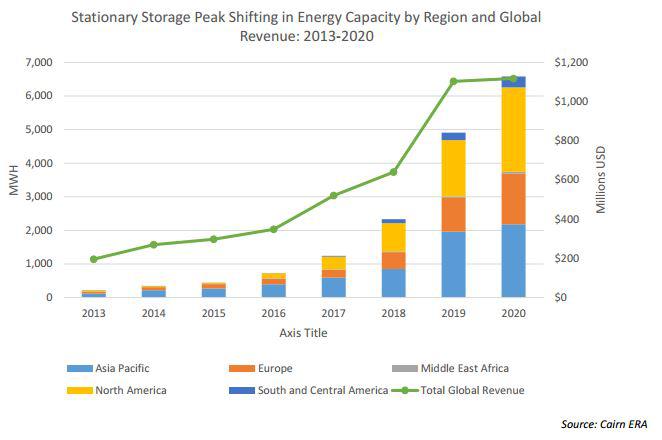

This doesn’t include stationaries, which some investors think will be the biggest market of all. I recently came across this chart showing a projection for stationary battery MWhs. that shows a magnitude of growth over the next five years.

When we convert these projections into projected graphite demand it is clear that the market dynamics change. Note that this chart contains amorphous graphite demand (low value material that comprises >50% of the market by volume).

These aggressive demand projections are contingent upon new markets developing, and these market in turn require new value chains that are larger and more efficient than those available today. There is a technology gap risk that suggest that this market will likely grow at a slower pace than expected. We think it also means that those companies who survive will have to enter with a small footprint. There are two reasons for this. The first is that battery costs are too high, and they have to come down substantially to make EVs and stationary batteries sufficiently attractive in the marketplace. The second is that the materials that are being used to make batteries more efficient are becoming more specialized as manufacturers need to control the battery’s chemical reaction with greater precision. Such specialized products have not been scaled up to the extent that they need to be for the above lofty projections to become reality.

Let’s look at these concerns in greater detail.

The Battery Cost: This is a concern for larger batteries, which given their size and their functions are going to be extremely expensive given current per kwh costs. This is not an issue for smaller batteries in, say, laptops or small portable devices, since the energy required to operate them is low compared with their cost. However, powering a car or storing large amounts of energy require much more energy and storage capacity. While this isn’t an apples-to-apples comparison consider that a Tesla (TSLA) EV will have several hundred, or maybe even more than a thousand times more battery cells than a laptop. A car only costs 50-100X more than a laptop, and so the battery cost relative to the product’s value is much higher in the EV/stationary.

We doubt the industry’s ability to sufficiently reduce prices in the next few years without a radical, unpredictable shift in the battery’s structure or material content (and this could exacerbate concern #2). Battery prices have come down steadily on a cost-per-kwh-basis.

Some are predicting that Tesla can get its costs considerably lower than this (<$100/kwh), yet this isn’t based on any hard evidence, but rather loose estimates based on new technological developments such as switching the liquid electrolyte with a gel or increasing the silicon content in the cathode. None of these processes has been scaled to the level of the proposed gigafactories, and it is very difficult to predict how expensive it will be to make these changes on a large scale.

This observation suggests that there will be less demand growth in the large Li-B market (i.e. EVs and stationaries) than many analysts are expecting.

Material Supply Chain Difficulties: The second is the availability of materials and the necessary value-add chain to create enough battery power. Today, Li-Bs require four materials: lithium, graphite, cobalt and nickel. Nickel isn’t an issue since it is a widely used commodity. Lithium, graphite, and cobalt are very small markets that are vulnerable to supply shortages, even in the event of a modest shift in demand. Most of the world’s lithium is produced by three companies. Graphite needs to go through multiple processes before it can be used in Li-Bs, and the processing capacity doesn’t exist. Right now many companies use synthetic graphite but natural graphite offers the potential for better performance is cheaper, and is less destructive to the environment. Cobalt is produced predominantly as a by-product of base metal mining, and therefore it is subject to supply shortages and price-spikes should base metal mines shut down (as we are seeing today).

As we saw with respect to cost, battery/EV companies have ambitious expansion agendas. This created a speculative frenzy in some of the raw material companies developing lithium, graphite, and cobalt projects, and this frenzy is predicated on growth projections for raw materials that take dramatic battery growth into consideration.

So there are two issues here. The first is that raw materials might be in short supply. The second is that the processed materials might not be available in sufficient quantities even if the raw materials are available: the infrastructure simply doesn’t exist yet as the material inputs are becoming more heavily engineered.

This will likely put pressure on growth, even if we see it in a high-price Li-B environment.

What Should Investors Do?

We think that there is tremendous potential for investors looking to benefit from battery cost production, although the process is largely taking place in secret. Investors might blindly bet on Tesla or another Li-B hopeful, but they aren’t in a position to judge what is going on. On the resource side we’ve seen time and again how graphite companies who say that they have battery-grade graphite must prove an enormous amount to the market, much more than we’ve seen. We think the value is in the processing. This is in part why we like Great Lakes Graphite, and why we haven’t dismissed Mason Graphite (TSX.v: LLG) (MGPHF) as a potential future investment. With respect to the latter the company is a shareholder in and partner with Group NanoXplore, which is a graphene and carbon composite company doing the kind of research that could potentially make Li-Bs more efficient by improving anode material.

With respect to lithium we think prices are elevated given the high concentration of production in very few hands, and that disappointing battery demand (compared with lofty expectations) could put pressure on prices. Lithium producers are also in various chemical businesses that have different supply/demand fundamentals, and I don’t think that these are good ways to get lithium exposure unless you want exposure to other industry’s as well. Junior companies have enormous hurdles to overcome, although we won’t dismiss the likelihood that there aren’t a couple of winners out there.

Ben is long shares of Great Lakes Graphite and Medallion Resources.

[IMG] ABOUT BEN KRAMER-miningWEALTH Weekly Update Home / Free...

Featured News

Featured News

The Watchlist

FHE

FRONTIER ENERGY LIMITED

Adam Kiley, CEO

Adam Kiley

CEO

SPONSORED BY The Market Online