Everyone has different opinions but I tend towards those who understand Mining and the Market over pundits....

MRL Corporation did not need a JORC but because of the Ignorance about SL Vein and Graphene and MRL Corporation the same old negatives are restated instead of thinking about it clearly...

MRL Corporation essentially sent their vein graphite to the same researchers that showed that Talga's ore was amenable to graphene production. MRL corporation however was able to achieve graphene yields in excess of 90% from the exfoliation of its vein graphite compared to 2-12% for Talga resources. The quality of the graphene it produces also appears comparable to Talga but was more crystalline in nature.

Sri Lankan vein graphite has commanded a premium in the market due to its high carbon content (90-99%). Its production has always been limited by the nature of the deposits, narrow, typically only a few cm to a meter wide as the name vein implies. This characteristic means that it is not feasible to drill a JORC compliant resource for a deposit.

The civil unrest in Sri Lanka has also limited production and by 2012 production of vein graphite was down to less than 3200 tonnes with only 2 mines left in production. Production in 1916 was 33,000 tonnes.

At present MRL has identified approximately 220 old mines on its 5 separate graphite project areas. The company believes that with the application of modern mining methods they will be able to follow these deposits deeper as historically large amounts of graphite were produced from quite shallow mines.

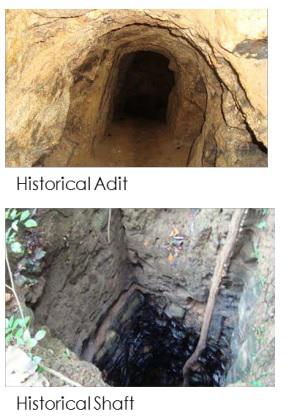

Figure 10. Historical Sri Lankan Vein Graphite Mine.MRL Corporation Presentation.

At this stage MRL corporation have yet to clarify the process by which it will achieve production and has yet to publish a feasibility study. Its market capitalisation however is only $8 million which would see incredible leverage in case of success and after its recent capital raising has at least >$1 million in cash at bank to continue operations.

Negatives for an investment in MRL Corporation

Geography risk in Sri Lanka.

No JORC compliant resource.

Untested technology.

Production of commercial quantities of graphene 2+ years away.

Positive for an investment in MRL Corporation

Vein graphite may have unique properties.

First mover advantage in Sri Lanka.

Leveraged graphene play due to extremely low market capitalisation.

Talga Resources (TLG:ASX) current focus is the development of its Vittangi Graphite project in Sweden. This deposit was previously owned by Teck Cominco now Teck Resources (TCK:NYSE) and this was purchased by Talga Resources in 2012 for $478,500 and a 1% net smelter return. A further 2% net smelter return is due to Phelps Dodge now Freeport-McMoRan (FCX:NYSE).

Its Vittangi deposit in Sweden is the world's highest grade JORC compliant graphite deposit at 7.6Mt @ 24.4% Cg. There is minimal overburden with a uniform deposit which allows for ease of extraction.

More importantly the uniformity of the graphite allows Talga to make graphene directly from Vittangi ore rather than synthetic graphite. The unique nature of Talga ore can be seen most readily by looking at the raw ore itself.

Figure 3.Synthetic graphite compared with Vittangi ore. Talga Resources Presentation. (click to enlarge)

Figure 4.Trial Block Mining at Vittangi.Talga Resources Presentation. (click to enlarge)

Like Grafoid, Talga has not detailed the exact mechanics involved in the production of its graphene but it appears that it may use the conductive properties of the ore to liberate the graphene. This simple process also appears to produce high quality few layer graphene with an Id/Ig of 0.23 and large particle size.

Figure 5.Talga Graphene Production Process.Talga Resources Presentation.

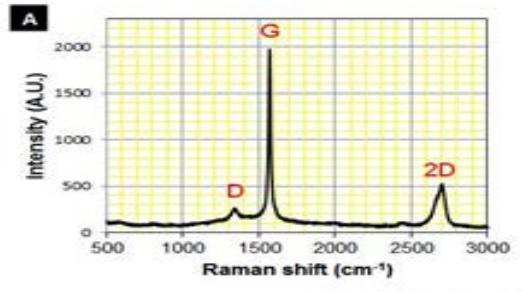

Figure 6. A) Raman Spectroscopy and B) Atomic Force Microscopy of Talga Graphene.Talga Resources ASX Press Release.

(click to enlarge)

Talga has already sold some of its graphene to a German 3D printing company and has started production at its pilot plant (capital cost A$1 million) in Germany. Production at the pilot plant is ramping up in 3 phases to a production rate of 100-200 tonnes of graphene per annum. Talga expects to reach this production rate by the end of 2016 at which point it will be one of the largest producers of graphene in Europe.

The capacity to directly produce graphene directly from raw ore leads to low capital costs and impressive net present values in its feasibility study. Management have been deliberately conservative in their assumptions with a 12% discount rate used and a 2% graphene yield when test yield results from Vittangi drill cores have reached >10% as the numbers would not be believable.

Figure 7. Feasibility Study Results for Vittangi Project.Talga Resources ASX Press Release. (click to enlarge)

Figure 8.NPV of Vittangi Project Versus Graphene Yield Results.Talga Resources ASX Press Release.

(click to enlarge)

Negatives for an investment in Talga Resources

Untested technology.

No offtake agreements.

Positives for an investment in Talga Resources

Will be one of the largest graphene producers in Europe by the end of 2016

Low market capitalisation, $40 million

Capital cost of Vittangi project low, $21 million.

Net present value of Vittangi project high, $343 million.

Production of few layer graphene has started at its pilot plant.

Capital cost of Vittangi project may be covered by revenue from pilot plant.

High quality few layer graphene has been produced.

I think with more research you see here MRL Corporation is far superior and moving far faster...

It is important to cut through the Marketing like this ... it down plays what it wants and glorifies what it wants.

MRL Corporations results and short processing time is historic. Even people uninterested in investing agree with this simple fact.

I spotted many errors in this one; did you spot any?

Like we spotted in the above Review any basic comparison reveals the tale in my opinion...

Here is a quick comparison:

In September 2014 Talga released the results of a scoping study based on an opencut mine at a 4:1 strip ratio producing 250,000 tpa ore grading some 24% total graphitic carbon (TGC). The process plant would upgrade this to 40,000 tpa of graphite concentrate grading 80-85% purity (which could be sold for $480/t) and 7,000 tpa of graphene grading 99.9% purity. However, it was thought that only a limited tonnage of the graphene could actually be sold as graphene because of the limited market for the material at this pioneering stage of the industry, and Talga assumed, for the sake of the exercise, that 1,000 tpa would be sold as graphene with the remainder sold as high quality graphite priced at US$1,600/t. That would result in annual project revenues of some US$84m. Capital cost was put at around $30m. Operating costs were put at $84/t of feed (i.e. $21m annually) and that included processing costs.

MRL could achieve revenue of US$75m from mining say 5,000 tpa (continuing with the example provided by CPS Capital) and producing 1,000 tpa graphene priced at US$55,000/t and 4,000 tpa of high quality battery grade graphite priced at US$5,000/t, at a capital cost probably well under $10m, at much lower operating costs (a cost of US$600/t for the raw graphite would amount to $3m annually, to which must be added the cost of processing) and probably earlier to boot.